Don’t let anyone tell you otherwise: financial stocks are still a hotbed of dividend (and share-price!) growth for contrarian income-seekers like us.

I know what you’re going to say next: “Brett, everyone says finance stocks are overbought.”

I get it, and that sounds logical … on the surface.

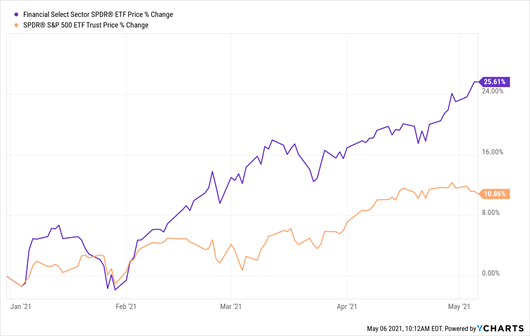

It is true that when the calendar flipped to January, finance stocks surged, more than doubling the price gains of the S&P 500, going by the performance of the benchmark Financial Select Sector SPDR ETF (XLF):

Finance Stocks on a Tear …

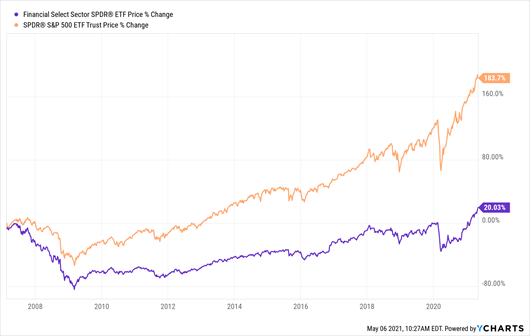

But here’s what most folks have missed: even with that gain, finance stocks are only 20% above where they peaked prior to the last financial crisis 14 years ago. And they’re still way behind the market in that span.

… But They Only Just Finished a 14-Year Consolidation!

That’s a crystal-clear sign that this sector has (finally!) consolidated and is ready to move higher from here.

Fed to Investors: “Buy the Banks Now”

We can thank the Fed for the upside to come in finance stocks, for many reasons.

For one, Fed Chair Jay Powell has been clear that he has no interest in lifting the Fed’s key lending rate from its zero-point-nothing level anytime soon. Banks profit from the gap between this rate and the yield on the 10-year Treasury note.

And you no doubt know that the yield on the 10-year, which guides rates on everything from car loans to mortgages, has nearly doubled from sub-1% levels prior to January. That’s why bank shares have booked big gains in ’21.

My latest forecasts still see more upside with 10-year bond yields reaching 2% in the coming year. That’s the sweet spot for banks, because it lets them pull in higher loan income at a rate that won’t scare off borrowers.

Circle June 30 as the Next “Launch Date” for Finance Stocks

But no matter what happens with bond yields, the Fed’s got us covered another way: on June 30, it’ll likely let banks resume dividend hikes, so long as they pass the next round of the Fed’s stress tests, after Powell and Co. put a lid on banks’ payout growth at the start of the pandemic.

Powell will also likely take the handcuffs off share buybacks, too. Repurchases have been allowed, starting in the first quarter, but with strict limitations.

Here are three stocks—an insurer, a bank and a closed-end fund (CEF)—that are well-positioned to cash in on these changes.

US Bancorp: Big-Bank Stability With Small-Bank Growth

US Bancorp (USB) is a name most folks know: it’s America’s fifth-biggest bank by assets and has branches in 26 states. It’s a smart play on both the relaxation of Fed restrictions and a bump in US Treasury rates.

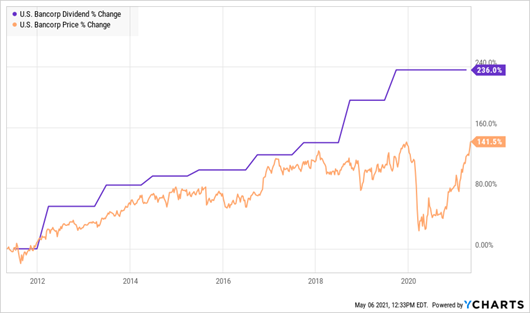

For starters, it’s a reliable dividend grower: the shares yield 2.8% today, but USB’s payout has more than tripled in the last decade. The share price has followed the dividend higher—until last year, when the onset of the crisis washed out bank stocks (and everything else!).

USB Chases Its Dividend—and a Buy Window Opens

I’ve written before about how share prices almost always track dividends higher—it’s why your favorite dividend stocks always seem to have roughly the same current yield, no matter when you look them up on your favorite stock screener. (Because you calculate dividends by dividing the yearly payout into the current share price.)

This also means that when the stock price lags the dividend, you’ve got a buying opportunity—especially in the case of a bank like USB, whose payout is being artificially held back (for now) by Fed restrictions. The bank’s dividend accounts for just 35% of its earnings, so it can easily resume hikes when it gets the go-ahead.

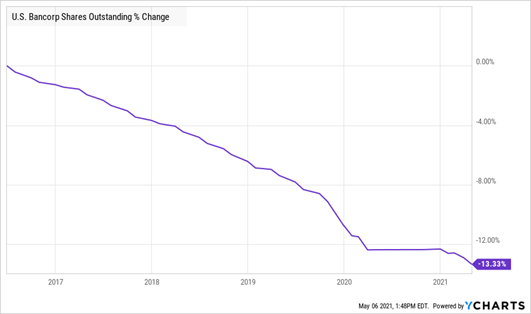

The stock should also get a lift from an easing of buyback restrictions: as you can see below, USB was a big repurchaser of its shares pre-pandemic, taking 13% of them off the market in the last five years (including the Fed-induced lull in 2020). It also restarted these purchases as soon as it was cleared to in Q1:

Fed Puts USB’s Buybacks on Hold, Setting Up a Stock-Price Surge

Any move by management (and us!) to buy shares would be well-timed: USB trades at just 13.1-times forecast earnings today, below its pre-pandemic level of 15.

Prudential: An Ignored (for Now) 4.4% Dividend

Insurers are another smart buy now, because they invest the premiums they collect in safe investments like Treasuries, whose yields I expect to break over 2% in the coming months, as I mentioned earlier.

Stand-alone insurers don’t face the same restrictions as banks. The biggest one, MetLife (MET), won an exemption from being considered a “systemically important” financial institution in 2016.

As such, they haven’t had their dividends and buybacks handcuffed the same way those of banks have. So we can’t look for quite the same lift for insurers when the Fed removes dividend restrictions in June.

But there are still some bargains to be had among insurers. And no, MET isn’t our best buy here. Instead we’re going to go with Prudential Financial (PRU), which we’ve covered a number of times before on Contrarian Outlook.

PRU’s dividend yields a nice 4.4% now, much more than MET’s 2.8% payout. It’s also cheaper, trading at 71% of book value, or what it would be worth if its physical assets were broken off and sold off today. MET, for its part, trades at 78%—though it should be noted that both valuations are insultingly (to management!) cheap. We’re basically getting both firms’ businesses for free.

But what we really love is the fact that Prudential is a shareholder-return machine, shoveling cash back to investors through dividends and buybacks that are driving the share price higher.

Dividends Up, Buybacks Up, Share Price Up (With Room to Run)

You can also see above that the stock hasn’t quite caught up to its share-price growth after the March 2020 crash (though it’s making a strong run!) This, as with USB, indicates our upside.

BTO: An All-in-One Play With a 5.5% Payout

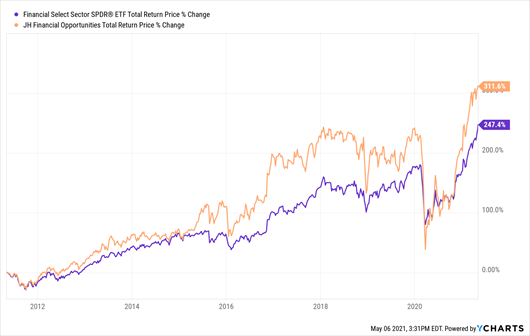

Finally, if you like to buy stocks through ETFs, let me offer this advice: do so through a CEF, like the John Hancock Financial Opportunities Fund (BTO), instead.

The biggest reason: dividends! BTO yields 5.6%, miles ahead of the 1.6% yield on XLF, the finance-sector ETF I mentioned earlier.

You’re also getting a nice mix of regional and national banks: BTO’s top holdings include Bank of America (BAC), US Bancorp and Citigroup (C), as well as regional players like Citizens Financial Group (CFG) and Fifth Third Bancorp (FITB).

The fund has also easily outperformed XLF in the last 10 years, so you’re getting strong performance from its management team:

BTO Wipes Out the Benchmark

Don’t be put off by the fact that BTO trades at a 2% premium to net asset value (NAV, or the value of its portfolio). It regularly trades at even bigger premiums, and I expect that to be the case again soon, making now a good time to get in.

— Brett Owens

Mysterious “Stamford Secret” Dividend Plan Exposed [sponsor]

I’ve found a fund with a killer edge its competition can only dream of—its managers, an unsung duo from sleepy Stamford, Connecticut, get first crack whenever a new stock comes on the market!

An advantage like that could literally be like buying Microsoft before its IPO! Or IBM. Or even Apple.

No wonder this low-key duo ALWAYS beat their benchmark. An “automated” ETF simply can’t keep up with these “ultimate insiders.”

Powered by this hidden advantage, their fund throws off a massive 6.5% dividend that dwarfs the payout on common stocks:

Huge “Stamford Secret” Dividend Reigns Supreme

This terrific fund is a “must own” for anyone looking for inflation-proof income, whether you’re in retirement or still building your nest egg.

I’m ready to share all the details with you now. Click here and I’ll give you everything you need to know about this amazing income play, including its name, ticker symbol, dividend history and full profiles of its high-powered management team.

Source: Contrarian Outlook