When you are interested in owning stock in an outstanding — but probably overvalued — company, what do you do?

Some would argue 100% of the time that you should wait and let the price come back to you.

To do so, you must be content knowing you might never own a piece of that company.

Over the years, I have passed on many stocks due to overvaluation; usually I’m happy I didn’t “overpay” for them, but occasionally I’ve regretted missing out.

For the longest time, Costco (COST) was in that latter category for me.

I kept waiting, but my price never came. I finally decided to pay the premium but got antsy when the price ran up, and I was happy to sell for a relatively quick 44% profit in March 2019.

In the two years since then, however, COST has experienced a market-beating total return of about 50%. Nice job selling, knucklehead!

A modest pullback in COST’s price this year seduced me again, and I gave into temptation by making some small purchases. Most recently, I bought a few more shares last week at $323 apiece.

I am taking these bites of COST knowing that it’s unlikely I’ll see the meteoric price appreciation of the past several years; I’m just glad to have a small stake in a great company, and I am looking for nice long-term performance.

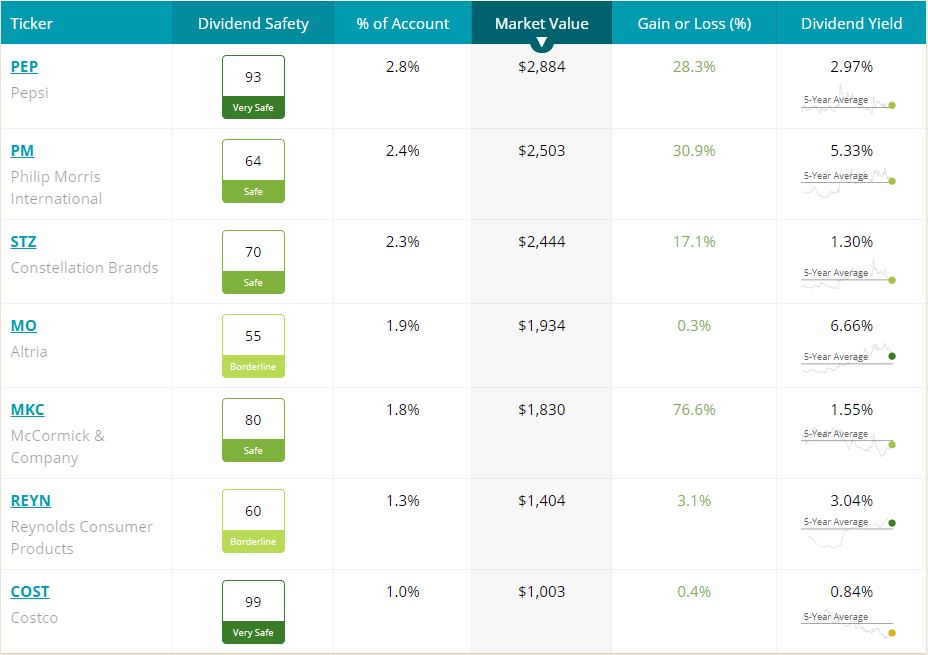

With that in mind, I also decided to add Costco to DTA’s Income Builder Portfolio.

On Monday, March 22, I executed a purchase order on Daily Trade Alert’s behalf for about $1,000 worth of the indomitable warehouse retailer.

COST becomes the portfolio’s 41st position. (See them all, as well as links to my IBP articles HERE.)

It is our second big-box retailer, joining Home Depot (HD), but our first general retailer.

Costco is the IBP’s 7th holding in the Consumer Staples sector, which makes up about 13% of the portfolio. Only Information Technology (21%) and Healthcare (15%) are better represented.

Valuation: How Costly Is Costco?

Costco is trading at about 33 times this year’s projected earnings. Even if profits grow an average of about 10% annually, as expected, the $333 we paid is 27.5 times forecasts for 2023.

Nevertheless, this is such a high-quality business and such a proven performer — as I discussed at length in my previous article — COST still is worthy of investors’ consideration.

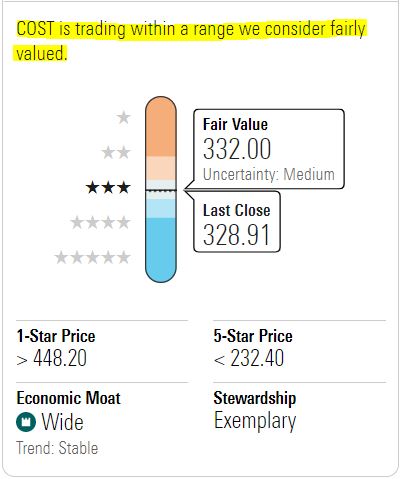

For example, the IBP added the stock almost exactly at Morningstar’s fair value price.

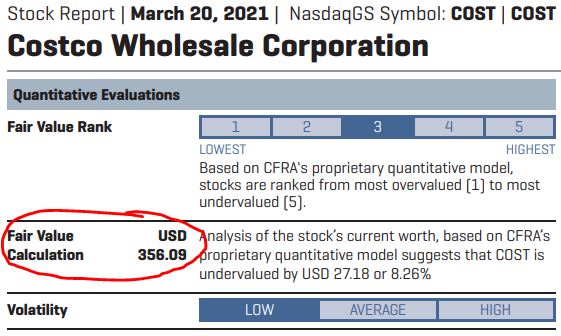

Citing Costco’s strong balance sheet, “defensive characteristics” and history of dividend growth, CFRA values COST at about $356.

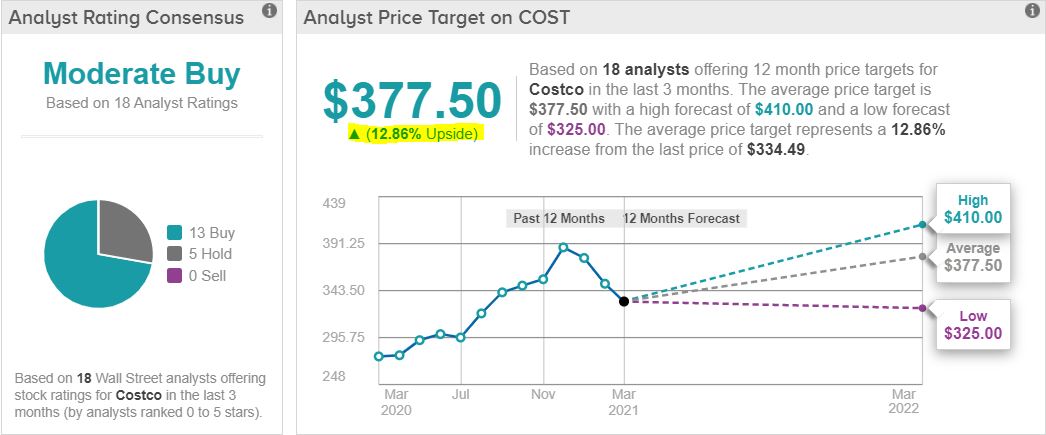

And analysts are quite bullish on the company’s near-term and long-term prospects.

Of 18 surveyed by TipRanks, 13 are calling COST a Buy, and their consensus 12-month price target suggests 13% upside from here.

The story is similar for the 34 analysts polled by Thomson Reuters, with 24 giving COST either a Strong Buy or Buy rating.

Thomson Reuters, via fidelity.com

Value Line just added COST to its model portfolio of “Stocks With Above-Average Year-Ahead Price Potential,” so it’s not surprising to see analysts there projecting good performance: $408 is the midpoint of their 18-month price range; and their 3-5 year target predicts longer-term gains of as much as 50%.

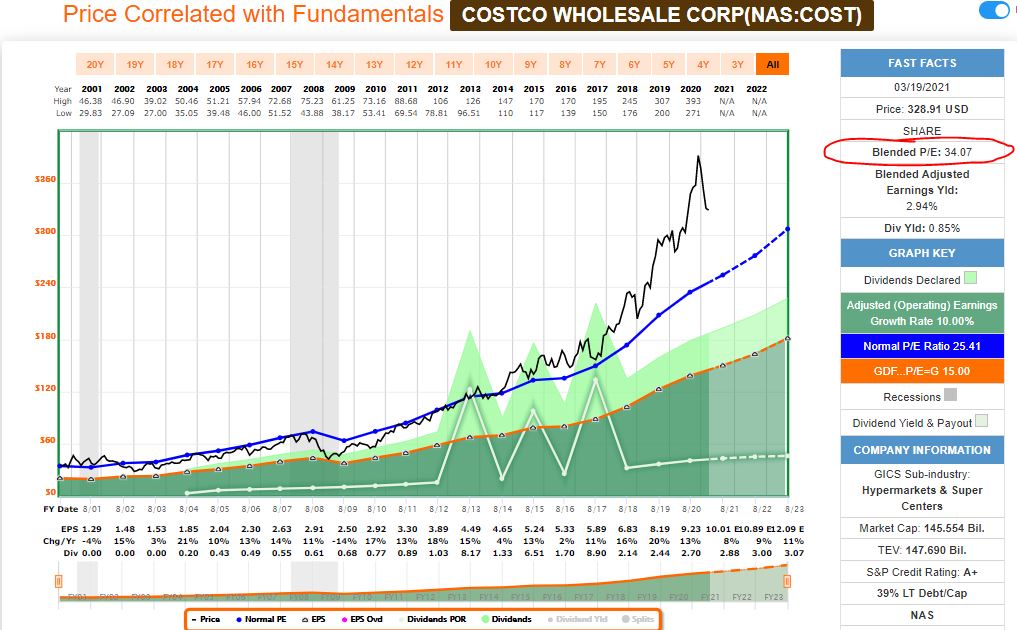

Using different time periods and metrics, one can get a lot of interesting valuation information about Costco from FAST Graphs.

Looking at the 20-year, adjusted-earnings back-test, COST certainly appears to be extremely overvalued — the blended P/E ratio of 34.07 is well above the 25.41 norm.

The blue line on the above graph represents the normal P/E ratio for the period; the black price line stayed very close to that this century’s first 14-15 years.

After that, Costco’s price remained fairly close to the blue line for a few more years before taking off in late 2017, and the P/E ratio has been well above 30 most of the time since.

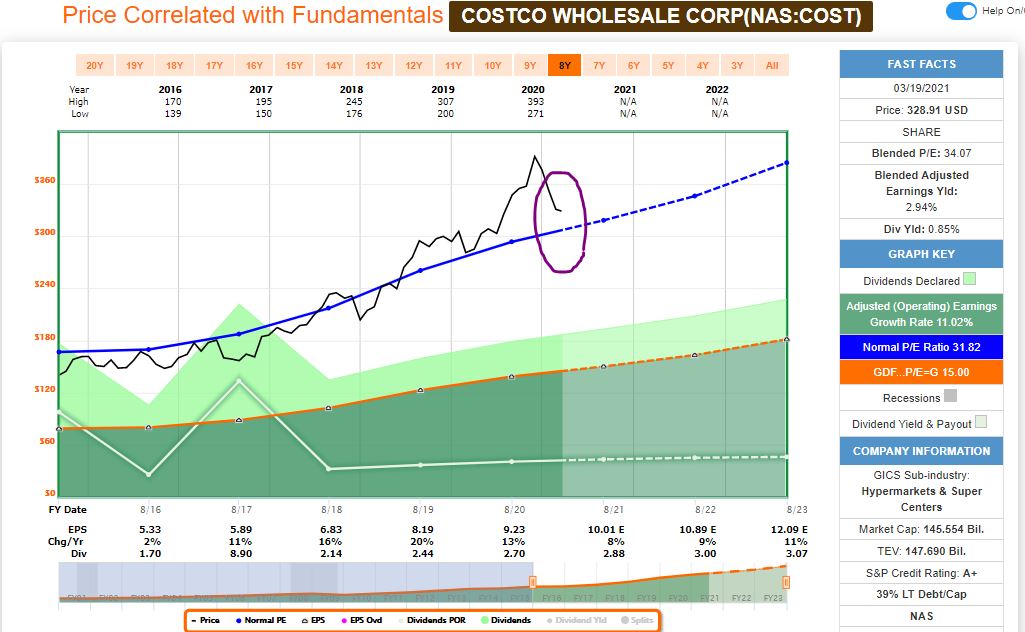

But some investors prefer not to look back so far, as the world — and the market — has changed a lot in the last two decades. Using a 6-year time frame instead, a 34 blended P/E ratio doesn’t seem so outrageous.

As the purple-circled area of the following graph shows, the end of the black line (representing the current price) sits only slightly above the blue line (representing the more recent P/E norm of about 32).

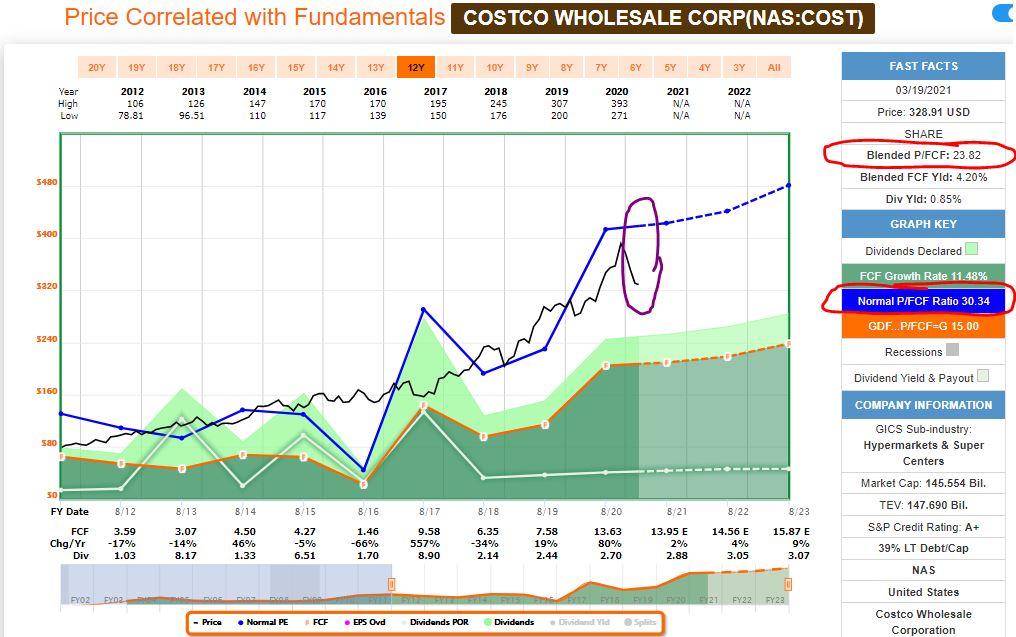

And finally, because Costco is a great cash-generating machine, let’s use free cash flow as another valuation metric.

The company’s current blended P/FCF ratio of 23.82 is well below the 10-year norm of 30.34. So by this measure, COST actually looks undervalued.

Taking in all the information available to me, I obviously don’t think COST is a bargain. But it is within a valuation range I am comfortable with, especially when talking about such a high-quality operation.

Still, it would be foolish to criticize investors who would prefer a larger margin of safety and who will wait to buy COST at a lower price (or not at all).

Dependable Dividend

At 0.9%, COST is one of the lowest-yielding companies in the Income Builder Portfolio.

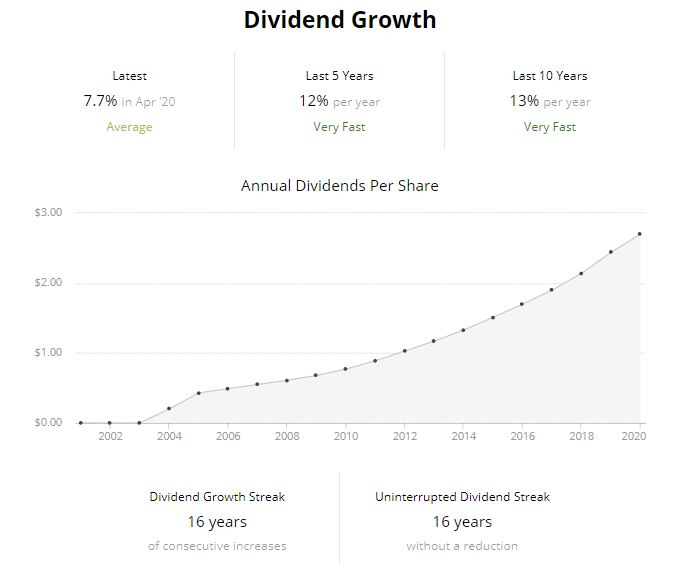

It nonetheless is a dividend growth stock, having increased its annual payout for 16 consecutive years. Most of the raises have been by double-digit percentages.

The following graphic from Simply Safe Dividends doesn’t show the four special dividends Costco has paid in the past decade: $7 per share in 2012, $5 in 2015, $7 in 2017, and $10 this past December. I never count on a special divvy, but I’m always delighted to get one.

SimplySafeDividends.com

Simply Safe Dividends gives the company a 99 “safety” score, meaning COST is an extremely reliable income producer thanks to its sound fundamentals, low payout ratio and reasonable debt load.

Costco routinely announces its annual dividend increase each April. I like to be conservative in my projections, so I’ll figure a 7% boost to .75/quarter.

In that case, our 3-share position would generate $2.25 in income, and that would be reinvested automatically (as per IBP rules) to buy an additional fraction of a share of COST.

That process will be repeated every quarter, not just with Costco but with every stock we own. No wonder we’ve given this project such a clever (and accurate) name.

Wrapping Things Up

There are so many reasons to like Costco as a business. In addition to those I mentioned in my previous article, here are a few others:

- The average wage for its hourly workers is an industry-high $24/hour, and they recently raised its minimum wage to $16, also tops. Costco consistently shows up on “best places to work” lists, and low employee turnover greatly helps the company’s bottom line.

- They have the best return policy in all of retail.

- They only increase membership fees every 5-6 years and they keep adding value for customers, so they have excellent retention and renewal rates.

- They haven’t raised the $1.50 price of their iconic hot dog-and-drink combo since first bringing the large, delicious franks to their warehouses in 1984. Co-founder Jim Sinegal once threatened to “kill” current Costco CEO W. Craig Jelinek if he ever raised the price.

Is COST stock pricey? Well, it sure isn’t cheap. But as a long-term investment gradually acquired via regular purchases over many years, I think Costco will prove to be a valuable part of the Income Builder Portfolio.

Note: COST also is held in the other public portfolio I manage for this site, the growth-and-income Grand-Twins College Fund. My next GTCF update will be published in early April. Until then, check out its home page HERE.

— Mike Nadel

This article first appeared on Dividends & Income

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.