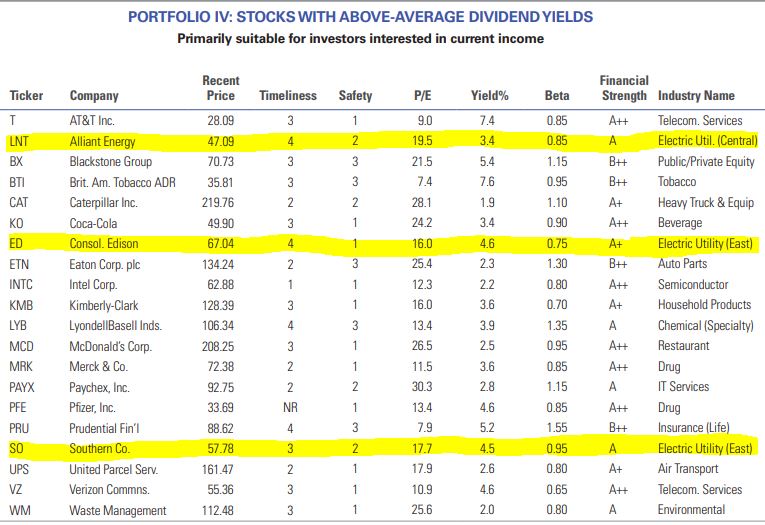

The well-respected stock market analysts at Value Line include three utilities in their model portfolio of “Stocks with Above-Average Dividend Yields.”

valueline.com

Value Line explains their appeal this way:

These holdings turned in respectable fourth-quarter results, and the outlook for 2021 remains positive. We think utilities should benefit from ongoing demand for power as the economy reopens. Incremental rate hikes and favorable tax treatments also should partially offset higher expenses in some categories. Meanwhile, substantial capital is being invested in renewable energy projects, and these initiatives, despite being initially costly and carrying some risk, should prove beneficial over time.

Specifically, Alliant Energy already heavily uses renewable assets and is actively investing in wind power. In addition, Consolidated Edison has an expanding solar initiative. Our utility issues have underperformed in 2021 so far, as investors have favored more dynamic equities. However, these stocks offer attractive yields, even in the current climate, and add stability to our portfolio, especially when the market runs into turbulence.

As the stock-picker and caretaker of DTA’s Income Builder Portfolio, all of that rings true for me.

Every stock has its role in a diversified portfolio. Generally, in a raging bull market, utilities will not keep up with the crowd; when Mr. Market turns bearish, however, utes normally will outperform.

And in good times and bad, most utilities pay attractive dividends.

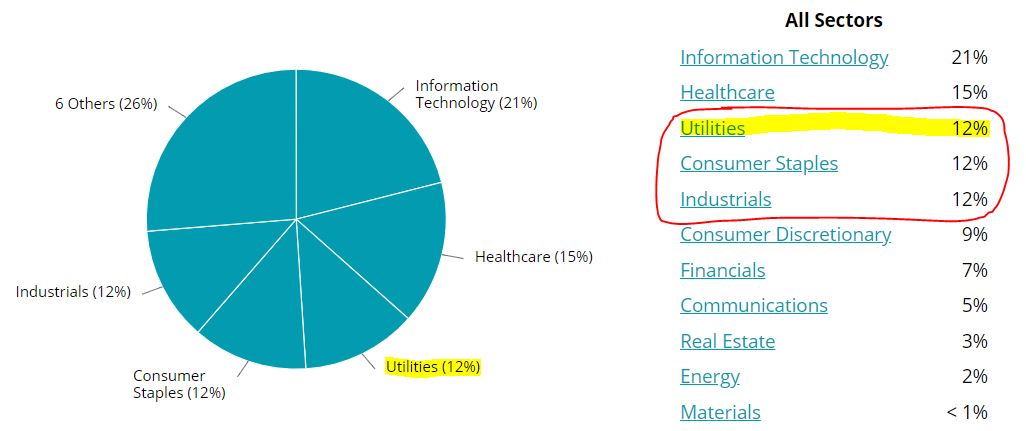

With that in mind — indeed, with “Income” being right in our portfolio’s name — the IBP owns five of them. Utilities are tied with Consumer Staples and Industrials as our third-most represented sector.

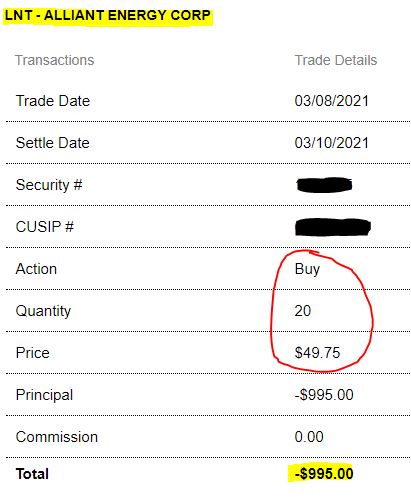

The IBP’s newest component from the sector is Alliant Energy (LNT).

On Monday, March 8, I executed a purchase order on Daily Trade Alert’s behalf for 20 shares of the Wisconsin-based electric and natural gas provider at $49.75 apiece.

The other four utilities in the Income Builder Portfolio are (in order of position size): NextEra Energy (NEE), Pinnacle West Capital (PNW), Avista (AVA) and American Electric Power (AEP). (Read about our most recent purchases of them HERE.)

Dividend Dandy

In my previous article, I mentioned several reasons for my selection of Alliant — and the company’s reliable, growing dividend ranked very high on the list.

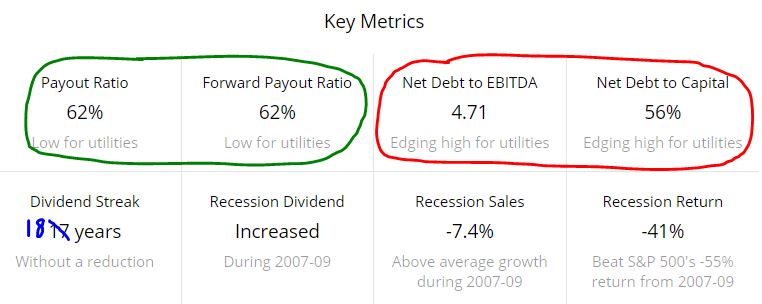

LNT yields 3.24%, and according to Simply Safe Dividends, most of the dividend-related metrics are positive.

I especially like the low-60s payout ratio (green-circled area of following graphic), as many utilities pay out more than 70% of their earnings in dividends. The red-circled area shows that the debt is a little higher than optimal — the lone negative in SSD’s analysis.

You’ll note that I used blue marker in the lower left square above to indicate that LNT has raised its dividend for an 18th consecutive year.

The 5.9% increase, announced in January, lifted Alliant’s annual dividend to $1.61 per share — meaning our position is expected to generate about $32 in income over the next year.

We will receive $8.05 in mid-May and that dividend will be reinvested back into the company, as per the IBP Business Plan. That will bring another .16 of a share into the portfolio.

Then, three months later, the new higher share total will generate slightly more income — a process that will be repeated over and over again, not only with LNT but with all 40 IBP positions.

And that, my friends, is why we gave this endeavor the name we did.

Analyze This!

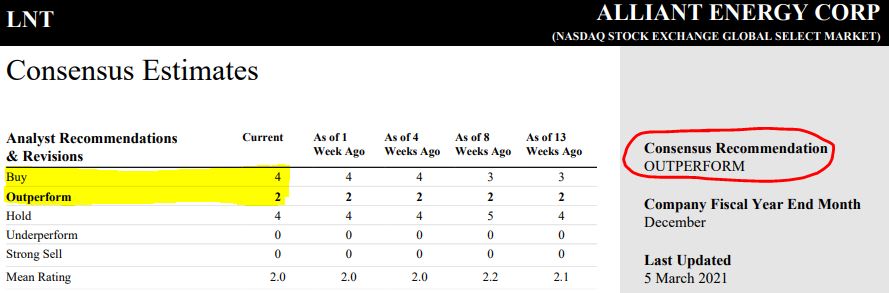

Professional market-watchers believe Alliant is a pretty good investment here. Reuters surveyed 10 analytical firms, with 6 rating LNT as either “Buy” or “Outperform.”

Reuters (via schwab.com)

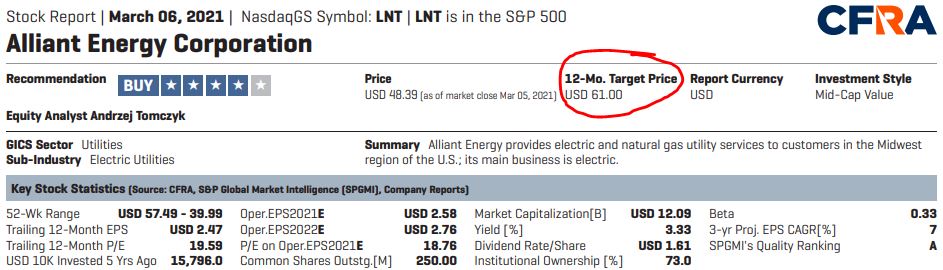

CFRA’s Andrzej Tomczyk believes Alliant’s price has a lot of room to run over the next year, setting a target price about 23% higher than what we just paid.

Tomczyk explained his analysis this way:

We think the recent share price implies sub-5% annualized earnings growth over the next five years, which we view as unwarranted given LNT’s clear drive towards expanding its renewable resource plays and its already established leadership position as a regulated wind operator. Currently, renewables make up approximately 20% of LNT’s total rate base, which is one of the highest percentages of renewable rate base among all U.S. utilities. We expect renewables will make up an even larger portion of the rate base as the company invests in solar projects for its Iowa and Wisconsin customers over the next three years. Separately, we believe the company is positioned well as more people stay at home because 46% of retail margins are residential.

Our $61 target is based on our dividend discount model, implying a 22.1x multiple on projected 2022 EPS, slightly above LNT’s three-year forward average (21.1x). Our model assumes annualized EPS growth of 7% (the midpoint of guidance) and a 5.1% cost of equity

Value Line’s analysts actually believe Alliant is more likely to produce a bigger gain in the next 18 months (yellow highlight) than in the next 3-5 years (red circle), which seems odds to me.

Valuation Station

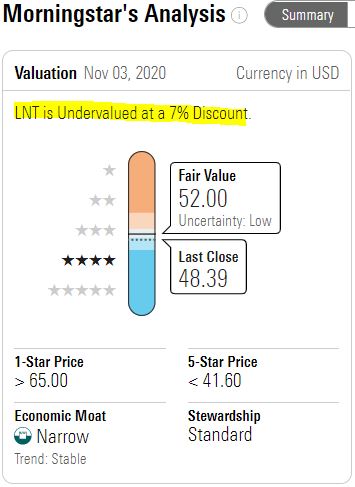

Morningstar Investment Research Center has calculated a $52 fair value for Alliant.

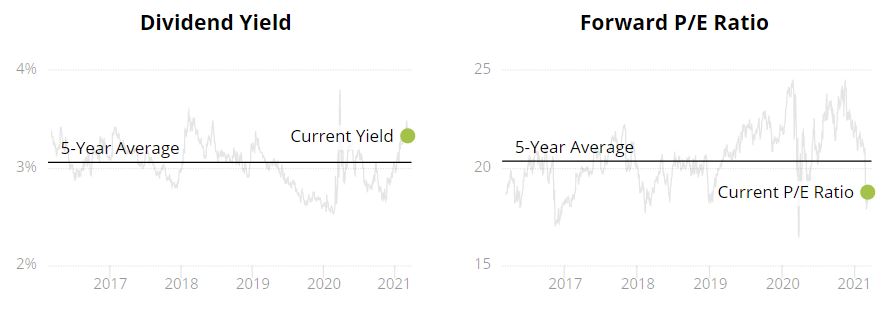

Comparing current yield to historic yield and forward P/E ratio to historic P/E ratio (see graphic below), Simply Safe Dividends says, “The stock may be reasonably valued … if you believe its health and long-term prospects are solid.”

SimplySafeDividends.com

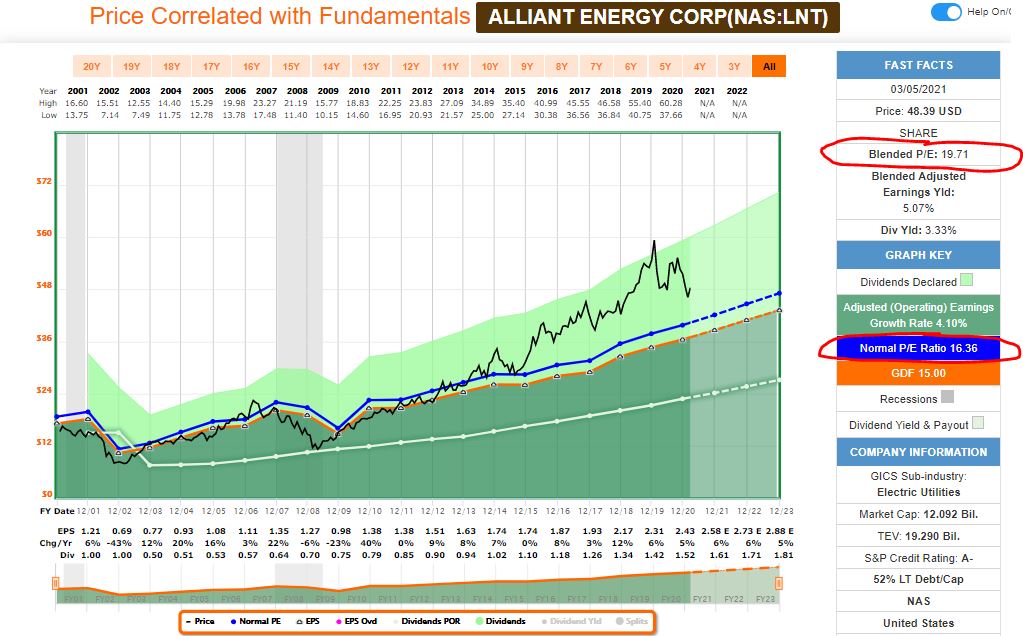

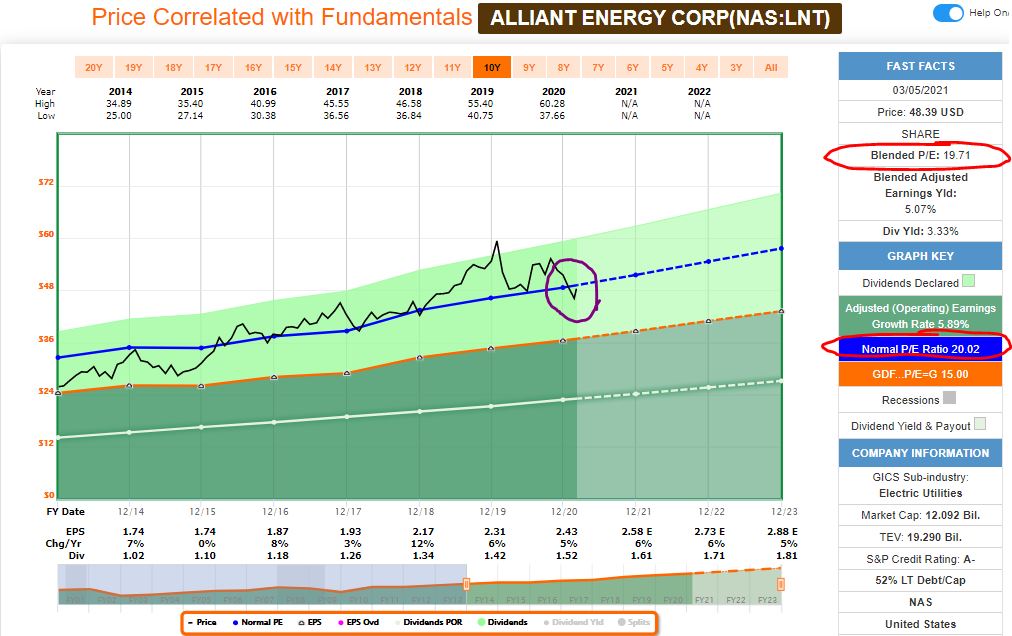

I am including two FAST Graphs illustrations to demonstrate how valuation results are affected by the time frames one uses.

The first, going all the way back to the start of the millennium, makes it seem LNT is quite overvalued compared to its norm for the period. I used red circles to highlight the current “blended P/E ratio” of 19.71 and the 16.36 norm.

But so much has happened over the past two decades, including three recessions and one of the longest bull markets ever, that some might think a shorter-term view is more relevant.

Going back only to the end of 2013, LNT now appears fairly valued at worst. The purple-circled area shows that the current price (black line) is a tad below the historic P/E ratio (blue line).

Wrapping Things Up

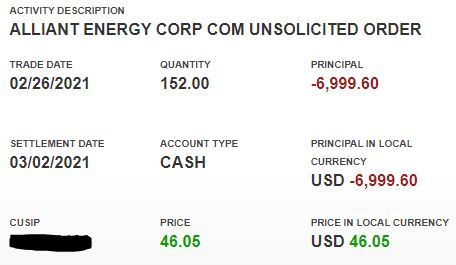

On Feb. 26, I bought LNT for my personal portfolio at about $46/share — a price I liked because it was the 3.5% yield mark as well as approximately 18 times this year’s projected earnings.

With the Income Builder Portfolio, however, my writing schedule dictated that I wait about two weeks to buy it — resulting in us having to pay about 8% more.

In the past, such time discrepancies also have worked out the other way. So I don’t sweat it too much because these things tend to even out. And under $50 still represents a reasonable price for LNT.

I will be building up the IBP’s position over time, and probably will pay both more and less along the way. Regardless, I will be happy the portfolio will have a solid position in this high-quality utility.

My colleague Dave Van Knapp also has LNT in his Dividend Growth Portfolio, which can be seen HERE.

Note: The IBP is one of two real-money portfolios I manage for this site. The other is my Grand-Twins College Fund, which includes both growth stocks and companies favored by income investors. Check it out HERE.

— Mike Nadel

This article first appeared on Dividends & Income

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.