Zoom Video (NASDAQ:ZM) will go down as a stock to remember for many years. After going public in 2019, ZM stock faced some investor skepticism due to its premium valuation.

However, it checked all the boxes for growth investors.

It had (and still has) strong revenue and earnings growth, was profitable and free cash flow positive, and had a strong balance sheet. The only thing not to like here was the valuation. But why should ZM stock come at a discount if it had all of these positives?

That was the case bulls were making as we entered 2020. Then the novel coronavirus happened.

Covid-19, Zoom and The Future

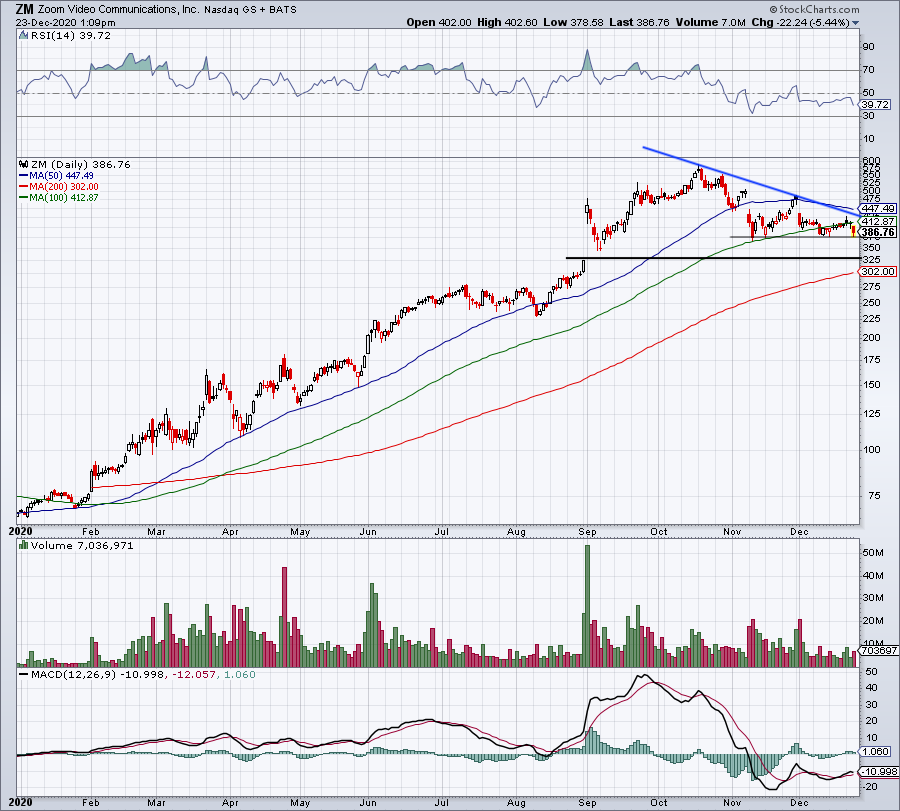

Shares rallied more than 750% from the start of the year to the Oct. 19 high. Although ZM stock has been pulling back, currently down 34.7% from those highs and flirting with a potential breakdown.

If bulls are lucky, that’s exactly what will happen, given them a better buying opportunity.

Because Covid-19 forced many meetings into the virtual space — be it for business or for family and friends — Zoom Video engulfed unheard of levels of growth. Short of a pandemic, there was simply no other way for the company to realize so much demand so quickly.

For example, analysts were expecting about $610 million in sales and earnings of 27 cents per share this year. Those estimates now sit at $2.58 billion and and $2.90 per share, respectively.

So earnings estimates have climbed 10-fold, while revenue estimates have increased about four-fold. That is absolutely astounding.

Moving Forward With ZM Stock

After such a big move in a short amount of time, ZM stock isn’t an easy one for investors. That’s particularly true because of the optics, which is that Zoom Video is up because of Covid-19.

That is not the case.

Covid-19 did accelerate Zoom’s business and act as a major positive catalyst. However, Zoom only needed the pandemic to fuel existing growth and a trend that was already in place. That is the major difference.

PPE manufacturers and other companies created new business lines for the pandemic. Those will see an immediate decline once Covid-19 is the rearview mirror. Imagine how many masks people will be buying in a pandemic-free world. Likely not many.

However, it’s not hard to imagine why Zoom will sustain its business. That’s because it’s video conference platform is:

- Cheaper than in-person meetings, especially for traveling

- Faster due to less travel time (be it to the conference room or across the country)

- More convenient

Zoom lets a company or group meet quickly, conveniently and more efficiently than an in-person meeting. Imagine having to go to the airport, fly to a different city or country, give a presentation or attend a meeting, get a hotel and various meals and then fly home.

That is so cumbersome and expensive vs. logging into Zoom and doing the exact same thing. When a product makes business more efficient, companies want it. That’s exactly why analysts’ expect the business to continue humming along, with or without Covid-19 in the headlines.

Revenue is forecast to grow 315% this year to almost $2.6 billion. Analysts expect another 38% growth in FY 2022 (next year) to $3.56 billion. Two-year revenue estimates swell to $4.3 billion.

The fact that Zoom isn’t giving back this year’s growth is wildly impressive.

Bottom Line on Zoom Stock

Source: Chart courtesy of StockCharts.com

Source: Chart courtesy of StockCharts.com

Source: Chart courtesy of StockCharts.com

Source: Chart courtesy of StockCharts.comI think a lot of investors are being short-sighted when it comes to Zoom regarding its growth being tied solely to Covid-19. With that being said, the valuation is a concern for many.

With a $110 billion market capitalization and forecasts for “just” $3.56 billion in sales next year, shares are not cheap at ~32.5 times forward revenue estimates. Maybe in today’s world, 30+ times forward earnings is cheap, but traditionally it is not.

That said, it’s hard to ignore a new platform that has shown staying power. As a result, I think investors can start to nibble. More conservative investors will likely want to wait for more pain in ZM stock and that’s fine too.

A look at the chart above highlights the $325 level as somewhat prominent. There the stock has a large gap that’s waiting to be filled. Of course, we don’t know if it will ever be filled, but if it is, it will mark about 15% more downside from current levels.

Perhaps that will time up with a test of the 200-day moving average, giving investors another reason to pull the trigger.

At $325, ZM stock will be down about 44% from its all-time high. It will have also filled that big gap and will trade with a market cap of about $93.5 billion. That would leave Zoom trading at about 26 times forward revenue, which is a bit more palpable.

Here’s the bottom line: It’s not a question of “if” ZM stock is a buy, it’s a question of where investors feel comfortable owning it.

— Matt McCall and the InvestorPlace Research Staff

Silicon Valley venture capitalist Luke Lango says this little-known Apple project could be 10X bigger than the iPhone, MacBook, and iPad COMBINED! Investing in Apple today would be a smart move... but he’s discovered a bigger opportunity lying under Wall Street’s radar -one that could give early investors a shot at 40X gains! Click here for more details.

Source: Investor Place