When my wife and I are on a long road trip and we start feeling hungry, we, like millions of other travelers, look for the next set of Golden Arches off the highway.

After arriving at McDonald’s (MCD), I usually opt for something cheap and familiar, such as a double cheeseburger and small fries. Roberta, ever sensible and health-conscious, goes for a salad.

Or at least she used to.

Due to the global coronavirus pandemic, McDonald’s has simplified its menu somewhat to reduce costs and to account for increased traffic at drive-thru windows … and salads didn’t make the cut.

Also axed was all-day breakfast, one of the initiatives that had been credited with helping the company escape its doldrums a few years back.

Judging by the results of the company’s most recent earnings call, my wife was one of the few folks disappointed by the absence of salads from the menu.

And though some have grumbled about no longer being able to scarf down McGriddles and Egg McMuffins at suppertime, that also doesn’t seem to have hurt the company’s bottom line.

McDonald’s easily beat analyst expectations in the third quarter, when earnings and sales actually surpassed pre-pandemic levels.

MCD quarterly earnings (left) and sales (right). (Graphic by Simply Safe Dividends)

Such resiliency is one reason I have decided to add to the MCD position in DTA’s Income Builder Portfolio.

After the market opens today, I also will execute orders on Daily Trade Alert’s behalf for relatively small purchases of the IBP’s two real estate investment trust holdings, Realty Income (O) and Essex Property Trust (ESS).

Oldie But Goodie

While O and ESS only became IBP components in recent months, we bought McDonald’s way back in the portfolio’s first year.

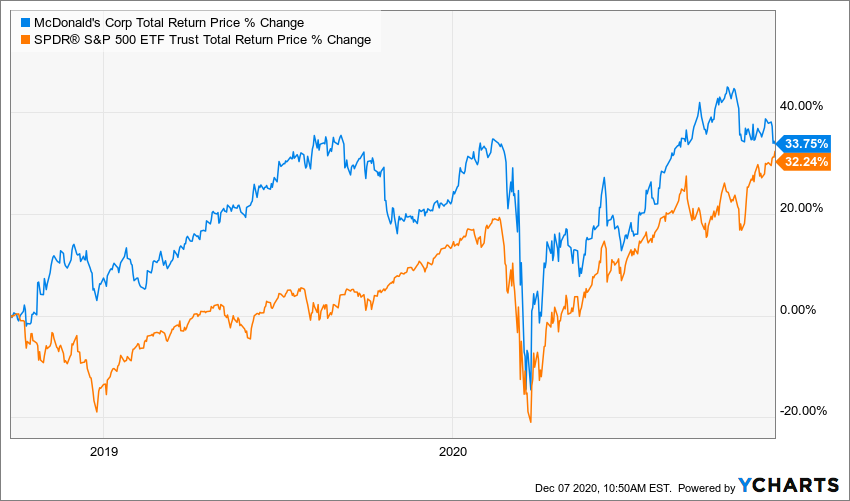

Since we purchased MCD on Sept. 26, 2018, it has had a total return of 34% — even better than the overall market, which keeps hitting new all-time highs.

I had been wanting to add to the MCD position for quite awhile, but I instead chose other companies for one reason or another.

One reason: McDonald’s has become overvalued, a victim of its own stock-price appreciation.

When possible, I prefer fairly valued companies — which helps explain why I’m also selecting add-ons to O and ESS instead of putting all $1,000 of DTA’s semimonthly allocation into MCD. (I will discuss valuation more thoroughly in my post-buy article, which will be published on Wednesday, Dec. 9).

Tough Task For MCD’s CEO

As if the fallout from that scandal wasn’t enough, Kempczinski soon had to deal with the pandemic.

He and his team has come up with an “Accelerating the Arches” strategy that focuses on marketing, the company’s core food offerings, and the “3-Ds”: digital, delivery and drive-thru.

Morningstar Investment Research Center, which added McDonald’s to its Dividend Select Portfolio earlier this year, is impressed:

We believe the key takeaway for investors after McDonald’s third-quarter update and investor day is that the company remains well positioned for post-pandemic market share gains. … We believe various components of its “Accelerating the Arches” plan position McDonald’s to meet (and likely exceed) its 2021–22 guidance for mid-single-digit systemwide sales growth, operating margins in the low to mid-40s, annual general and administrative spending of around 2.3% of system sales (versus 2.2% in 2020), capital expenditure of $2.3 billion, and implied free cash flow of $5.5 billion–$6.0 billion.

The REIT Stuff

Both Realty Income and Essex Property continue to progress nicely since the market’s “pandemic plunge” last March.

The vast majority of their tenants are paying rent in full and on time, their balance sheets look solid, and I remain high on their future prospects.

Because we added O to the IBP just last month, and our ESS position was initiated in August, what I said about them in recent articles is still valid today. (See the Realty Income purchase HERE and the Essex buy HERE.)

That’s why I’ve been focusing primarily on McDonald’s in this piece.

Delicious McDivvies

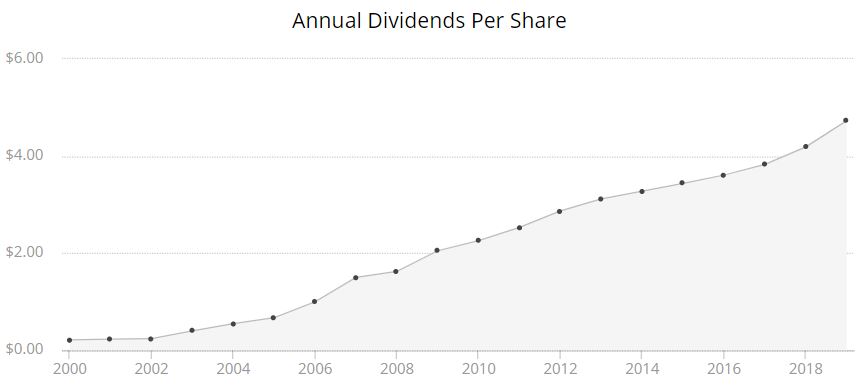

A Dividend Aristocrat, McDonald’s has grown its annual payout to shareholders for 45 consecutive years.

A few days before we bought MCD in 2018, the company had announced a 14.9% dividend raise.

McDonald’s has increased its dividend twice since then — by 7.8% in 2019, and by 3.2% for the upcoming 12 months. Its first payment under the new quarterly amount of $1.29/share will be made on Dec. 15.

The 3.2% hike is the company’s smallest ever. And though I always want more, more, more — don’t we all? — it seems prudent to be conservative during a global pandemic that has seriously wounded the restaurant industry.

I was heartened by this slide from last month’s Investor Update presentation:

When a company with a nearly half-century history of growing its dividend says paying divvies is one of its top priorities, that’s good enough for me.

Essex Property Trust and Realty Income also are Dividend Aristocrats, so the decision to add to all three positions figures to have a positive long-term effect on the IBP’s income stream.

Wrapping Things Up

The Income Builder Portfolio has stakes in 37 companies (see them HERE), and Essex, Realty Income and McDonald’s are three of the smallest positions.

It’s time to add to their share counts. Heck, for MCD, it’s long past time to make another buy.

No, McDonald’s is not delivering salad and all-day breakfast to their customers right now (and perhaps never again), but the company rarely fails to deliver for investors.

That’s why I own a large MCD position myself, why it’s in the other real-money portfolio I manage — the Grand-Twins College Fund — and why I selected McDonald’s for the IBP in the first place.

As always, investors are urged to conduct their own due diligence before buying any stocks.

— Mike Nadel

This article first appeared on Dividends & Income

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.