With the market continuing its giddy, post-election, fingers-crossed-for-coronavirus-vaccine climb, finding a fairly valued, high-quality stock is a challenge.

Detecting such a company in the Consumer Staples sector — especially if it isn’t in an industry facing extreme headwinds — is tougher still.

For example, I put the following filters into the Simply Safe Dividends screener:

- Consumer Staples sector

- Dividend yield of at least 3%

- P/E ratio below or in-line with 5-year average

- Most recent dividend raise of at least 5%

- Annual dividend growth streak of at least 5 years

- SSD dividend safety score of 81 or better (“Very Safe”)

When I hit the button, here’s what the search revealed:

Of course, I could have played around a little with the categories and found a few “investable” stocks. Even if I had gone down a level in every category, however, only 11 companies in the staples sector would have matched — and several of those look overvalued.

So for my next selection for DTA’s Income Builder Portfolio, I decided to go outside the box with a mid-cap stock that has been available to investors for less than a year.

But I’m really not going that far outside the box; this company’s brands are familiar to just about every American adult.

reynoldsconsumerproducts.com

At some point during today’s trading session, I will execute a purchase order on Daily Trade Alert’s behalf for about $1,000 worth of Reynolds Consumer Products (REYN).

The History

Reynolds Wrap was first introduced in 1947. My grandmother used it to cover pies she baked, my mother wrapped leftovers in it, the product is in my cupboard now, and my grown kids have it in their kitchens, too.

The business grew and became Reynolds Metals Company. Over the years, it expanded its product line significantly before being acquired in 2000 by Alcoa (AA).

Alcoa sold its packaging and consumer businesses in 2008 to New Zealand-based Rank Group, which is owned by that country’s richest man, Graeme Hart. Rank then acquired Pactiv Corp., maker of Hefty trash bags, combining those operations under the Reynolds umbrella.

Finally, in January of this year, Reynolds became a publicly traded corporation. Hart retained 77% of Reynolds’ voting rights through a subsidiary he owns.

Rapping About Reynolds

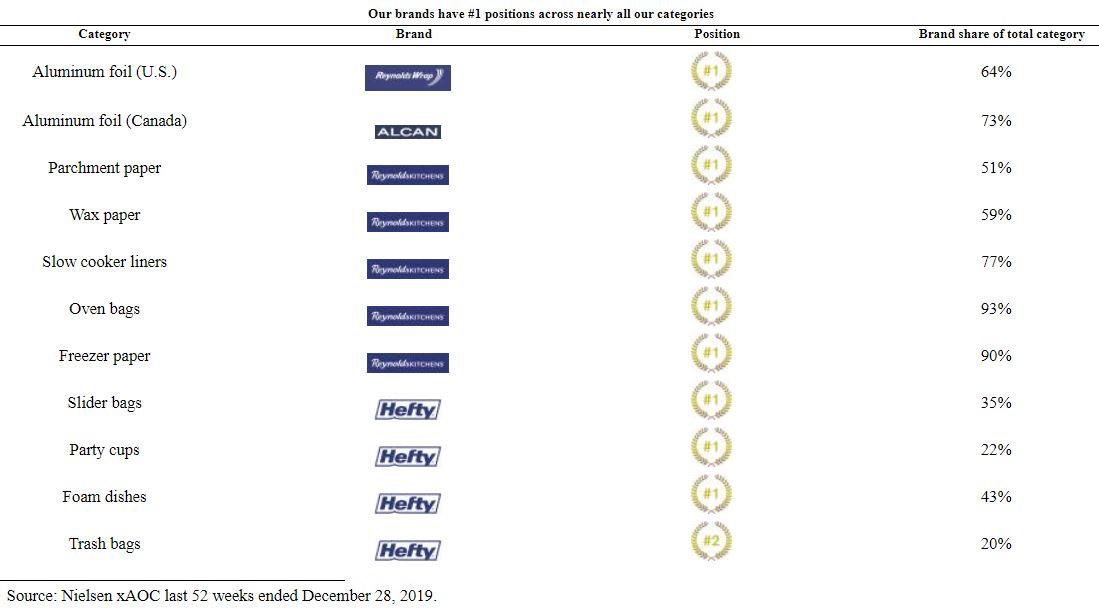

REYN operates four divisions: Reynolds Cooking & Baking (which includes the ALCAN brand in Canada and the Diamond brand outside of North America), Hefty Waste & Storage (which includes trash bags and slider-top storage bags), Hefty Tableware (disposable plates, cups and cutlery), and Presto Products (mostly store brands).

Most of the company’s top brands rank No. 1 in their product categories, often by huge margins.

Reynolds’ Form 10-K filing with SEC

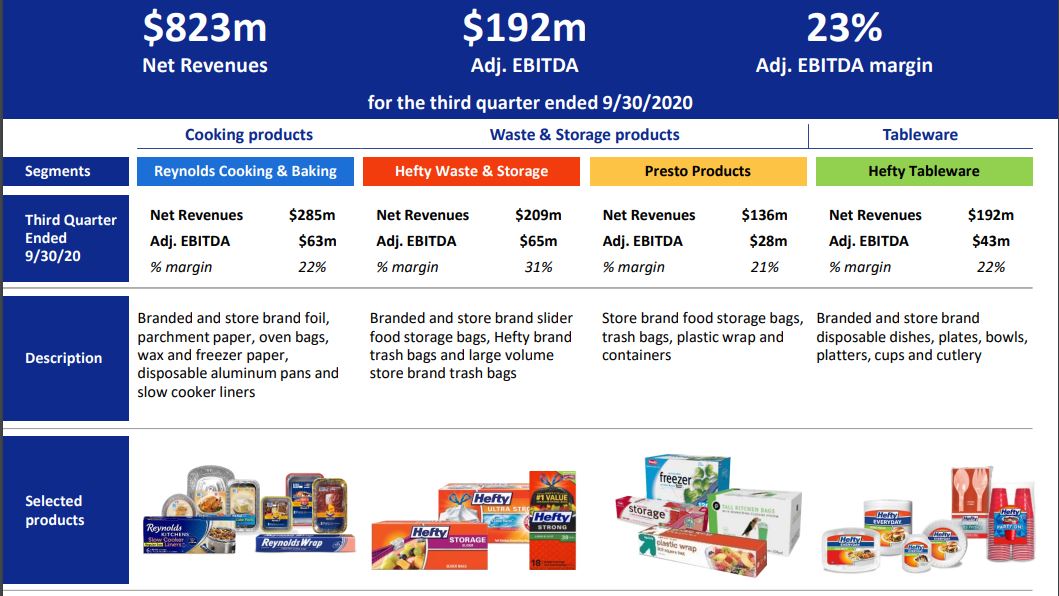

Reynolds presented its third-quarter report on Nov. 11, showing quite well.

Revenue of $823 million was an 11% improvement over Q3 2019 and beat analyst estimates by $26M, and REYN also easily beat earnings estimates.

Reynolds’ Q3 earnings presentation

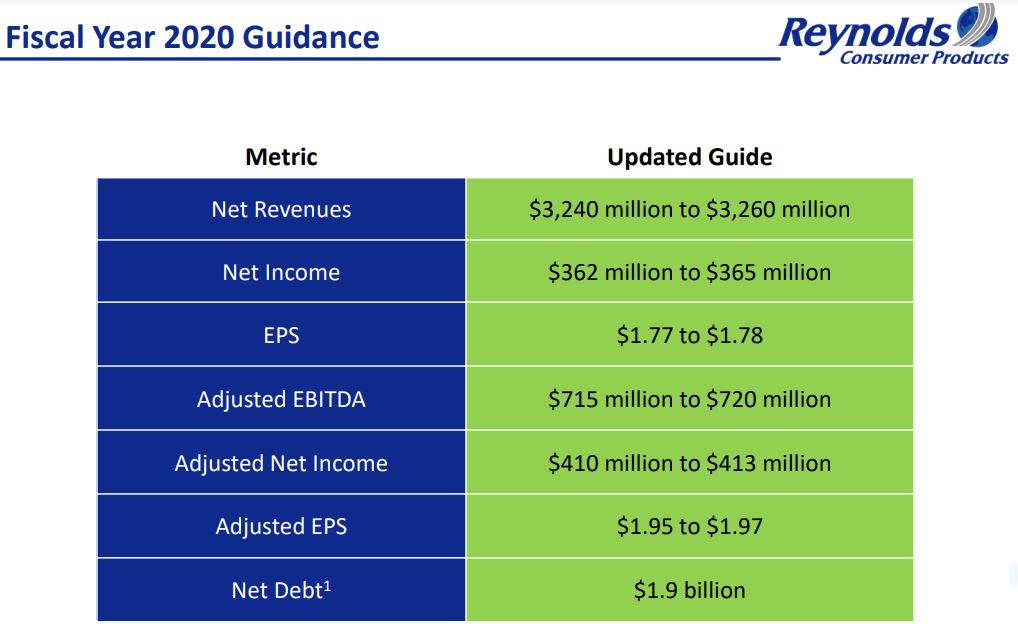

Looking ahead, the company estimated year-over-year “mid-single-digit” revenue growth for Q4.

Reynolds also gave strong full-year guidance, updating its previous outlook with raises in most metrics.

Reynolds’ Q3 earnings presentation

Analysts at Credit Suisse, who early in the year called REYN their “top defensive pick,” were impressed with the report — especially given that the global coronavirus pandemic has been getting worse.

Growth was broad-based, reflecting high demand, new product introductions, increased capacity, and sequential improvement in restaurants/foodservice trends. … Management showed confidence that the revenue profile of its categories is now structurally higher. … Reynolds is beneficiary of “stay-at-home” cooking and eating. The new capacity additions are high-quality, margin accretive gains. Its industrial heritage means dollar profits-focused company, which should be able to weather commodity headwinds.

Reynolds announced its first quarterly dividend shortly after its initial public offering, 15 cents per share. The company then raised the amount to 22 cents for its August payment, and kept that same amount for November.

Extrapolating the dividend to 88 cents per year, REYN has a yield just under 3%.

During the Nov. 11 earnings call, CFO Michael Graham said: “We remain committed to cash returns, including a dividend payout ratio of approximately 50% of net income, with dividends growing over time … “

So while there is no dividend “promise,” there is a commitment, and I like that.

Wrapping Things Up

Given its newness as a publicly traded company, Reynolds does not carry many of the quality ratings common to the Income Builder Portfolio’s other 36 components.

For example, REYN gets a sub-investment-grade BB credit rating from Standard & Poor’s, and mediocre Safety (3) and Financial Strength (B+) scores from Value Line.

Morningstar doesn’t cover the company yet, so REYN has no moat or stewardship ratings from that analytical firm. And Simply Safe Dividends still hasn’t assigned it a safety score.

Nevertheless, we are not talking about a highly speculative, fledgling operation here. Reynolds has been around for generations and makes top-selling, iconic kitchen products.

It really doesn’t take a wild imagination to believe Reynolds Consumer Products will be a good long-term investment for the IBP.

My next article, to be published on Wednesday, Nov. 18, will dive into REYN’s valuation and other pertinent information.

As always, investors are strongly urged to conduct their own due diligence before buying any stock.

— Mike Nadel

This article first appeared on Dividends & Income

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.