Four years ago, I published an article detailing how a young upper-middle-class professional could quit working and still survive on dividends alone in just five years.

It was a claim that many folks thought was impossible to achieve (and they told me so in the comments!).

But history has proven that, in fact, it was true.

Today I want to show you how following the advice I gave back then would have produced financial independence (or an income stream that could cover basic needs) in just five years—and how you can replicate that same success today.

How It Works

Back then, I made three arguments:

- A young professional earning $70,000 a year and, being very disciplined, managed to save about two-thirds of that income, could use the stock market to build a substantial nest egg in half a decade.

- They could invest in the stock market and make an 8.2% annualized return over those five years. And they could do this by buying an index fund.

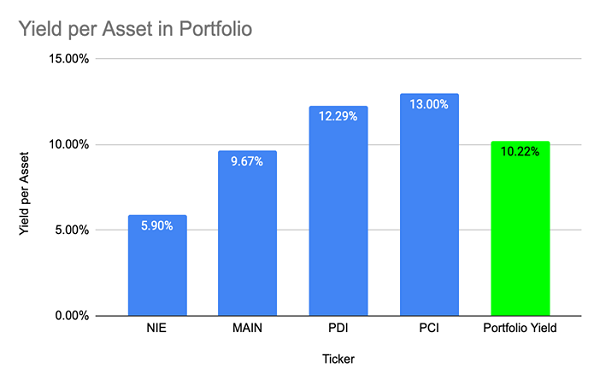

- Then, at the end of five years, they could rotate their principal and gains into a portfolio of four assets that provides a sustainable high income stream. These were Main Street Capital (MAIN), the AGIC Equity & Convertible Income Fund (NIE), the PIMCO Dynamic Income Fund (PDI) and the PIMCO Dynamic Credit Income Fund (PCI).

Let’s go through the above, then track how our hypothetical early retiree’s portfolio is doing four years into my plan.

No. 1: Annualized Return

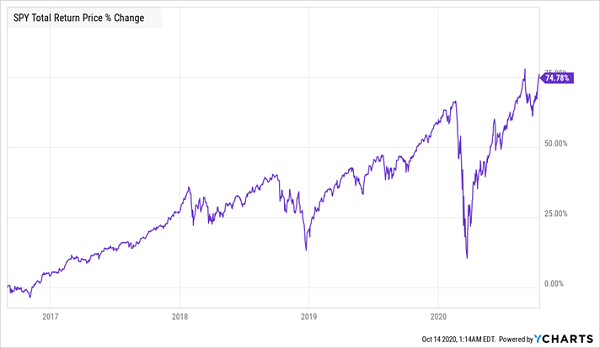

In the four years and one month from then to now, the S&P 500 SPDR ETF (SPY) has returned 74.8% in total, or 14.7% annualized.

Strong Gains Despite Challenges

As this is significantly higher than the 8.2% growth rate planned, even with a global pandemic, it’s easy to say that history has proven this expectation to be reasonable.

No. 2: Growing the Nest Egg

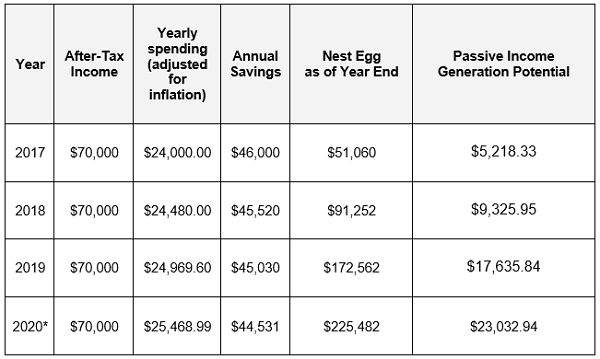

Here’s how our investor’s nest egg would have grown over the time they were building it via the index fund, showing the market’s actual yearly return in dollars and cents.

On the right, we see how much each year’s year-end balance would produce in dividend income once the investor switched over to our four-asset high-yield portfolio. This hypothetical dividend income is based on the 10.22% average yield our four-asset portfolio offers, which is not far from the 10.34% it yielded in 2016.

*2020 numbers are based on current market value

*2020 numbers are based on current market value

Factoring for inflation over these four years, we come to a spending rate of $25,469, which would require total savings of $249,207 for our investor to maintain in retirement. At this savings rate, our investor will have that much in six and a half months, just on savings alone. If stocks rise at all, our investor will have that much even sooner.

At that time, the investor can then sell her index-fund holdings and rotate into the high-income assets that will give her a stable income stream to help fund her early retirement.

Source: CEF Insider

Source: CEF Insider

(These yields are based on each stock’s regular and special dividends, based on the current regular distribution rate and special dividends paid in 2019.)

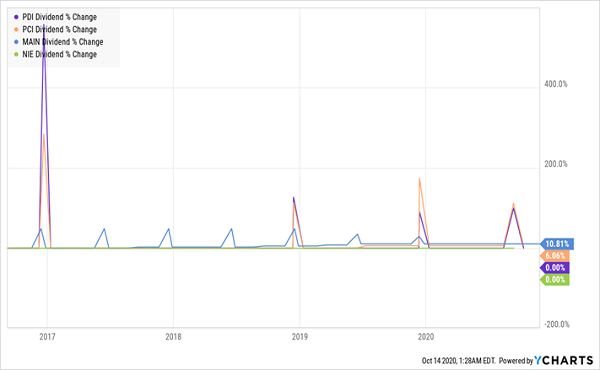

None of these assets have cut dividends in the last four years—a concern of readers back then. And, in fact, we have seen modest growth in regular distributions:

A Steady Stream of Regular, and Special, Dividends

Conclusion: High-Yield Investing Can Get You Financially Independent Fast

Four years ago, I wrote that an investor could quit working and still have a passive income stream to maintain their lifestyle with just $330,000; however, as we can see above, it could actually take much less: below $250,000.

But that $330,000 would provide a buffer; with that amount, you’d need a yield of just 7.7%, so you could spread your nest egg out among other assets (a lack of diversification in this portfolio is an issue with our four-asset high-income portfolio).

Another alternative would be to stick to these four stocks and funds, withdraw only 7.7% and reinvest the rest of the dividend cash as it comes in. The elimination of brokerage fees since 2016 at many online firms would make this easy to do on a monthly basis.

The bottom line? With a portfolio of high-yielding stocks and funds, it is possible to cover off your bills in retirement on dividends alone—and on a lot less than most people think.

— Michael Foster

These “Retirement-Ready” Funds Make Money 98.4% of the Time [sponsor]

Three of the investments in our “4-fund” retirement portfolio are closed-end funds (CEFs)—high-paying funds that give you another level of safety … especially if you’re investing for the long haul (and with 8%+ dividends common in the CEF world, you should be!).

I’m talking about a shocking fact I’ve recently discovered—a “profit rate” among CEFs that’s truly jaw-dropping. I’ve never seen anything like it, in bonds, stocks, real estate or anything else.

Get this: of the 326 CEFs that are a decade old (or older), only 16 have lost money in the last 10 years.

That’s a 95% win rate!

There’s more: of the 16 CEFs that did lose money, all but 5 were in the energy sector. Dump those 11 laggards and these CEFs’ win rate jumps to an incredible 98.4%!

That’s right: this group of incredible investments made money 98.4% of the time! And because these statistics include dividends, you’re getting much of your return IN CASH with these CEFs.

My 5 Top CEFs Could Pay You $41,000 in Dividends in Just 12 Months

The best news is, my 5 top CEFs to buy now yield in outsized 8.2% today, and thanks to their bizarre discounts, they’re primed to jump 20%+ in the next 12 months.

A $500K nest egg generates $41,000 in dividends! And that’s on top of the $100,000 in projected GAINS I’m calling for here!

Don’t miss your chance to pick up these 5 remarkable funds while they’re cheap. Get everything you need to know—names, tickers, complete dividend histories and more—right now.

Source: Contrarian Outlook