This article first appeared on Dividends & Income

I’m not the brightest bulb in the candelabra, but even I’m smart enough to know to keep doing something when it’s working spectacularly.

Case in point: the Home Depot (HD) and Medtronic (MDT) positions within DTA’s Income Builder Portfolio.

A brief history …

- Oct. 19, 2018: We bought 6 shares of Home Depot, the world’s largest home-improvement retailer, at $179.79 apiece.

- Jan. 15, 2019: We purchased 12 shares of Medtronic, the biggest pure-play medical device company, at $86.49 each.

- March 1, 2019: We divested our entire MDT position and used the proceeds to double our stake in HD, buying 6 shares at $183.81 apiece. We did this after learning that our brokerage, Schwab, would not automatically reinvest MDT dividends, as called for in the IBP Business Plan. (Medtronic is based in Ireland, and Schwab does not allow “dripping” of companies with non-U.S. headquarters.)

- June 23, 2020: We again bought MDT, paying $94 apiece for 11 shares. We were willing to do so because the brokerage introduced a product called “Schwab Stock Slices” that lets investors buy partial shares (or “slices”) of companies. This would enable us to “self-drip” MDT, using even small dividend amounts to buy fractions of shares, as shown in the following graphic.

So although Medtronic and Home Depot are very different companies, they always will be linked in Income Builder Portfolio lore.

And given the performance of both companies since we’ve owned them, I have decided to keep a good thing going.

Later today, I will divide our semi-monthly $1,000 allocation equally between HD and MDT, executing purchase orders of both companies on Daily Trade Alert’s behalf.

HD = Hundred Dollars (More)

HD has given us 100 reasons to be happy, as shares are trading about $100 higher than the prices we paid in our two purchases of the company; our total return on the position is a market-crushing 60%.

Had we purchased the SPDR S&P 500 Trust ETF (SPY) the same days we bought Home Depot, total return would have been only 24%.

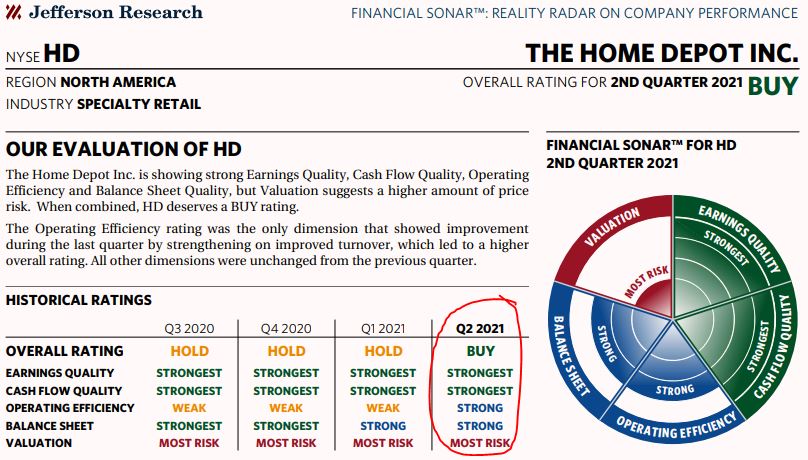

Our reasons for wanting more Home Depot are the same as when I first selected the company for the IBP two years ago: It is a very high-quality business that has outperformed the market for decades and has been growing its dividend for years.

Since then, HD has increased earnings by 60%, revenue by 45% and dividends by 46%.

Rather than hurt Home Depot, the global COVID-19 pandemic has served as a catalyst, as more people are staying home and doing projects for their dwellings.

And Morningstar, which has chosen HD for its Dividend Select Portfolio, does not believe that the end of the pandemic (whenever that comes) will hurt the company at all:

As the world’s largest home improvement retailer, Home Depot captures significant

efficiency gains through its large scale. During the COVID-19 pandemic, its stores have

been seen as essential, helping buoy financial results. Home Depot should capture

a significant portion of the pent-up demand when the economy reopens. Housing

investment should also be strong in the years ahead, providing a long tail to growth.

The biggest knock against Home Depot’s stock is that it is pricey.

The following “Financial Sonar” from Jefferson Research reflects the company’s quality but also shows the analyst believes shares are very expensive.

I will discuss the valuations of both Home Depot and Medtronic in greater detail in my post-buy article, which is scheduled to be published on Wednesday, Oct. 7.

Medtronic Showing Improvement

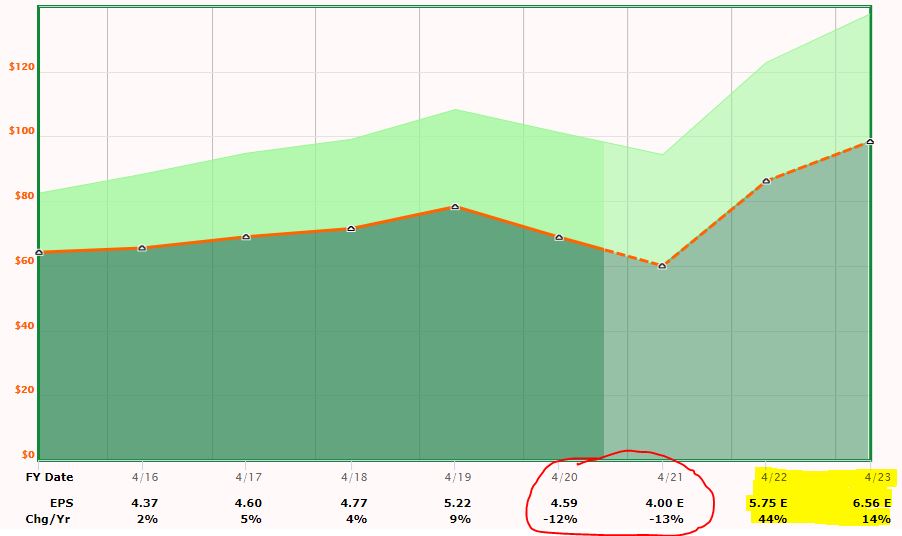

Because surgeries were put off as hospitals dealt with coronavirus patients, Medtronic saw double-digit-percentage decreases in sales and earnings during the fourth quarter of fiscal 2020 (which ended April 30) and Q1 2021 (ending July 31).

Things already were starting to improve in the most recent quarter, as MDT handily beat analyst forecasts.

And as the yellow-highlighted area of the following FAST Graphs image shows, earnings are expected to soar the next couple of years.

Medtronic gave income-centric investors reasons to cheer in May when it announced a 7.4% dividend increase; many companies have reduced or even eliminated their dividends during the pandemic.

It’s the 43rd consecutive year this Dividend Aristocrat has raised its payout to shareholders.

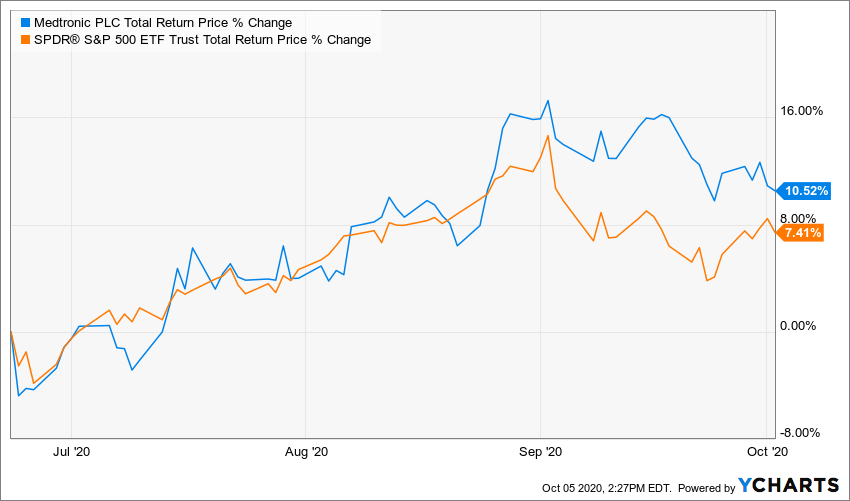

Despite the coronavirus-related headwinds, MDT has a 10.5% total return since we added it back to the Income Builder Portfolio on June 23 — besting the overall market by 3 points.

I believe part of the reason for those gains is that investors are impressed with management’s focus on trimming costs wherever possible while simultaneously putting more money into research and development.

Wrapping Things Up

When we add shares of Home Depot today, it will become one of the IBP’s largest holdings by value. Medtronic, meanwhile, will go from one of our smallest to a medium-sized position.

That’s all great news, as I am always looking to improve the portfolio’s quality. The following table illustrates just how outstanding these companies are.

Neither Home Depot nor Medtronic is a part of the other public, real-money portfolio I manage, my Grand-Twins College Fund, but both are on the watch list and could be added any time.

As always, investors are strongly urged to conduct their own thorough due diligence before buying any stocks.

— Mike Nadel

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.

Source: Dividends and Income