This article first appeared on Dividends and Income.

Since we launched DTA’s Income Builder Portfolio back in January 2018, I have talked often about the concept of “diversification.”

A stock portfolio should include enough names, in a variety of sectors, to limit the risk of owning too much within any one industry while still providing competitive overall performance.

So far, the IBP has a nice mix, with investments in 9 of the 11 sectors.

My next selection should help diversify the portfolio even a little more because it’s in one of the two sectors not yet represented in the IBP: Real Estate.

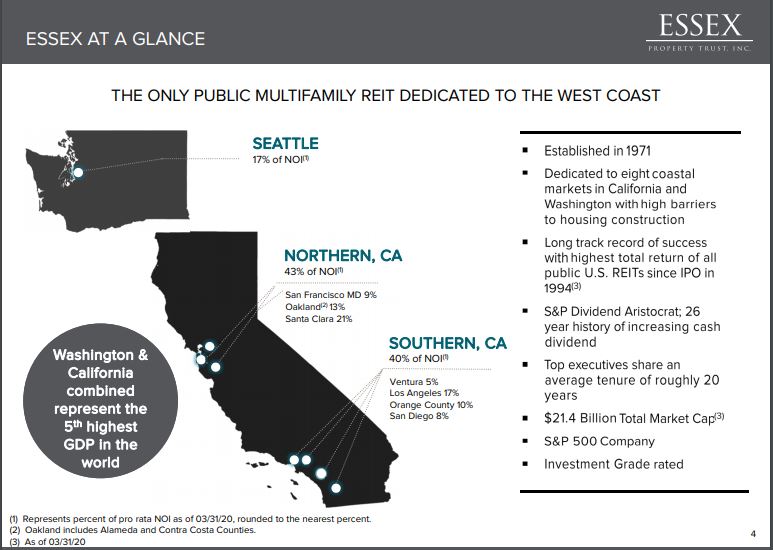

Notably, this real estate investment trust (or REIT) is, itself, uniquely concentrated – in other words, the opposite of diversified.

Not only does Essex specialize in multi-family units, it focuses on high-end facilities within only a handful of West Coast markets.

Essex Property Trust — Investor Presentation, June 2020

I actually considered two far more diversified apartment REITS — AvalonBay Communities (AVB) and Mid-America Apartment Communities (MAA).

Ultimately, however, I opted for Essex in part because I happen to believe these large West Coast cities will continue to attract residents who can pay top dollar for lodging.

Essex Property Trust — Investor Presentation, June 2020

Not For Everybody

We do not expect those who follow the IBP to re-create the portfolio for themselves. Rather, we try to offer interesting candidates for further research.

I certainly believe Essex Property Trust is interesting, but I acknowledge that it might not have as broad appeal as the more “traditional” Dividend Growth Investing names held in the IBP.

Those seriously considering ESS will tend to believe:

- That high-end West Coast apartment properties will recover well from the effects of the global coronavirus pandemic.

- That Essex-run facilities will continue to attract well-paid employees of high-tech companies.

- That if the work-from-home environment necessitated by the COVID-19 crisis becomes more permanent, it will not lead to a migration away from the expensive metropolitan areas in which Essex operates.

- That real estate in general, and a REIT in particular, is a welcome addition to one’s portfolio despite some of their quirks, such as somewhat different tax rules.

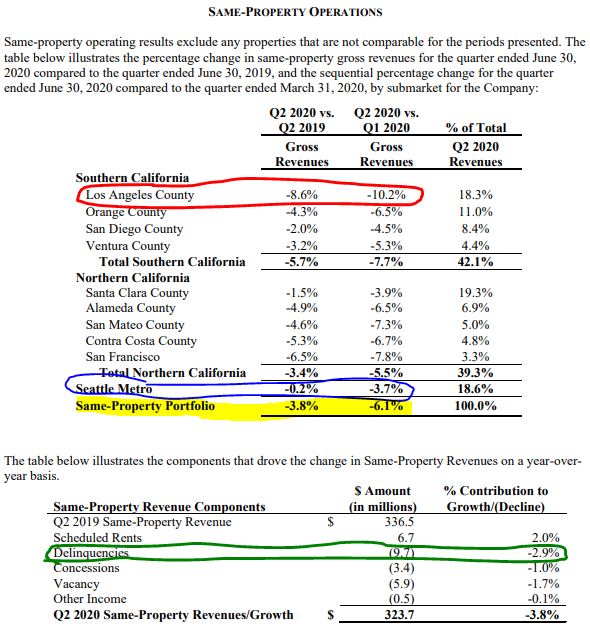

At the ESS second-quarter earnings call on Aug. 3, there was some sobering financial data, including: a steep decline in revenue for its Los Angeles County properties (red-circled area in graphic below); and a nearly 4% year-over-year decline in overall revenue and 6% revenue decline compared to Q1 (yellow highlight).

Essex Property Trust — Q2 2020 Results

The green-circled area shows that delinquencies — uncollected rents — made up most of the decline.

A relative bright spot was that Seattle-area properties held their own year-over-year (blue circle), although revenue was down nearly 4% from the previous quarter.

Essex CEO Michael Schall fully acknowledged that COVID-19 probably will continue to be a drag on his company’s performance in the near term.

Nevertheless, he cited several areas for optimism: fundamental improvement in numerous metrics at the end of Q2 and into Q3; a continuing “growth mode” for leading tech companies; some 17,000 job openings at the 10 largest public technology corporations; continued flow of venture capital; and gradual restarting of television production in the L.A. area.

At the end of the day, we believe that, the transaction markets will like to recover because lower interest rates will provide sufficient incentive to offset greater perceived risk. Historically, we found opportunities to add value as markets transition and in periods of disruption. I’m confident that we have the team, resources and strategy to thoughtfully act on these opportunities, consistent with our long-term track record of our performance.

The long-term track record that Schall referenced makes me confident in my ESS investment thesis.

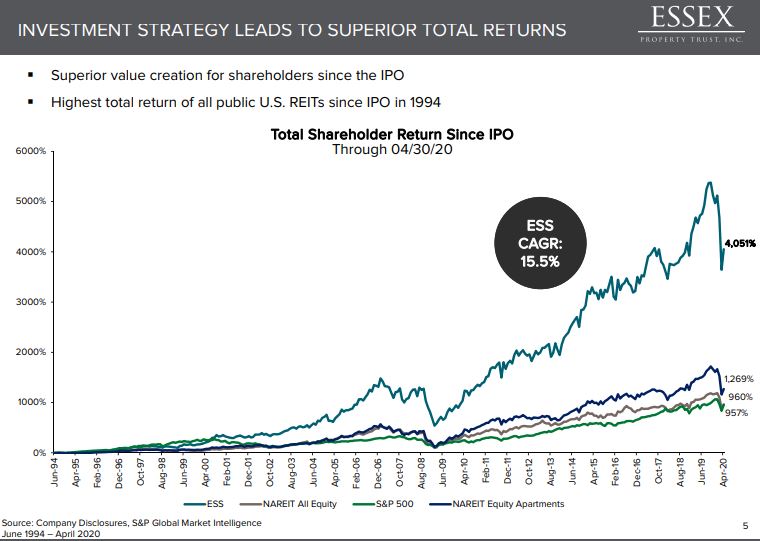

Since going public in 1994, Essex has blown away its peers, as well as the overall market.

Essex Property Trust — Investor Presentation, June 2020

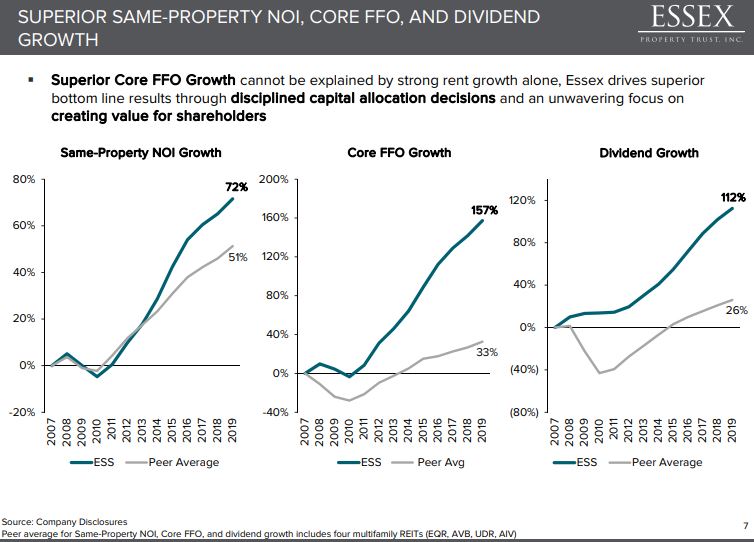

In more recent years, Essex Property’s fundamentals have continued to excel in categories important to REITs, such as net operating income (NOI), funds from operation (FFO) and dividend growth.

Essex Property Trust — Investor Presentation, June 2020

Dividend Royalty

To avoid onerous corporate taxes, REITs are required by law to pay out 90% of their income to shareholders.

So many of them tend to be higher yielders than regular corporations, which makes them popular with some DGI proponents.

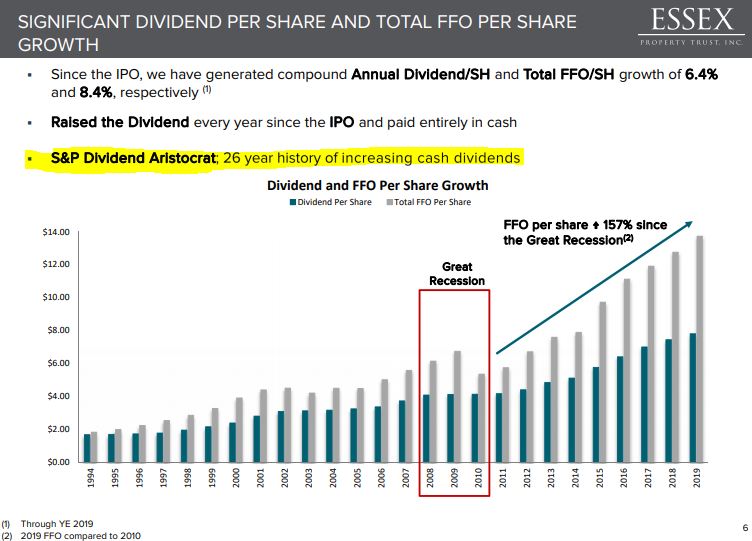

Still, only a few REITs have achieved Dividend Aristocrat status by growing their payouts annually for a quarter century or more.

Essex Property Trust is now at 26 years and counting.

Essex Property Trust — Investor Presentation, June 2020

The most recent dividend raise, 6.5%, took effect in April. Combined with the pandemic-related drop in the ESS stock price, that lifted the yield to 3.8% — near its all-time high.

Wrapping Things Up

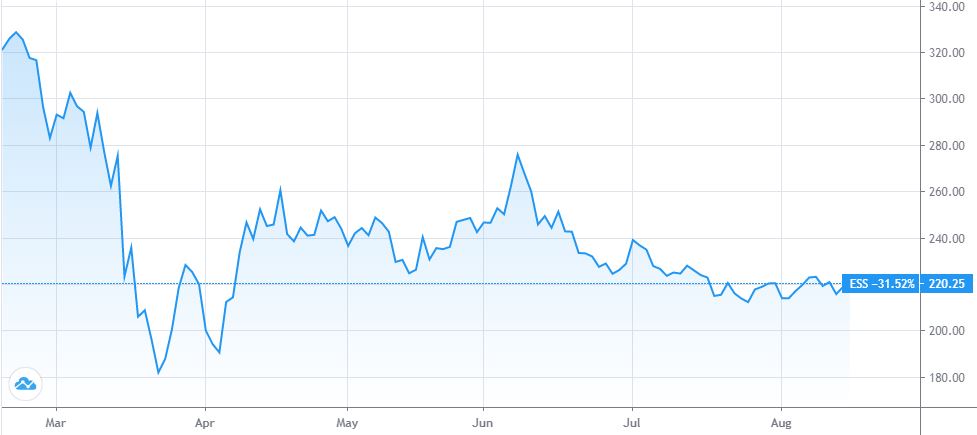

Back before February’s coronavirus-induced market crash, Essex Property Trust was riding high, its share price nearing $330.

ESS fell hard, and like many companies in industries that depend on a robust economy, recovery has been elusive. Its price at Monday’s close was $220.25.

Although folks who bought ESS last year or in early 2020 might not be happy campers, those considering it now have an opportunity to get a well-run company at a much more attractive price.

I will explore Essex Property’s valuation in my post-buy article, which will be published on Wednesday, Aug. 19.

Meanwhile, investors should conduct their own due diligence to determine if they are comfortable diversifying into REITs, especially one with such concentrated holdings.

— Mike Nadel

Marc Chaikin built the system that isolated NVDA before it became the best-performing stock of 2023. Click here to get his latest buy. More here.

Source: Dividends and Income