Right now, millions of people are plowing cash into this market, gambling that the worst of the dividend cuts is behind us.

I hope you’re not one of them, because this “dividend trap” is likely to spring—and steal away the income (and value) these folks have spent years building!

Just look at the numbers: unemployment is likely over 20%. Consumer spending cratered 7.5% in March, before this mess even really got started.

Meantime, even cash-rich companies are pulling in their horns, like the Walt Disney Co. (DIS), which suspended its dividend for the first half of the year—saving $1.6 billion, a fraction of the $14 billion of cash it has in the bank.

This is all why, as I wrote [last week], we need to comb through our portfolios to weed out any dividend payers that:

- Are in disastrous industries like travel.

- Have histories of cutting their payouts at the first sign of trouble.

- Have rickety balance sheets, with high debt and little cash, and …

- Unsustainable payout ratios, or annual dividends as a percentage of free cash flow (FCF). If any of your stocks pay more than 50% of FCF as dividends, you need to watch them carefully.

Monthly Payers Give You Extra Safety

We’ve got plenty of time to get back into stocks, so don’t feel any urgency to jump in now, despite the sugar high the market’s been on.

But if you do have cash you want to deploy, I’d suggest one thing: demand a monthly dividend, like the one you’ll get from the two funds I’ll reveal at the end of this article.

Sure, a monthly dividend tops a quarterly one—or, heaven forbid, one that dribbles out every six months like Disney’s—for managing your cash flow. But there’s more to it than that, because a dividend is a promise, and a monthly payout is a statement that management feels it can keep the cash coming through thick and thin.

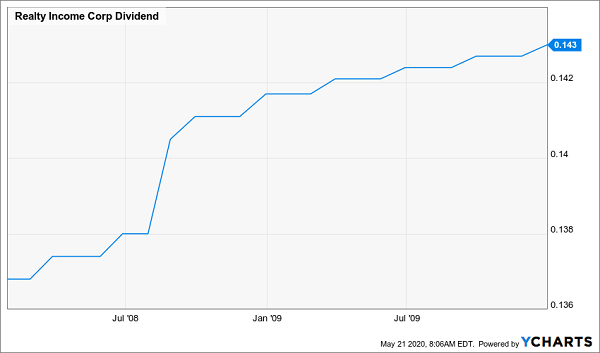

Even mall landlord Realty Income (O), the poster child for monthly payouts, has kept its dividend growing through previous crises, including 2008/09:

“Monthly Dividend Company” Keeps Payouts High in One Crisis …

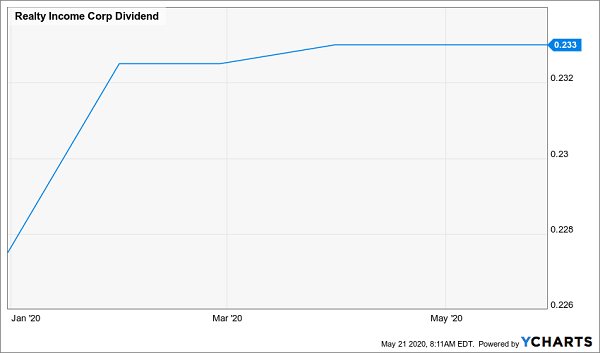

Even through the current crisis, Realty Income has kept its payout steady, despite missed rent from many of its restaurant, gym and child-care tenants.

… And Another

Amazon.com (AMZN) was already clobbering malls before this crisis, and with most people still stuck at home and shopping online, that trend will only accelerate.

So even though Realty Income’s payout still looks safe, at just 55% of funds from operations (which is low for a real estate investment trust), there’s little opportunity for payout growth here. That means the most we can expect is the stock’s current yield of 5.3% on an investment made today.

We can do better.

CEFs Deliver Big Returns—in Cash

Truth is, we won’t find the 7%+ monthly payers we need for a happy retirement among the cheapskates of the S&P 500. We need to go off the beaten path, to one of my favorite hunting grounds: closed-end funds (CEFs).

The PIMCO Dynamic Credit and Mortgage Income Fund (PCI) is a great example: it has a broad mandate to invest across the fixed-income universe and is led by superstar manager Daniel Ivascyn.

PCI yields an outsized 11.6% today and has handed members of my Contrarian Income Report service a gaudy 51% total return since I recommended it in May 2016. That’s more than double the 21% return on the high-yield benchmark SPDR Bloomberg Barclays High-Yield Bond ETF (JNK).

PCI has done what we wanted since we bought it, giving us a huge income stream (it yielded 10.8% when I recommended it) while its share price held relatively steady, meaning its entire gain was in safe dividend cash, rather than paper gains.

Big Discount, Safe Dividend

There’s another CEF measure that helps keep your income safe: the discount to net asset value (NAV). Due to a quirk in the CEF structure, these funds can (and often do) trade for less than the per-share value, or NAV, of their portfolios.

It’s an easy-to-spot measure that instantly tells you if a CEF is cheap. But what few people realize is the discount to NAV also amps up our yield, because to management, the only yield that really matters is the yield on NAV. However, as we’re buying at the discounted market price, we’re actually getting a higher yield.

PCI is a good example of this “yield magnifier” in action: as I said, it yielded 10.8%, based on its market price, when we bought. But because it traded at a 10% discount to NAV, its yield on NAV was a lower (and easier to cover for management) 9.7%.

Fast-forward to today, and PCI trades at a premium to NAV, so I don’t recommend putting any money into this fund now.

There are, however, plenty of CEFs still boasting discounts. Here are two that are worth your attention. As you can see, their “true” yields are much lower (and easier to cover for management) than their market-price yields. They pay monthly, too:

2 Cheap CEFs With Safe, High Dividends

This duo also makes a nice standalone monthly dividend portfolio on its own: GDV holds some of the top S&P 500 stocks for both the current period of social distancing and the recovery, such as Verizon Communications (VZ), MasterCard (MA), Microsoft (MSFT) and food maker Mondelez International (MDLZ).

ISD diversifies us beyond stocks, with high-yield bonds mostly issued by US companies. Managed by Prudential (PRU), a cornerstone of the financial world, this fund pays us a massive 10.1% yield on price—and its payout has been growing.

ISD’s Massive—and Growing—Monthly Payout

Source: CEFConnect.com

So don’t let anyone tell you that a safe, high, monthly dividend is a pipe dream. These “unicorns” are out there—and CEFs are your best shot at pocketing them.

— Brett Owens

Don’t Miss My “Crisis-Ready” 10% Monthly Payer Portfolio [sponsor]

You’ll find an entire collection of these dividend stars—CEFs and other investments included—in my “10% Monthly Payer Portfolio.”

I’ve personally hand-picked and safety checked this unique portfolio—from every angle—for maximum safety. The bottom line is that these stocks and funds are so cheap that I expect them to easily hold their own in the next pullback—and soar faster than the market if the rally picks up steam!

And we’ll soak up their huge payouts the whole time!

The dividends you’ll find here are truly life-changing: drop $500K into this powerful portfolio now and you’ll kick-start a $50,000 income stream—$4,167 a month!

Now is the time to get in, while you can still do so at a bargain. Click here to get everything you need—names, tickers, complete dividend histories and more—instantly.

Source: Contrarian Outlook