Beware of Wall Street “wisdom” now more than ever. Especially when it comes to the most commonly quoted maxim for retirement: it’s based on a rule that was never designed for times like these!

Enter the “Dividend Death Spiral”

I’m talking about the so-called “4% rule,” which says you should sell 4% of your nest egg every year in retirement.

Trouble is, it slashes your income stream and caps your upside in one go!

It’s especially dangerous advice to follow in a downturn like the one we’re experiencing.

Let’s say, for example, you owned $200,000 worth of Johnson & Johnson (JNJ) shares, which pay $3.80 in dividends on an annualized basis, for a 2.9% yield.

Let’s also say you were slated to sell 4% of your holding—or $8,000 worth—on February 5, when the stock hit an all-time high of $154. To get your $8K back then, you’d have had to sell 52 shares.

With 52 shares gone from your account, your dividend income drops by $198. Plus, you’ve got 52 fewer shares to appreciate in the future. It’s the worst of both worlds!

Now imagine what would happen if you had to sell last Thursday morning, only a bit more than a month later:

The Worst Kind of Market Timing

JNJ’s dividend is still fine, but the stock cratered 19% from its February 5 high to last Thursday morning. So now you’d now have to unload far more shares (64, to be exact) to get your $8K.

That puts an even harder cap on your future gains and slices your yearly income even more: by $243. Get hit by a few pullbacks like that and you’re well on your way to running out of money in retirement!

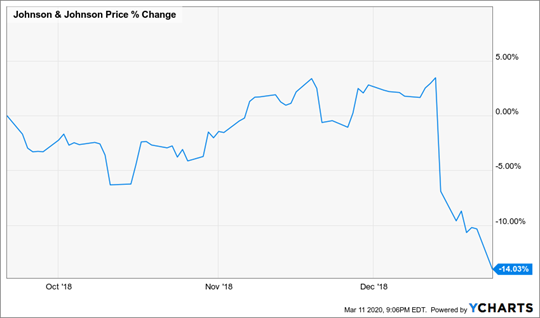

And you and I both know that these crashes are far from uncommon. In fact, if the chart above looks familiar, that’s because it is: JNJ last followed the S&P 500 down the drain a year and a half ago, in late 2018:

JNJ’s Last “Dividend Death Spiral” Wasn’t Long Ago

Your Return: From Sketchy to Serene

Luckily, there’s a better way than Wall Street’s flawed 4% approach. It involves moving more of our return away from wild stock charts like JNJ’s and toward a huge monthly cash stream that grows over time:

Swap This Wild Ride …

… For a Smooth Cash Stream Like This

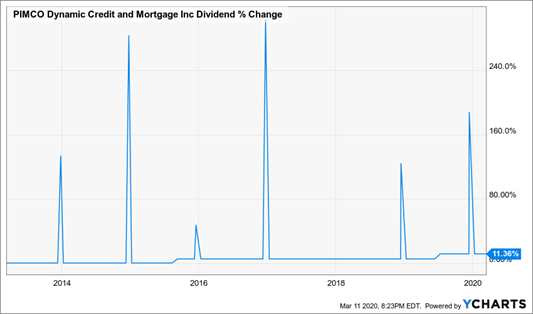

That second chart belongs to a closed-end fund (CEF) called the PIMCO Dynamic Credit and Mortgage Income Fund (PCI). As I write, this bond fund, run by one of the biggest, and savviest, CEF shops out there, yields an eye-popping 10.8%. That’s 3.5 times the payout on JNJ and 4.5 times the 2.1% the typical S&P 500 stock pays.

It gets better: as the chart above shows, that huge payout has grown 11.4% in the last decade—and you’d have gotten way more than that, thanks to the huge special dividends (represented by the big blue spikes) PCI sends out yearly.

The capper? PCI’s dividend comes your way monthly, not quarterly.

High monthly payouts give you something our beleaguered JNJ investor can only dream about: flexibility. If you’re relying on your portfolio to pay your bills, PCI’s monthly payouts line up nicely. And if you’re diverting some, or all, of your dividend cash back into your nest egg, monthly payouts let you do that faster.

Think about that for a moment: it’s the opposite of the 4% rule. Your reinvestments grow your upside potential and, with more shares in your account, your dividend stream grows, too. And thanks to PCI’s huge 10.8% payout, each additional share boosts your overall income a lot more than buying JNJ, with its ho-hum 2.9% payout.

Putting It All Together

Here’s the power of reinvesting PCI’s monthly payout: on a total-return basis (including dividends), the fund has nearly doubled the market’s gain since I recommended it to my Contrarian Income Report members in May 2016, returning 62% to the market’s 32%.

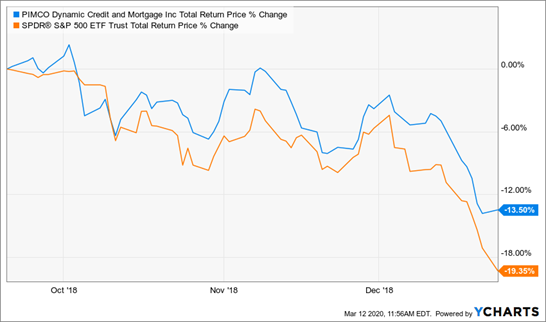

PCI’s cash stream helps steady the fund, too: back in 2018, it didn’t fall nearly as far as the market, thanks in large part to its continuing dividend payouts:

PCI’s Dividend Makes the Difference

— Brett Owens

Sponsored Link: PCI is just one of the picks in my Contrarian Income Report portfolio, which is throwing off an outsized 9.9% average dividend yield as I write this. And many of the stocks and funds inside yield much more, like one real estate investment trust (REIT) paying an incredible 12.4% now.

And get this: this smartly run company’s dividend has doubled in the last five years alone.

A 12.4% dividend that doubles? It’s one example of the kind of picks you’ll find in Contrarian Income Report’s portfolio, stocked with 17 funds and stocks. And today, with everyone losing their heads, is the perfect time to buy.

5 “Pullback-Proof” Dividends (up to 9.8%) You NEED to Buy Now

I’ll start by handing you my very best portfolio buys for these panicked times: 5 stout stocks and funds I refer to as “pullback-proof.”

These 5 buys trade at attractive discounts now, and they yield an incredible 8.5%, on average. The highest payer of the bunch throws off a massive 9.8% payout!

Here’s how a payout like that gives you an extra level of safety: nearly 10% of your initial buy boomerangs back to you every year in dividends, so if you simply let that cash accumulate, it will slowly offset your portfolio’s stock-market risk, adding a growing amount of ballast every year.

After 10 years, you’ll have recouped all of your investment in dividend income alone. Everything else is gravy!

That’s the definition of safety, and I can’t wait to share these 5 cash-rich dividend-payers with you now. I’ll also give you full access to my complete 17-stock Contrarian Income Report portfolio (average dividend yield: 9.9%!) with no risk and no obligation whatsoever.

Don’t deny yourself the peace of mind (and high income) you need in these worrying times. Go right here and I’ll give you my full safe-investing plan, complete access to my 17-stock Contrarian Income Report portfolio and the names of my 5 “pullback-proof” dividends.

Source: Contrarian Outlook