We named our income investing website Contrarian Outlook for times like these. When the rest of the world is selling everything, we are sorting through their hastily discarded dividend bargains.

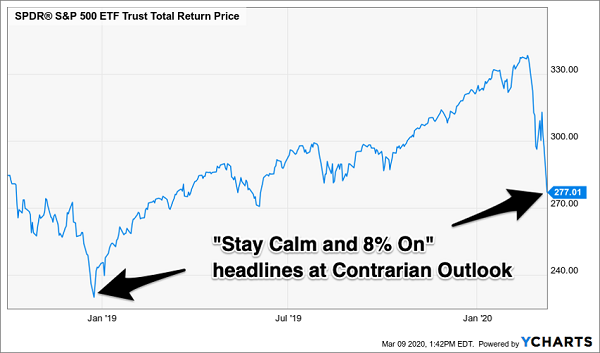

It was December 26, 2018, and the stock market had just plunged nearly 20%.Fear was rampant, which meant it was time for us contrarians to be greedy. Or, at minimum, not panic.

I don’t take the responsibility of being your Chief Investment Strategist lightly. Nor do I poke bear markets for the sake of contrarianism.

But we must keep level heads when the rest of the world is losing theirs. And while I didn’t know that the stock market was going to take off the moment I last issued a missive like this, I was pretty confident that we were (as we are right now) at least overdue for a big bounce:

Will Contrarian Outlook History Rhyme?

Panic is a wealth-slayer. Most investors employ a “gut feel” which basically means they take stomach punches from the market until they can no longer take it. They sell after most of the decline is through (as this is when it feels the most nauseating). Then they sit on cash and miss the inevitable follow-through rebound.

Studies show it’s very difficult (and really, impossible) to know when it’s time to “get back into stocks.” Hulbert Financial recently ran the numbers for Barron’s on the advisors it monitors. It focused on the best “peak market timers”—the gurus who correctly forecast the bursting of the Internet bubble in March 2000 and the Great Recession in October 2007.

These were the clairvoyant advisors who had their clients out of stocks and mostly in cash as the S&P 500 was about to be chopped in half. Surely their clients did great over the long haul, given their capital was largely intact at the market bottoms, right?

Wrong. None of these advisors turned in top performances. The reason? While they were good at timing tops, they were terrible at timing bottoms! The bearish advisors didn’t get their clients back into stocks anywhere near the bottom. They had their capital intact, but they didn’t deploy it—and they largely missed out on the epic bull markets that ensued after these crashes.

Let’s consider the CBOE’s S&P 500 Volatility Index (VIX). I know “the VIX” is now calculated differently, and that it is technically a trailing indicator (which means it’s looking in the rearview mirror). Whatever. If we had used this rearview mirror to buy stocks at the VIX’s peak, we’d be thrilled with our market timing:

Peak Fear Means Buy Here

Let me admit a couple of drawbacks to my back-of-the-napkin VIX analysis. First, VIX peaks are indeed only obvious in hindsight. However, when you see oil crash 30%+ overnight and US exchanges halt trading, we can reasonably assume that anything to follow would actually be an improvement.

Second, a “VIX spike” can precede the bottom in stock prices by a few days. This can be a tipoff that the plunge is ending. Lower prices but a calmer VIX is what traders call a “divergence.” In this case, it is one that would foreshadow higher prices.

Also, the magnitude of the current correction is worth noting. According to information from Nasdaq Dorsey Wright this is the 52nd correction of 10% or more since 1950. The average pullback was -17.9%.

Of the 51 previous 10% corrections, only 12 of those resulted in a peak-to-trough drawdown of 20% or more.

(As rough as the past few weeks have felt, we are roughly in line with the average, around 18.8% as I write.)

The near-term is always murky in these situations. Markets that are “oversold” can go even lower in the days ahead. But, eventually, the rubber band must “snap back” in the form of some rally.

And that, I think, is the point that we must keep in mind, especially this week. There are one of two market scenarios playing out:

- A scary but typical (every-other-year or so) pullback, or

- The beginning of a recession and broader bear market.

Number one remains the most likely, but let’s discuss them both. If this is indeed a pullback, then we’ll see a bottom put in soon (perhaps it was Monday). From there, we’ll see a sharp bounce higher. In late 2018, that was “it.” The market took off and never looked back (even now!). In other historical examples, the bounces have been interrupted by scary bouts to retest the previous lows (and shake shares from the final “weak hands.”)

Scenario two, a recession and bigger bear market, is of course the scary one. However, even if stocks are indeed destined to head lower, they are unlikely to continue heading lower in a straight line. We haven’t been this overdue for a bounce since December 26, 2018.

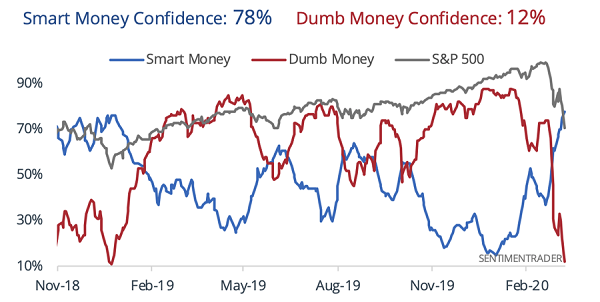

From a pure sentiment perspective, it’s the safest time to buy stocks since late 2018. Courtesy of data from our friends at SentimenTrader, here is our favorite “Smart versus Dumb Money” Confidence Chart:

Typically, we see peaks in the red line (the “Dumb Money”) as markets top. This reflects the greediness of individual investors, who typically jump into rallies late in the game.

Likewise, the blue line (the “Smart Money”) reflects the confidence that professionals have in the short-term future. These are the investors who don’t (dumbly, may I say) project recent market action out into the future. They prefer to buy low.

Let’s make sure we are running with the Smart Money and buying at current prices.

“Perfect” Late Cycle Dividend Plays That Pay 10% Today [sponsor]

To paraphrase the legendary rock band Chicago, does anybody really know what time it is in the rally right now? “Late cycle” is a popular guess. But how late?

Did the streetlights just pop on, or is it 2am with money managers stumbling into their taxis and Ubers outside?

Most rallies don’t make it to eleven, but then again, most don’t follow financial crises either. As Carmen Reinhart and Kenneth Rogoff outlined in their unique read This Time Is Different: Eight Centuries of Financial Folly, the big meltdowns eventually give way to economic expansions that:

- Have less “pop” than standard-fare recoveries. The previous financial wounds take longer to heal, so the ensuing good times take a (long) while to get rolling. And,

- They last longer, too. Participants pace themselves and everyone worries about the next hangover. The calmer party has more longevity!

Yet I often hear from readers who are concerned that our decade-plus market rally is ending right in front of our eyes. I can appreciate the concern. After all, stock prices usually precede economic news—drops precede recessions, bumps precede expansions—and ten-plus years is a long time to go between recessions (regardless of their severity).

Our newest “perfect” late cycle income play pays a safe 10%. That’s right. A secure 10%!

Put $50K into this stock and you’ll see $5,000 per year in dividends. Or $50K in annual dividends on a relatively modest $500,000! You get the idea.

What’s the ticker? Well, that’s what I’m here to show you today.

After years of keeping it my personal secret, I’m finally revealing my “Perfect” Late Cycle Income Portfolio. A simple, proven, and time-tested strategy you can use to double, triple, even quadruple your income–almost immediately!

Plus, I’m also going to give you THREE specific investments you can buy right now for MAXIMUM income combined with MAXIMUM stability!

This is a strategy I could easily charge thousands of dollars for.

But today, I’m handing you the keys to the kingdom right here on this page.

All you’ve got to do is take action and implement what you’ve discovered. If you want to take charge of your retirement income, you can easily build a portfolio which returns 10%+ per year—without EVER having to withdraw from your savings.

Now, compare this to the S&P 500’s 1.9% dividend and we’re talking about a $40,500 difference on a $500,000 portfolio—every single year! That’s the sort of life-changing money that can provide true security and freedom.

Best of all, as you’ll see today, it only takes a few minutes to set up this vastly more profitable portfolio.

When I talk about the Perfect “Late Cycle” Income Portfolio, I’m speaking about a collection of safe dividend stocks and funds that:

- Pay you 7%, 8% or more consistently and predictably—even if there’s a crisis, crash, or pullback.

- Give you a safe, secure, and steady income of $10s of thousands per year in cash—not just ‘paper gains.’

- Pay out exclusively from your investment income and NOT require you to withdraw cash from your savings or assets.

- Avoid overly complex, high-risk investments that can wipe out decades of hard-earned money in a matter of weeks or months!

- Are simple to set up and simple to manage—so you’re not glued to your screen all day and you can actually enjoy life.

- Are backed up by a proven track-record of 10% total returns per year since inception.

As I mentioned, this was built from years of painstaking research, trial and error, and financial modelling. I designed it for my own personal portfolio and my desire to enjoy a large income…without exposing myself to too much risk or withdrawing from my savings.

And, in the obsessive pursuit of this goal, I quickly realized traditional income strategies just weren’t going to cut it.

So, instead of listening to the mainstream advice like:

- “Invest in the Dividend Aristocrats” …

- “Withdraw 4% per year”…

- “lower your expenses”…

- “cut back on luxuries”…

I decided to carve my own path instead.

This journey led me to uncover three little-known investment “vehicles” that can safely and securely double, triple or even quadruple your income—almost immediately.

So, right now, I’m pulling back the curtain and showing you how you can build the Perfect “Late Cycle” Income Portfolio today. Click here and I’ll show you how to get access to my full research, recommendations and stocks to buy today (including their tickers and buy prices).

Source: Contrarian Outlook