Common stocks are what make up the vast majority of the stock market and the model portfolios of my Profitable Investing. They represent equity in the underlying companies that issue them, and they rise and fall in price with the valuations of those underlying companies.

Preferred shares are a different kind of stock. Companies typically issue them with a fixed dividend, paid quarterly.

And while they do represent an interest in the companies’ assets and businesses, their price will tend to be more stable. Like bonds, preferred shares represent more of a company’s debt.

They got their start back in the 19th century in the U.S. market as railroads were seeking to expand their networks westward and needed capital.

But since many of the railroads had already borrowed heavily in bank loans and bonds, investors were reluctant to lend more or buy more bonds. And the railroads had equally exhausted their ability to just issue more common stock.

The solution was a hybrid of a security that would be sold as equity but with the certainty of higher dividend payments. And if the railroads failed, investors would be next in line — just behind bond holders and well ahead of common stock investors — in getting paid.

Preferreds became a success. And thanks to evolving credit, accounting and tax rules, preferreds became ideal for companies to issue as an attractive additional form of capital.

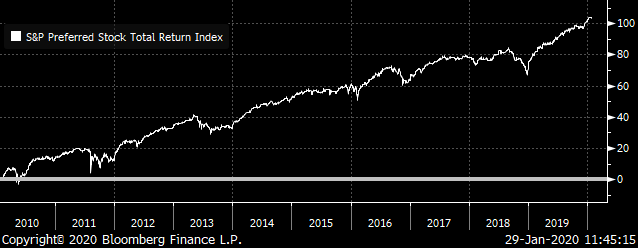

Preferreds Perform

Source: Chart by Bloomberg

Source: Chart by Bloomberg

These shares have continued in the market albeit at a lower number than common shares. And that’s one of the things that makes them attractive. Being less noticed than common stocks they tend to trade more under the radar of traders. That makes them more ideal for individual investors that seek less volatility with more certainty of higher dividend payments.

In addition, there are fewer indexes that track the market for preferreds and even those that do, don’t necessarily fully reflect the broad variety of the shares. Instead, most of the indexes focus on banks and financial firms’ preferreds which can distort the true attractiveness of many of the individual issues.

But they do continue to perform. For the past trailing ten years, the S&P Preferred Stock Index has shown a total return of 103.7% for an annual equivalent return yearly of 7.4%.

This means that the security of preferred shares along with declared dividends is no major sacrifice.

And it gets better when you look at how preferred stocks fare during major downdrafts in the general stock market. During the fourth quarter of 2018 when the S&P 500 dropped by almost 14% overall, the Preferred Index lost just a bit more that a third of that, proving that preferreds are preferred during times of common stock chaos.

Preferred Funds

To start investing in a preferred way, there are some funds that provide easy access to the best of the market.

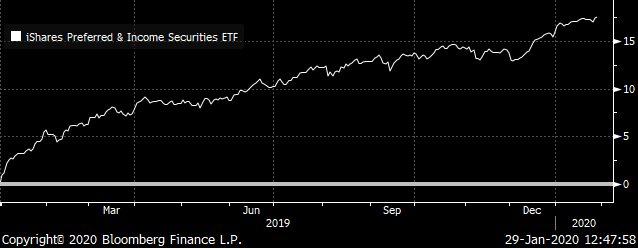

The iShares Preferred and Income Securities ETF (NASDAQ:PFF) pays a current yield of 4.9% which is multiples of that of the S&P 500, which runs at a mere 1.8%. And the exchange-traded fund has generated a return for all of 2019 to date of 17.5%.

Source: Chart by Bloomberg

Source: Chart by Bloomberg

Then beyond the ETFs there’s the favored closed-end Flaherty & Crumrine Preferred Income Opportunity Fund (NYSE:PFO). It generates and pays a 5.9% dividend yield and it has provided a total return of 29.7% for all of 2019 and the current year to date.

Source: Chart by Bloomberg

Source: Chart by Bloomberg

Individual Preferred Stocks

While the number of preferred stocks is dwarfed by common shares, there is still a wide collection of preferreds to choose from. Each of the following come from varied industries. The issuing companies are all well-supported to pay ample dividends. These shares will pay you well while taking more risk off of the table.

Now a word on buying these stocks. They do not trade with much volume. And the reason why is a good one. They are mostly bought by individual investors and funds that serve them, and they tend to be bought and owned, not traded. So, when placing orders, use a limit order near the current quote to buy.

In addition, I also recommend buying individual preferred in smaller sums and spreading your buys among a greater number for better acquisition prices and liquidity when selling. And note, that I provide the symbols for each of the preferreds along with the CUSIP or ISIN numbers which can be used to make certain that you buy the right issues for the following recommendations

So, let’s get on to my recommended bigger dividend preferred buys.

Preferred Stocks to Buy: Digital Realty Trust (DLR)

Digital Realty Trust (NYSE:DLR) is one of the leading real estate investment trusts (REITs) which owns and leases data center properties around the U.S. and in strategic markets beyond. Data centers are the crucial hubs for cloud computing and will also be integral for the evolution of the fifth generation (5G) wireless.

This REIT continues to perform well with its common shares. But it also has its Digital Realty Series J Preferred Shares (DLR Series L, CUSIP #253868822) to compliment the ordinary common REIT shares of Digital Realty. The shares are priced at $26.12 for a current yield just under 5%.

Seaspan Corporation (SSW)

Seaspan Corporation (NYSE:SSW) is sort of a REIT, but for container ships. It leases out its ships to various companies on longer-term contracts. As such, it focuses on making contracts with viable operating shipping companies to maximize revenues from its fleet while controlling the risk of default. And revenues are up over the past year by 31.9%

It has done a good job of this with ample operating margins sitting at 42.9% which results in a return on common stock equity of 14.9% It has ample cash on hand and its debts are low, resulting in an under-leveraged landlord of the shipping lanes.

It has a series of preferred shares as part of its capital. The preferred to buy is the 7.875% Series H Preferred Shares (SSW.H, CUSIP #81254U304) that are currently trading at $26.13 for a current yield of 7.5%. This preferred is perpetual, meaning that there is no maturity. However, there is a call that the company can make to buy it back at $25 starting on Aug. 11, 2021 which if occurred would reduce the yield to 4.8%.

Teekay LNG Partners (TGP)

Teekay LNG Partners (NYSE:TGP) is a pass-through company that is focused on shipping liquified natural gas (LNG) as well as other petroleum products. The LNG market is attractive, particularly thanks to the expanded production of natural gas in the U.S. What’s more, the industry is expanding pipelines and marine terminals for LNG. Those things combined should support LNG shipping, despite recent price action.

With global demand for LNG remaining strong as it replaces coal as the preferred form of energy, companies upstream to downstream continue to see further progress.

Teekay has rising revenues climbing by 18% over the trailing year. And operating margins are fat at 28.9%. And like for Seaspan, debt is reasonable with its debt-to-assets ratio running at a serviceable 60.7%, making for a reasonably leveraged company.

The company has two preferreds in the market. I’m recommending the 9% Series A Preferred (TGP.A, ISIN #MHY8564M1131). It is another perpetual maturity with a call on Oct. 5, 2021 at $25. It is trading at $26.50 for a current yield of 8.5%. If called, the yield would be reduced to 5.3%.

NuStar Energy (NS)

NuStar Energy (NYSE:NS) is another pass-through company with 8,700 miles of pipeline for refined petroleum products. It has additional pipelines for crude oil and other petroleum-related products. It also provides services for marketing companies in the Caribbean and South American markets

Revenues are positive with gains over the trailing year of 8.1% and operating margins are ample at 18.5%. Like the other companies with preferred recommendations, it has controlled debts at only 49.3% of its ample assets.

It has a series of preferreds as part of its petroleum logistics. I’m recommending the 8.5% Series A Preferred (NS.A CUSIP #67058H201) it has a fixed dividend of 8.5% until Dec. 15, 2021 at which it will shift to an adjustable dividend at the three-month U.S. Treasury yield plus 6.8% of the price at which the preferred is trading. It currently trades hands at $24.81 for a current yield of 8.6%. And if called the yield would rise to an effective 9.8%.

— Neil George

Silicon Valley venture capitalist Luke Lango says this little-known Apple project could be 10X bigger than the iPhone, MacBook, and iPad COMBINED! Investing in Apple today would be a smart move... but he’s discovered a bigger opportunity lying under Wall Street’s radar -one that could give early investors a shot at 40X gains! Click here for more details.

Source: Investor Place