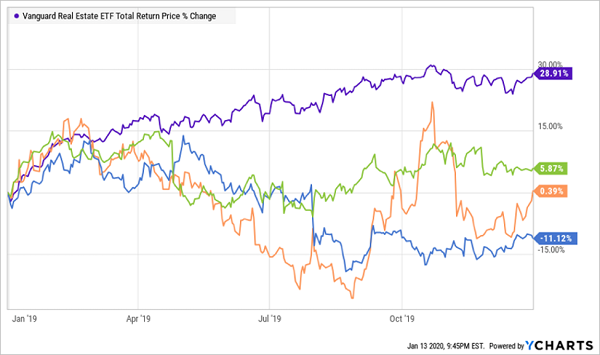

Income hunters that made their way into real estate investment trusts (REITs) at the start of 2019 are rolling in more than rent checks right now. Not only did they enjoy the sector’s generous dividends, they enjoyed big price gains to boot.

Even the “dumbly indexed” Vanguard Real Estate ETF (VNQ) peeled off a sweet 28.9% in total returns last year. That’s its best showing since 2014, and more than double its average annual return of 11%-plus over the past decade.

I’ve previously warned about the dangers of holding REITs whose fundamentals are out of whack with its valuation.

Not only are we limiting our upside with expensive shares, but overpriced property owners tend to yield less, too.

Unfortunately, today, the entire sector looks quite expensive!

REITs on average are trading for almost 19 times funds from operations (FFO, a quintessential profitability metric for real estate companies).

I typically want to buy into REITs when they’re cheaper from a P/FFO perspective. Our pickings are slim.

However, not every REIT followed the sector into the clouds in 2019. In fact, a few took it on the chin, and as a result trade far cheaper than their lofty peers—and sport screaming dividends to boot:

Could This Troubled Trio Turn It Around in 2020?

These three beaten down REITs are cheap in terms of their cash flows, and boast yields all the way up to 8.6%. But are they cheap for a reason?

These three beaten down REITs are cheap in terms of their cash flows, and boast yields all the way up to 8.6%. But are they cheap for a reason?

Taubman Centers (TCO)

Dividend Yield: 8.6%

Price/FFO: 6.2

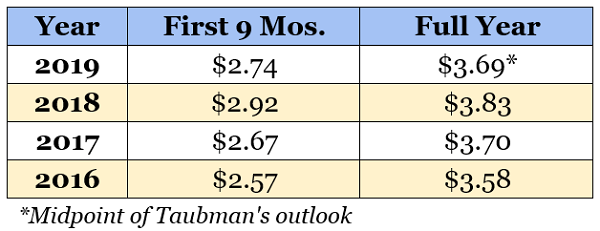

Let’s start out with Taubman Centers (TCO), which is quite cheap at a mere 6.2 times its trailing 12-month funds from operations.

Taubman is a retail REIT, which immediately answers the question “What happened?” once you discover that TCO’s stock plunged 32% in 2019.

Specifically, Taubman owns, manages and/or leases 26 regional, super-regional and outlet shopping centers in the U.S. (that’s a problem) and in Asia (more encouraging).

To the company’s credit, it has been working for years to improve various aspects of the business. Taubman’s tenant mix is much more diversified than it once was, which has driven more than three consecutive years’ worth of quarterly tenant per-square-foot sales growth. It’s also been dealing with its debt issues, extending its primary line of credit and selling 50% of its interest in Starfield Hanam, to real estate funds managed by Blackstone (BX), to raise $300 million in cash.

Indeed, if you look at the company’s operational performance since 2016, it would appear that 2019’s thud—which included a disappointing third-quarter report that investors met with ire—was merely an anomaly.

Indeed, if you look at the company’s operational performance since 2016, it would appear that 2019’s thud—which included a disappointing third-quarter report that investors met with ire—was merely an anomaly.

But one of the factors impacting that Q3 report is a reminder of the uphill climb Taubman and most traditional shopping-center REITs have to contend with: dying retailers. CEO Robert Taubman said in the most recent conference call that the bankruptcy of Forever 21 had a “significant impact.” That’s despite the loss of just two of Forever 21’s locations.

The dividend is at least for real. The payout has been growing steadily for years and represents only 73% of this year’s full-year FFO estimates. But an uncertain landscape for brick-and-mortar retail puts most retail REITs in question. Taubman might be set up for a dead-cat bounce simply because it’s so cheap. But a long-term retirement solution? Hardly.

Hersha Hospitality Trust (HT)

Dividend Yield: 8.3%

Price/FFO: 6.6

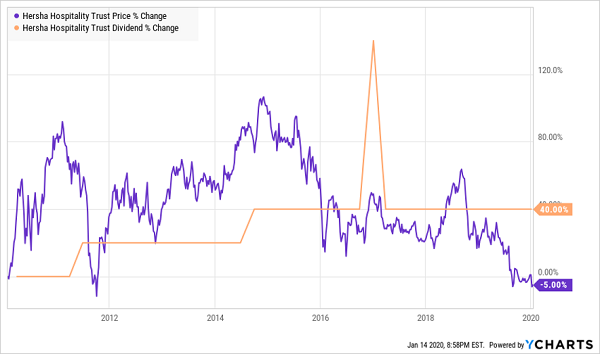

Hersha is a bi-coastal hotel REIT sporting a collection of 48 hotels, totaling more than 7,600 rooms, in cities such as New York, Boston, Los Angeles and Washington, D.C. Its properties house high-quality upscale, luxury and lifestyle transient hotels, spanning well-known brand names such as Hyatt (H) and Marriott (MAR), but also independent hotels such as Philadelphia’s five-diamond The Rittenhouse.

That didn’t matter in 2019. Almost everyone in the hospitality real estate industry struggled. Pebblebrook Hotel Trust (PEB) lost 5%. CorePoint Lodging (CPLG) fell by 13%. Hersha, though, was among the worst at a 17% loss.

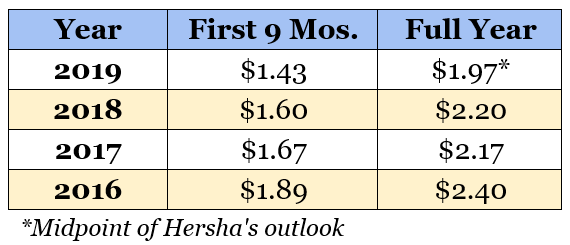

I believe in lodging’s potential long-term, and catering to upper-class customers is almost a winning formula more often than not. But Hersha’s 2019 isn’t an isolated incident. Just look at how funds from operations have been trending over the past few years:

While CEO Jay Shah expresses quite a bit of optimism in the company’s quarterly results, as well as some legitimately strong results in important hotel metrics such as RevPAR, the fact remains that it’s struggling in key markets, most notably New York City.

While CEO Jay Shah expresses quite a bit of optimism in the company’s quarterly results, as well as some legitimately strong results in important hotel metrics such as RevPAR, the fact remains that it’s struggling in key markets, most notably New York City.

HT’s payment has remained flat for almost five years now as a result of its weak results, and as I frequently preach: prices chase dividends, for better or worse:

Upscale Hotels, But Downmarket Price Action

Iron Mountain (IRM)

Iron Mountain (IRM)

Dividend Yield: 8.1%

Price/FFO: 10.8

Iron Mountain (IRM) is truly a rare breed of a REIT, providing something that many companies still need: shredding and document storage.

It provides a lot more than that, too, out of necessity. As companies go increasingly paperless, that’s less product for Iron Mountain to keep locked up or destroy. So it has branched out into data centers, document scanning, analytics and workflow automation.

But it’s not happening fast enough.

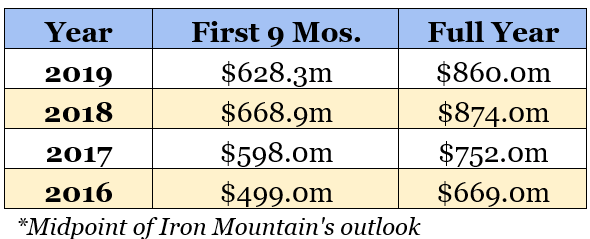

The “first-level” numbers don’t seem to indicate that. Growth has been pretty steady of late, albeit with a hiccup in 2019.

The problems lie underneath. For instance, consider that through nine months in 2019, data center operations accounted for just 6% of revenues. Data management accounted for 9%. Records and information management, which includes its shredding business, was half IRM’s year-to-date sales, and that part of the business continues to shrink.

The problems lie underneath. For instance, consider that through nine months in 2019, data center operations accounted for just 6% of revenues. Data management accounted for 9%. Records and information management, which includes its shredding business, was half IRM’s year-to-date sales, and that part of the business continues to shrink.

It’s clear management isn’t pleased with its progress on modernizing. The day of its earnings release, it also announced a “transformation program” called Project Summit that’s “designed to accelerate execution of Iron Mountain’s stated strategy. In a nutshell, it’s simplifying its org structure and streamlining management (cutting costs).

That’s not to say IRM can’t become a digital juggernaut somewhere much farther down the line, but for now, its legacy business is in decline while it struggles to make hay in where its future lies.

The final strike against Iron Mountain for now? Its pace of dividend growth over the past four years:

- 2016: +13%

- 2017: +6.8%

- 2018: +4%

- 2019: +1.2%

These 8%+ yields are far from perfect, which is why their stocks are trading a such steep discounts. But it is possible to find bargain yields that are a bit more ideal for your retirement portfolio. Dare I say, these stocks are near-perfect for any retiree hoping to live on dividends forever?

Brett Owens

“Perfect” Retirement Income”: Start 2020 By Quadrupling Your Yield [sponsor]

There’s nothing inherently “safe” about 7%-8% yields.

What makes a high level of income right for retirement is a company’s ability to sustain and grow that payout over time while still funneling money into growing the business.

That’s what allows you to afford your home, afford your utilities and afford a high quality of life, even if the broader stock market doesn’t cooperate.

You can lock up that level of safety from the dividend-rich stocks in my “Perfect Income Portfolio.”

Nest eggs are being stretched paper-thin because medical innovations are helping us live longer than ever before, meaning retirement accounts must last far longer than they were ever intended to. But this is 2020, not 2000. 10-year Treasuries don’t pay 6.6% anymore—they pay 1.8%. The 2%-3% yields on most Dow stocks just won’t cut it, either.

Instead, investors—especially those with more modest nest eggs—need roughly 3x to 4x the yield of the broader market. And those substantial income checks need to survive not just through 2021 or 2022, but literally decades down the road.

My Perfect Income Portfolio offers exactly that. In fact, several of my readers have emailed me to tell me this portfolio has literally doubled, tripled, or in a few cases actually quadrupled their annual income.

Also, this is a buy-and-hold portfolio. This isn’t a crazy options tactic or a set of short-term swing trades. It’s just a set of under-the-radar, contrarian income plays that can quickly build your wealth without piling on the extra risk of gambling on newspapers and dying retailers.

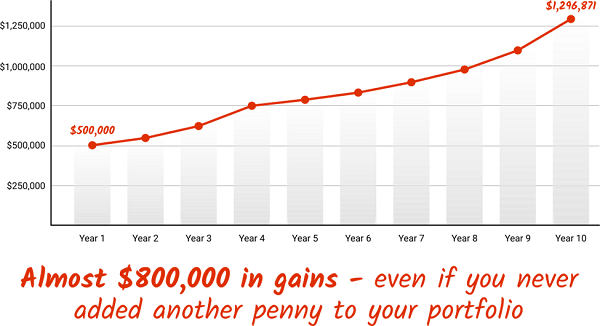

Too good to be true? Look at this strategy’s past 10 years of returns, and you’ll see why I call it the “Perfect Income Portfolio”:

These dividend dynamos offer so much more than high headline yield. This portfolio checks off a bundle of vital retirement boxes:

- It gives you a safe, secure, and steady income of tens of thousands per year in cash—not just “paper gains.”

- It pays out more than enough to live on from dividends without drawing down your savings or assets.

- You avoid overly complex, high-risk investments that can wipe out decades of hard-earned money in a matter of weeks or months!

- You’re not involved in any risky options, spread-bets, or day-trading.

- It’s simple to set up and simple to manage. That way you’re not glued to your screen all day. Go out. Enjoy life. Your check’ll be in the mail.

Don’t lie awake anymore worrying about your yo-yo-ing net worth. Instead, let me teach you more about this incredible strategy, including its dominant track record. In fact, I’ll even let you hear it from the mouths of other investors that have reaped market-smashing gains from my research service.

Don’t wait another minute. Learn how to get 2x-4x your current income with this simple, straightforward system. Click here to get a FREE copy of my Perfect Income Portfolio report, including tickers, buy-in prices, dividend yields, full analyses of each pick … and a few other bonuses!

Source: Contrarian Outlook