A big thank you to the 1,186 subscribers who attended our Contrarian Income Report webcast! As we discussed in the session, I did my best to address presubmitted questions during the session.

More questions came in during the live webcast. I love the enthusiasm. Let’s use our time together today to chat about your shared thoughts, curiosities and concerns.

Q: What do you think about trailing stops (with percentages)?

Q: Do you recommend trailing stops, or should we just wait for you to tell us when to sell?

Q: Would a 10% trailing stop work for your picks?

Q: How did these holdings perform during a bear market?

Trailing stops can be useful tools, especially if you are a trader. For example, let’s say we are greedy from hearing about all of the gold hype and we want to “get in” before gold goes to the levels that you see speculated on the commercials polluting our mind on financial TV.

But how do we know when the trend has switched from up to down?

We could use a trailing stop to do this.

For example, today we know that gold is heading up.

So we could buy the yellow metal today and sell when the relic drops by 10%.

(I’m not suggesting we actually do this!)

The problem with using a trailing stop strategy for our dividend portfolio is that it is not nearly as volatile as gold or even the stock market in general. Our big dividends (averaging 7.2% in the CIR portfolio as I write) serve as flotation devices during any downturn.

For example, check out the performance of this portfolio during the last bear market we’ve experienced. (It actually began just 12 months ago!) Anyone who dumped their life savings into the S&P 500 on October 1, 2018 was quickly cursing themselves for their bad luck, as the index proceeded to drop 20% over the next three months (the black line in the chart below).

Our CIR portfolio, however, treaded water through most of the downturn (the green line below). Some positions finally turned down in mid-December, when the selling was reaching its climax:

CIR Returns 15.7% Versus the S&P 500’s 5.5%

Source: Morningstar

Source: Morningstar

It was clear to me, your human portfolio operator, that stocks were ready to bounce. In fact, I touched base with you on December 26 (the day the bull market resumed) to reiterate that we were buyers and not sellers!

Depending on the percentage used for your stop-loss formula, the computer portfolio operators wouldn’t have been so smart. Tight stops in particular would have flipped you into cash at exactly the wrong moment. And then how would you know when to redeploy that cash?

There’s a time and a place for stops. I do use them from time to time, but only on a limited basis and after I’ve put my human eye to their exact placement.

You don’t need to worry about this. When it’s time to sell, I let you know in our monthly issues. And if it’s urgent (which, to be honest, it rarely is) I’ll send out a flash alert via email.

Q: What’s up with DSL?

Q: What is your current view of DSL?

Q: Any news on DSL?

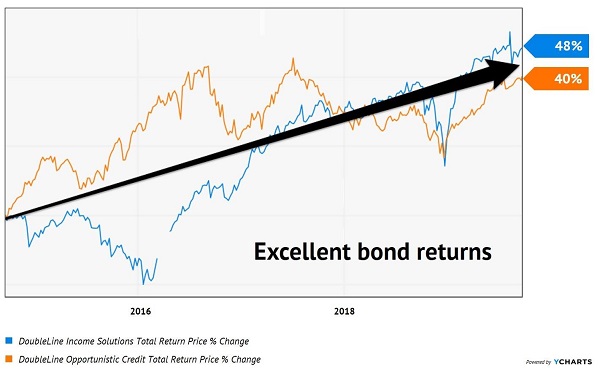

DoubleLine’s founder Jeffrey Gundlach (nicknamed the bond god for his fixed income brilliance) runs two very successful closed-end funds (CEFs). His team of 65 credit analysts cherry pick their favorite bonds in the US and around the globe. Over the past five years, the two funds have delivered total returns (including distributions) of 40% and 48%:

It’s Tough to Beat These Bond Funds

These are of course excellent results for bonds. Of the two vehicles, I prefer to drive the DoubleLine Income Solutions (DSL) fund because its team has a wider mandate to search the globe for high yield.

These are of course excellent results for bonds. Of the two vehicles, I prefer to drive the DoubleLine Income Solutions (DSL) fund because its team has a wider mandate to search the globe for high yield.

At the end of July, DSL’s top 25 holdings yielded an average 7.6%. How great is that in a world where Uncle Sam’s bonds pay just 1.5%?

Plus, Gundlach gets to borrow money for cheap (about 2%) to buy more high paying bonds. DSL levers its portfolio up an additional 30% or so to bring the net yield on its fund to 9.1%. And remember, that’s after Gundlach’s fees!

Since I formally recommended DSL to my Contrarian Income Report subscribers, it has delivered 60% total returns in less than three-and-a-half years. We beat the chart above because we “bought the dip” in early 2016. And we have another dip right now thanks to a good ol’ fashioned currency crisis in Argentina.

The DoubleLine team had doubled down too often on Argentina. A charming place to visit, but an economic basket case, it represented 10% of the fund. That’s not a position you want to have when the country’s peso crashes.

It was a rare miss for this talented team, but a miss nonetheless. It doesn’t make sense to buy more shares at a premium. So should we sell and cash our profits? No. I think Gundlach & Co. deserve the benefit of the doubt while they sort out this mini-mess.

Most of the short-term damage is done. Our long-term prospects remain very good and the fund still pays 9.1%. We’re going to keep holding this income machine.

Q: Do you recommend reinvesting dividends?

Q: Is it better to reinvest dividends or collect cash in the account?

The most important thing in income investing is to make sure your money is collecting additional cash flow for you at all times. This means being fully invested (and not paying attention to broke economists who are trying to get attention with their recession predictions!)

If reinvesting your dividends automatically does this, and it works for you, then go for it. Any current portfolio holding is a good candidate for dividend reinvestment (whether a buy or hold).

What’s the difference? “Holds” are stocks and funds that I project to return their yields. For example, if a fund is paying 7% and I have it ranked as a hold, then I believe its price will trend sideways while the fund pays its dividend.

If the same fund is ranked as a “Buy,” then I believe it has some price upside, too. Modest price gains can result in 10%+ total returns.

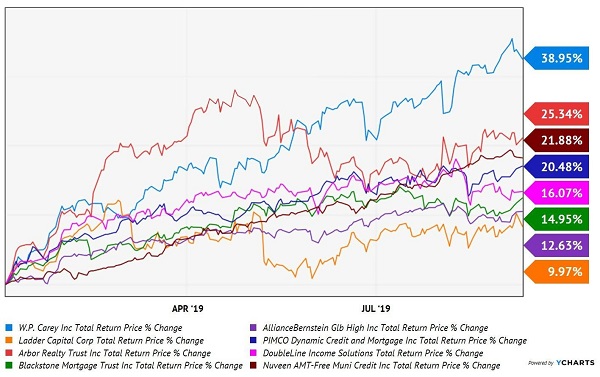

In a perfect world, you’d collect your cash and reinvest it in our monthly best buys. For example, the eight best buys we outlined in the January issue of CIR have gone bonkers year-to-date:

Returns Up to 39% Year-To-Date

Then again, our average portfolio holding is up an amazing 23.4% year-to-date, so you really couldn’t have gone wrong. The important thing was to stay invested, keep reinvesting and, most importantly, not “stop out” when the outlook was most bleak last December!

Then again, our average portfolio holding is up an amazing 23.4% year-to-date, so you really couldn’t have gone wrong. The important thing was to stay invested, keep reinvesting and, most importantly, not “stop out” when the outlook was most bleak last December!

Q: Are you concerned with expense ratios? Some funds have ratios over 2%. This would usually be a concern for me.

In a word, no. When investing in CEFs (closed-end funds) it is important to not be cheap about fees.

Most investors are conditioned by their experience with mutual funds and ETFs to search out the lowest fees, almost to a fault. This makes sense for investment vehicles that are roughly going to perform in-line with the broader market. Lowering your costs minimizes drag.

Closed-ends are a different investment animal, though. On the whole, there are many more dogs than gems. It’s an absolute necessity to find a great manager with a solid track record. Great managers tend to be expensive, of course – but they’re well worth it.

The stated yields you see quoted, by the way, are always net of fees. Your account will never be debited for the fees from any fund you own. They are simply paid by the fund itself from its NAV.

— Brett Owens

The Secret to Boosting Your Retirement Income 4X (2008 or No) [sponsor]

My “Perfect Income Portfolio” sets you free from ever having to worry about a recession. That’s because it returns 4X more income than regular investors make.

And you won’t ever have to withdraw a single cent from your portfolio!

So if you never have to sell, who cares when the next crash hits? You can simply live on dividends alone, come what may.

Here’s what else you get from this incredible collection of investments:

- Consistent, predictable payouts—even if there’s a crisis, crash or pullback.

- Safe, steady income of tens of thousands per year in CASH—not just “paper gains.” And you can do it on a reasonable nest egg, not the million bucks (and more) Wall Street says you need.

- Easy setup, minimum time commitment—so you’re not glued to your screen all day and can actually enjoy life.

I know—sounds like I’m promising a lot, right?

It does.

But my system, which I’ll share with you when you click right here—is proven to deliver all of the above and more.

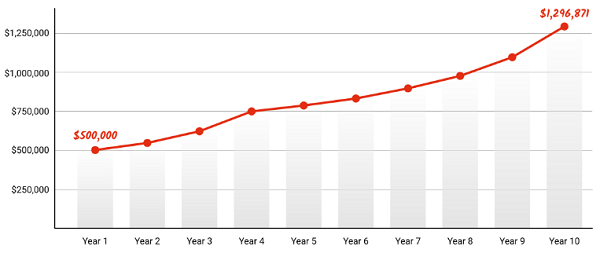

Look at what would have happened to, say, a $500K nest egg—half of what the so-called “experts” say you need to hang them up—if you’d invested it in my “Perfect Income Portfolio” 10 years ago:

That’s almost $800,000 in gains—even if you never added another penny to your portfolio!

I’m ready to show you everything you need to get started right now, including how to take the 2% dividends you’re likely earning and turning them into 6%, 8%, even 10% per year in cold, hard, spendable income.

I’ll also give you my favorite investments on which to build your “Perfect Income Portfolio”—names, tickers, buy-up-to prices and all of my research on each of these “steady Eddie” income generators.

All yours. Right now.

Don’t miss out: click right here to get full details on my brand new “Perfect Income Portfolio” and start building your own “correction-proof” future today.

Source: Contrarian Outlook