Until about a year ago, the most common question I got from readers was always something like: “How will rising interest rates affect my portfolio?”

The question looks simple, but the answer was not, and in 2015, when the Fed said it would start hiking rates (the first hike came in December of that year), plenty of panicked investors sold (despite my advice at the time):

Short-Term Rate Fears …

What this chart really meant is that these short-term panickers gave patient investors a great buying opportunity, as the next chart shows:

… Set Up Longer-Term Gains

But the folks who sold right around the time of the first rate cut missed out because they feared the Fed.

First, let’s back up and quickly talk about how floating-rate loans work.

If you’ve bought a house, chances are you had the choice between a fixed-rate mortgage (a loan with a set interest rate, based on interest-rate benchmarks) or a variable-rate mortgage (with a rate that changes in the future, based on movements in the interest-rate benchmark).

For the homebuyer, a fixed rate is good if rates go up, and a variable rate is good if rates go down. The bank takes the other side of the variable-rate bet: these loans are bad for banks if rates go down and good if they go up, because higher rates mean borrowers pay more interest.

Floating-rate loans are simply variable-rate loans given to companies, usually mid-sized and up. You can buy into floating-rate loans through one of 31 CEFs specializing in them.

So picking up some floating-rate-loan CEFs in a time of rising rates sounds like a great idea, right? In theory, sure. In practice, not so much.

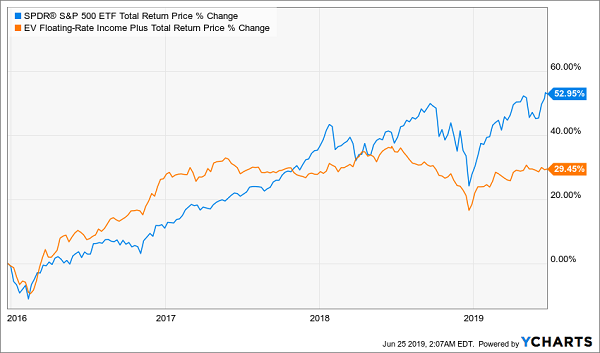

“Obvious” Rate-Hike Play Fizzles

From the time the Fed started hiking rates to now, the total return on the Eaton Vance Floating-Rate Income Plus Fund (EFF) was just over half that of the S&P 500. Clearly the winning move was to ignore the noise about the Fed (and the conventional “wisdom” that rising rates are bad for the stock market) and stick with stocks.

This wasn’t just true of EFF, by the way; only two floating-rate funds, the Nuveen Credit Strategies Income Fund (JQC) and the Aberdeen Credit Strategies Fund (ACP), outperformed the S&P 500 during this period, and that was only because of both have an international focus.

The reason why all US senior-loan funds underperformed is simple: the Federal Reserve isn’t the only thing that affects the value of a senior loan.

There are risks with the debt issuer, the underwriters, the larger economy, default rates and ratings that also impact the value of these assets, which makes them a very difficult investment to get right. It’s no wonder many of these funds did poorly during this period—even the biggest debt players in the world got it wrong, like the BlackRock Floating Rate Income Trust (BGT), which was crushed by the market:

Floating-Rate Giant Comes Up Short

The key takeaway: don’t let one factor dominate your investment decisions, even if it’s a big factor like the Fed. If you think the Fed’s interest-rate targets will affect markets, do incorporate that into your decision, but don’t let it be the only decider.

EFF: Is Now the Time to Buy?

EFF’s management has taken this advice to heart, which is why it’s made a change to its investment strategy that seems subtle but is actually a big deal for a fund with “floating rate” in its name: EFF is shying away from floating-rate loans.

While the fund will still focus on this market, it will now be able to invest up to 20% of its assets in collateralized loan obligations and collateralized debt obligations (CLOs and CDOs), both of which are types of derivatives based on corporate debts of many types, not just senior loans. As derivatives, they have much higher potential returns and much higher risks; as diversified derivatives, they also offer a hedge against senior loans.

EFF’s decision to increase its allocation to the opposite of its investment mandate makes sense: the Fed is looking to cut rates, which should make a lot of overbought senior loans fall in value, hurting EFF’s total returns. So the fund’s management is smart to get ahead of this trend.

The pivot to CLOs doesn’t make EFF an obvious buy, however. The massive risks and high costs involved in CLOs will make EFF much riskier than it currently is, especially if there’s a panic in corporate-debt markets. So let’s leave EFF and its 6.6% yield on the sidelines and put our cash into safer (and higher yielding) alternatives.

— Michael Foster

Forget EFF: This Growing 10.7% Dividend Is a Bargain (for now!) [sponsor]

You can start by giving yourself a dividend nearly twice as big (and much safer) than what EFF pays when you buy my No. 1 equity CEF pick now.

I’ve made this top-secret CEF my No. 1 pick in stock-focused funds for two reasons:

- It boasts an amazing 10.7% dividend yield, and …

- Its cash payout is exploding, up an amazing 150% in the last decade!

How does this fund do it?

Simple: it’s run by an investment all-star team cherry-picked from 5 of the sharpest management firms on Wall Street.

Together, this crew invests in a “no-gimmicks” portfolio of value and growth stocks, all of which have deep moats protecting their businesses: names like Visa (V), Microsoft (MSFT), Alphabet (GOOGL) and Abbott Laboratories (ABT).

So how has this all-star team performed?

They’ve absolutely dominated, with most of my pick’s monstrous total return coming in cash, thanks to that huge dividend payout:

Crushing the Market in Cash

Finally, this fund trades at a 5.1% discount to net asset value (NAV, or the value of its underlying portfolio) as I write this. It’s only a matter of time before that shifts over to a big premium, pulling my pick’s market price higher as it does.

That’s not all! I’ll also give you 3 other cash-spinning CEF picks (combined yield: 8.7% for all 4 funds; price upside: 20%), too. Don’t miss out. Click here now!

Source: Contrarian Outlook