Generally speaking, summer is a lethargic time for the market. With investors thinking about vacations, ball games and cookouts, and in the absence of many catalysts, it’s just a slow time of year.

There are always exceptions though.

Granted, these exceptions are often born out of unusual circumstances, and may need the right nudge to realize their full potential.

Given how lethargic the summer of 2019 is shaping up to be though, investors looking to add a little extra zip to sleepy portfolios may want to take some strategic action.

With that as the backdrop, here’s a rundown of seven stocks to buy with the best shot at bucking the brewing stagnation and mustering a respectable summertime gain. They’ve already demonstrated some unusually impressive — and new — bullishness, but more may be in store.

Whirlpool (WHR)

The ongoing tariff war — and the ensuing economic headwind it has helped create — has prompted investors and analysts alike to identify those names that seem the most vulnerable. In so doing, investors have largely overlooked names that are able to shrug off those woes.

The ongoing tariff war — and the ensuing economic headwind it has helped create — has prompted investors and analysts alike to identify those names that seem the most vulnerable. In so doing, investors have largely overlooked names that are able to shrug off those woes.

That’s Whirlpool (NYSE:WHR) right now, says KeyBanc’s Kenneth Zener. He suggests the appliance maker is actually shelter (of sorts) from the storm, positioned to capitalize on what could turn into lower mortgage rates. It’s also somewhat of a beneficiary of a moderating economy; consumers may buy a dishwasher rather than purchase a new vehicle.

Simultaneously, even if out of necessity, the company’s cost-cutting initiatives are working. This year’s EBIT margin forecast of between 6.5% and 6.8% marks a 40 basis point improvement, though the company anticipates EBIT margins of more than 10% by 2020. That should be enough to drive profit growth of more than 10% this year and next.

The market has finally taken notice. After a rough 2018, WHR stock is up 40% from its late-December low, and up more than 20% since late May. Yet, the bulk of last year’s loss has yet to be reclaimed.

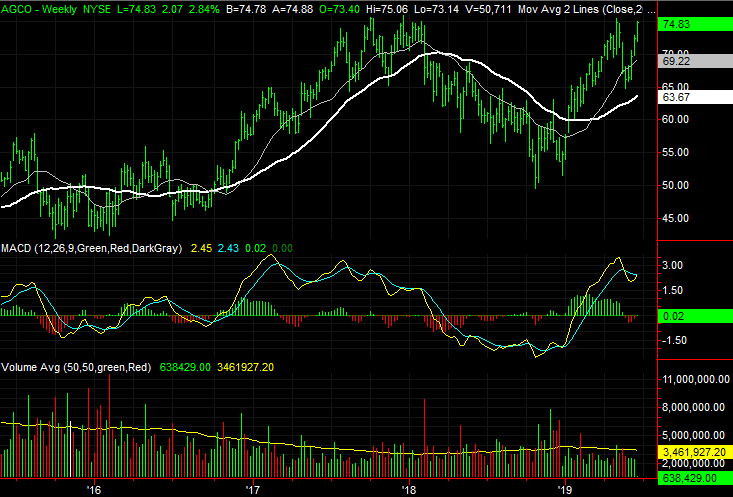

Agco (AGCO)

Given the uncertainty that has kept shares of farming equipment name Deere & Company (NYSE:DE) from moving forward for well over a year now, it would be easy to assume the same woes apply to smaller rival Agco (NYSE:AGCO). Indeed, a month ago, BofA Merrill made a point of saying that would be the case, lowering its stance on AGCO stock to “Underperform” in anticipation of falling demand.

Given the uncertainty that has kept shares of farming equipment name Deere & Company (NYSE:DE) from moving forward for well over a year now, it would be easy to assume the same woes apply to smaller rival Agco (NYSE:AGCO). Indeed, a month ago, BofA Merrill made a point of saying that would be the case, lowering its stance on AGCO stock to “Underperform” in anticipation of falling demand.

AGCO shares took a hit, unwinding a sizeable piece of this year’s 36% rally. Curiously though, AGCO didn’t stay down. It’s almost back to May’s highs, which are within sight of record highs.

That rebound likely has much to do with the fact that, rather than worrying about what may or may not happen in China, which is out of the company’s control, Agco is focusing on something it can control. That’s improving margins. CEO Martin Richenhagen said that plainly in a CNBC interview from last month, though recent investments in production as well as outright purchases of complementary companies also set the stage for better margins.

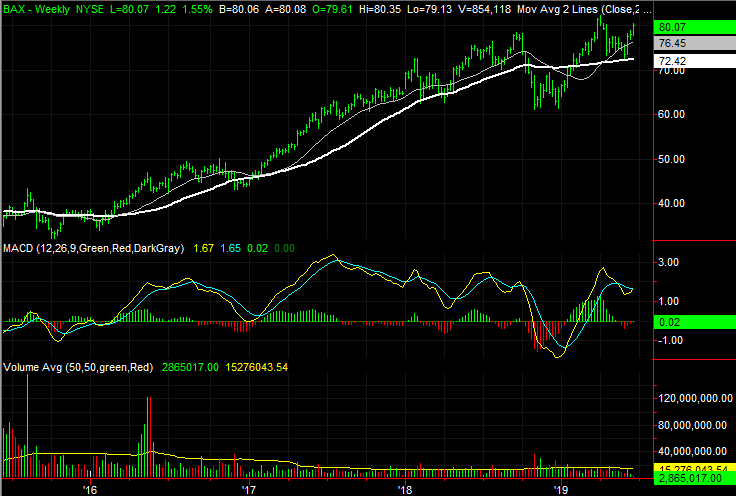

Baxter International (BAX)

Medical supply and equipment company Baxter International (NYSE:BAX) is never going to be a red-hot growth machine. But, what it lacks in explosiveness it more than makes up for in consistency.

Medical supply and equipment company Baxter International (NYSE:BAX) is never going to be a red-hot growth machine. But, what it lacks in explosiveness it more than makes up for in consistency.

Most investors would struggle to name one specific product Baxter offers. Millions of caregivers and patients would struggle with Baxter-made wares though. From infusion systems to surgical tools to kidney dialysis solutions, it does a little of everything for a lot of people.

That diversity is the key to its consistency, and while it would be untrue to suggest the company never fails to grow its business, it would also be untrue to suggest it doesn’t usually drive quarterly top-line growth. That’s a core reason BAX stock has been such a reliable performer. It’s also a key part of the reason BAX stock was able to shrug off last year’s stumble and reclaim all that was lost. Record highs are once again back in sight.

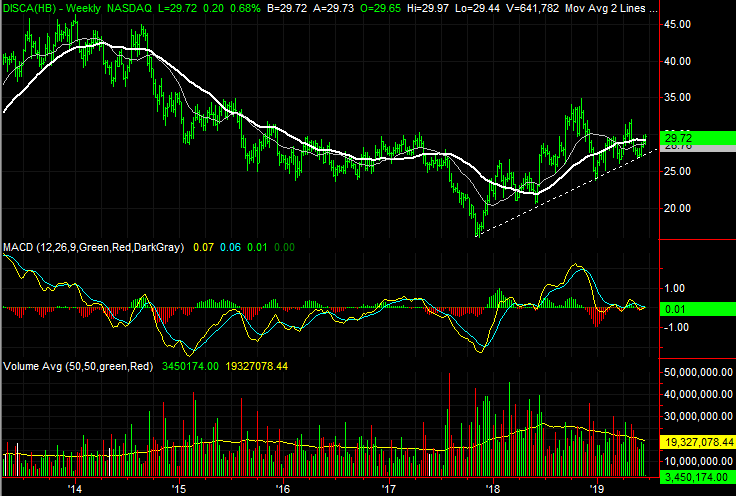

Discovery Communications (DISCA)

A recovery of most of the television production industry’s names certainly provided a tailwind, but Discovery Communications (NASDAQ:DISCA) has emerged from that sweeping turnaround as one of the hot stocks to buy again.

A recovery of most of the television production industry’s names certainly provided a tailwind, but Discovery Communications (NASDAQ:DISCA) has emerged from that sweeping turnaround as one of the hot stocks to buy again.

You know the company’s flagship and namesake television channel. But, it’s much more than that. Discovery is also the studio behind HGTV, Food Network, TLC, Animal Planet and the Oprah Winfrey Network … and more.

It’s a business seemingly with a cloudy future. The advent of all sorts of streaming options against a backdrop of cord-cutting would theoretically work against the company.

But, as few have fully appreciated, Discovery is wisely working with that tide rather than against it. Namely, it’s more likely to partner with the names disrupting the tradition television industry. Discovery’s content is available through YouTube, for instance, and Animal Planet is a choice on most so-called skinny bundles.

This willingness to rethink how to most profitably distribute content in an ever-changing market is a big part of the reason 2018 was so fruitful for DISCA stock after a rocky 2017. Revenue is projected to grow more than 5% this year, and next, accompanied by comparable profit growth. But, there’s still lots of ground for DISCA to make up from years of sub-par performance. A newly developed rising support line (white, dashed) is helping to do just that.

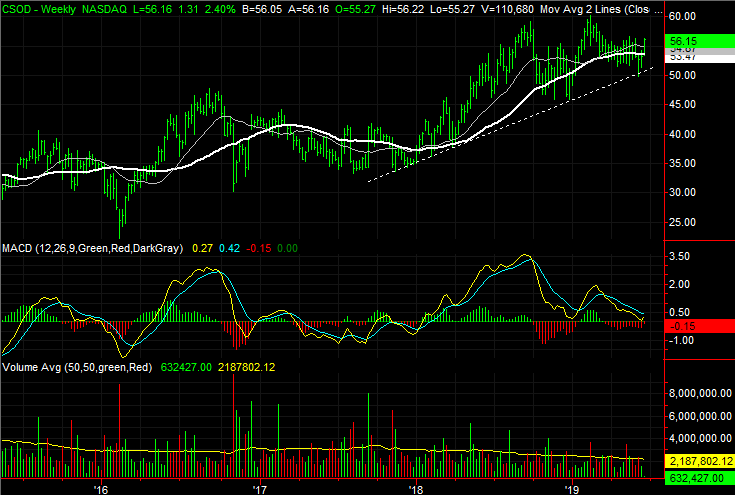

Cornerstone OnDemand (CSOD)

Cornerstone OnDemand (NASDAQ:CSOD) isn’t a household name, though it would be a nice addition to most household’s portfolios.

Cornerstone OnDemand (NASDAQ:CSOD) isn’t a household name, though it would be a nice addition to most household’s portfolios.

Cornerstone OnDemand offers cloud-based human resources management software. It’s not exactly riveting stuff, nor is it high growth. It’s got teeth though, but more than that, the company is currently in the middle of a major pivot. This year is the one where Cornerstone finally achieves enough scale to drive a profit explosion. Last year’s per-share earnings of 74 cents are expected to reach $1.04 this year, and jump 40% next year to $1.46 on sales growth that isn’t nearly as impressive.

Analysts agree that the business model and the recurring revenue it produces makes Cornerstone currently undervalued. The consensus target now stands at $64.11, or 14% above the stock’s current price. The uptrend that’s been in place since early last year, however, says CSOD stock is en route to that level.

Federal Realty Investment Trust (FRT)

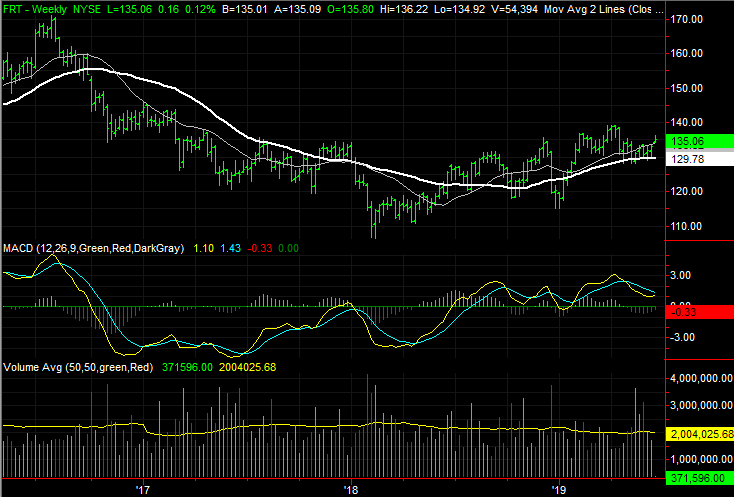

Any new exposure to the retail landscape, particularly in the current environment, isn’t easy to take on, even if the play is acting as a landlord to consumer-facing companies. Retail REIT Federal Realty Investment Trust (NYSE:FRT) isn’t nearly as vulnerable as it would be easy to assume it is, however, for a couple of reasons.

Any new exposure to the retail landscape, particularly in the current environment, isn’t easy to take on, even if the play is acting as a landlord to consumer-facing companies. Retail REIT Federal Realty Investment Trust (NYSE:FRT) isn’t nearly as vulnerable as it would be easy to assume it is, however, for a couple of reasons.

Chief among them is where Federal Realty Investment Trust sets up shop. Most of its properties make up an upscale destination for diners and shoppers, and aren’t as impacted as a rural shopping center or less affluent areas might be by economic turbulence.

The second reason FRT is taking shape as one of the best stocks to buy this summer? While the retail apocalypse may still be underway, it has become something more predictable and manageable. This REIT’s feel for development and redevelopment delivers the experience and mixed-use areas consumers want; much of the retail apocalypse was self-imposed by retailers that failed to keep their finger on the pulse of the market.

It’s a nuance investors largely missed a couple years back, but the 27% gain from its early 2018 low suggest they’re now remembering. The recent weakness is a chance to get into the bigger-picture uptrend at a bargain price.

Incyte (INCY)

Finally, add Incyte (NASDAQ:INCY) to your list of stocks to buy for the coming summer months.

Finally, add Incyte (NASDAQ:INCY) to your list of stocks to buy for the coming summer months.

Incyte is the name behind a drug called ruxolitinib, though it’s better known by its brand name Jakafi. It has proven to be an effective treatment for a handful of blood-related diseases, including a rare cancer called myelofibrosis and a similar condition called polycythemia vera. It may be a one-trick pony, so to speak, but when that pony is Jakafi, that’s ok. That one drug is expected to improve the top line by nearly 10% this year, and more than 16% next year, driving Incyte much deeper into the black.

Although it has been a compelling success story, INCY stock is no stranger to volatility. Those swings, however, have proven relatively predicable. A technical floor near $60 that took shape (again) last year ultimately served as a springboard for this year’s bullishness, and a former ceiling near $74 has since turned into a support level.

Now on solid footing, the bulls are starting to reach for higher highs, not unlike the beginning of the big move seen in 2016.

— James Brumley

Silicon Valley venture capitalist Luke Lango says this little-known Apple project could be 10X bigger than the iPhone, MacBook, and iPad COMBINED! Investing in Apple today would be a smart move... but he’s discovered a bigger opportunity lying under Wall Street’s radar -one that could give early investors a shot at 40X gains! Click here for more details.

Source: Investor Place