If your mattress is a bit heavy on cash these days, you’re probably grinding your teeth every day as the markets tick higher. Should you be in the market? Shouldn’t the market pull back eventually?

Here’s a solution that’ll get your “buy and hope” friends out of your face: buy some dividend machines that’ll pay you while the markets levitate and hold up just fine if we do see the dip we’re overdue for.

More on those in a moment.

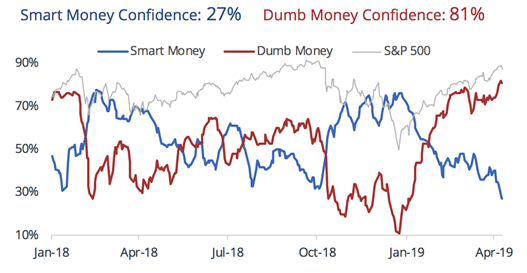

Beware the “Dumb” Money

First, when I say “cliff edge,” I’m not kidding around.

As I just wrote in my Contrarian Income Report service, I’ve recently grown wary of the market’s short-term outlook—and my unease goes well beyond first-level panic about the “inverted yield curve.”

The real reason to be wary is simpler: the “dumb money” hasn’t been this confident of further market gains since January 2018! Dumb was dumber back then, because stocks promptly collapsed:

Source: Sundial Capital

Source: Sundial Capital

(By the way, many individual investors would be categorized as “dumb money” because they get greedy when markets are hot and tend to buy high. Professionals—and savvy contrarian income-seekers like us—on the other hand, smartly buy the dips.)

This does not mean we’re going to cash. We need to keep our income and our nest egg growing, so we’re going after what I call “pullback-proof” dividends.

These high-yield “unicorns” have three weapons to deploy against the next market brushfire:

A. Big—and growing—dividends. I like to see a stock throwing off a yield of at least 4% (double the current average S&P 500 payout), backstopped by explosive payout growth.

B. Bargain valuations: For stocks and real estate investment trusts (REITs), this means low price-to-free-cash-flow (FCF) ratios; for high-yield closed-end funds (CEFs), we’re talking huge discounts to NAV (or market prices well below the value of the fund’s portfolio).

C. Rising sales to keep driving those dividends and gains—no matter what.

What’s the endgame on stocks like these?

Simple: they’ll hold their own in a meltdown, and when markets rise, their attractive payouts and cheap prices nicely set them up to outperform.

3 “Pullback-Proof” Dividend Buys—and 5 More Bonus Buys

With that, let’s move on to the three “pullback-proof” plays I have for you now. Then I’ll wrap by telling you about five “bonus” dividend payers hardwired to push back against the next crash. These five boast even bigger payouts—I’m talking massive cash hits all the way up to 8.5%!

Put it all together and you’re actually getting a free “8-pack” of dividend-payers to protect and grow your nest egg here. Let’s get going, starting with our three leadoff hitters:

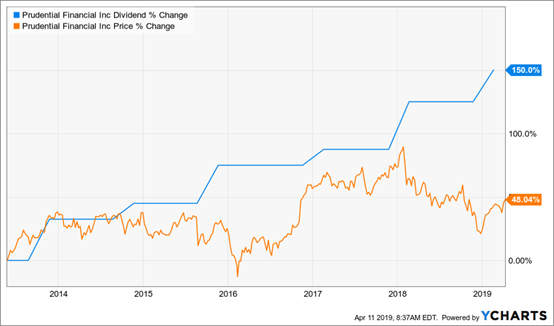

Prudential: “Cheap by any Measure”

The 21% surge from Prudential Financial (PRU) this year might make you think the easy money has been pocketed here. No way. Because this stock still ticks all three of our “pullback-proof” boxes.

For one, the insurer is cheap by any measure. Right now you can buy shares for 82% of book value—or less than what PRU would sell for if it were broken up and sold off! What’s more, PRU trades at a silly two times free cash flow! Downright insulting for a management team that’s grown sales 52% in the last five fiscal years.

Then there’s the dividend, which yields a nice 4.1% now and is growing like a weed:

PRU’s Supercharged Payout

If you’ve been following my articles on Contrarian Outlook, you know I’ve written before about a dividend’s power to yank share prices higher as it grows.

If you’ve been following my articles on Contrarian Outlook, you know I’ve written before about a dividend’s power to yank share prices higher as it grows.

PRU is a textbook example. As you can see above, the share price has jumped up to meet its payout over and over—until early 2018, that is, when the pair parted ways. That’s even more proof we’ve got a nice buy window now, before the stock gaps back up.

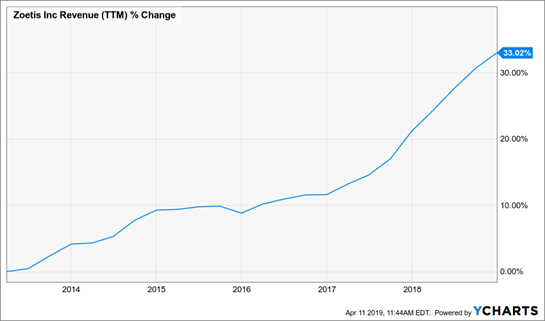

Zoetis: A Classic Megatrend Stock

My “unofficial” fourth requirement for a pullback-proof payout is a tie-in to a soaring megatrend. One of the biggest (and most overlooked)? The growing pile of cash we’re doling out on our furry pals.

Consider this: in 2009, total US pet spending clocked in at $45.5 billion. This year? An estimated $75.4 billion—a 66% rise in just a decade!

And Zoetis (ZTS), a maker of medicines for pets and livestock spun off from Pfizer (PFE) in 2013, is grabbing more than its share of that spending:

A Cash Machine

There are, however, a couple places where Zoetis does come up a bit short on our “pullback-proof” checklist.

There are, however, a couple places where Zoetis does come up a bit short on our “pullback-proof” checklist.

Let’s deal with those now.

First, the dividend looks lame at 0.7%. But that’s because investors bid up the price with each hike, keeping the current yield the same (because you calculate yield by dividing the yearly payout into the share price).

But if you’d bought in early 2013, the yield on your original investment would already be up 200%, to 2.1%. Going hand in hand with that increase are management’s stock buybacks, which have propelled the shares to a very speedy triple.

Share Count Down, Share Price Up

Second, Zoetis seems pricey at 34 times free cash flow. But as you can see below, that’s on the low end historically—another sign that now’s the time to move:

Second, Zoetis seems pricey at 34 times free cash flow. But as you can see below, that’s on the low end historically—another sign that now’s the time to move:

When Expensive Is Cheap

Finally, let’s …

Finally, let’s …

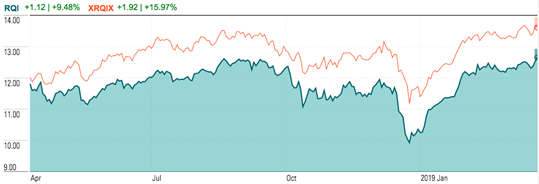

RQI: A Cheap—and Safe—7.5% Dividend

REITs are one of my favorite pullback plays because these landlords are obligated by law to pay 90% of their income as dividends, fueling some truly gargantuan payouts.

There’s just one problem.

REITs on a Roll

With the big run in REITs since the Fed suddenly became “patient” on interest rates, it’s been tough to find bargains here.

With the big run in REITs since the Fed suddenly became “patient” on interest rates, it’s been tough to find bargains here.

That’s where CEFs come in. By tapping their famous discounts to NAV, we can “rewind the clock” and tap into some of the hottest properties in the US at 2018 prices! Consider the Cohen & Steers Quality Income Realty Fund (RQI).

This stout CEF trades at a 7.1% discount to NAV. But as you can see below, that gap has almost completely closed in just the last year. So we’ve got plenty of “snap back” upside built in here:

RQI’s Buy Alarm Goes Off

Source: CEF Connect

Source: CEF Connect

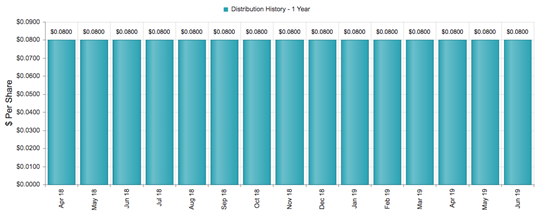

Here’s something else you need to know about this “all-in-one” real estate play: it rolls out an enormous dividend (7.5% yield!) every single month:

A Steady Monthly Cash Infusion

Source: CEF Connect

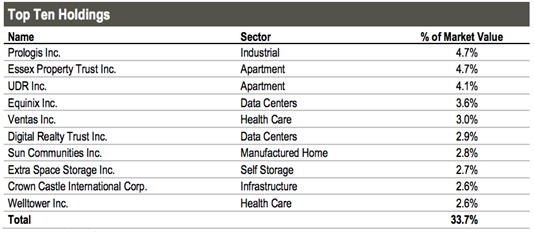

Finally, this portfolio focuses on the best REITs—industrial, residential, self-storage, data center and health care—while dodging retail, the perennial whipping boy of Amazon.com (AMZN).

Finally, this portfolio focuses on the best REITs—industrial, residential, self-storage, data center and health care—while dodging retail, the perennial whipping boy of Amazon.com (AMZN).

RQI Skips the Mall

Source: Cohen & Steers

Source: Cohen & Steers

With its 7.5% dividend and (nearly) matching discount, RQI is a solid “pullback-proof” candidate now.

— Brett Owens

My Top 5 Pullback-Proof Dividends (up to 8.5%)—Don’t Miss Out [sponsor]

Now let’s move on to those other five high-yield plays I mentioned above.

I’ve dropped them into a brand new Special Report—and I’m going to GIVE you your own copy now.

These five stocks have a lot in common with RQI, ZTS and PRU. But there are two key differences—and they both work in your favor!

- Higher yields: I’m talking 7.5% payouts, on average—and one of these cash machines throws off a mind-boggling 8.5% dividend.

- Bigger upside: This cash-spinning quintet is even cheaper than the three stocks above. That means you can dive in safely, knowing you’ve got even stronger downside protection—and even faster gains as the market grinds higher. I’m expecting 20%+ price upside in the next 12 months from each of these five dividend superstars.

The kicker? Because some of these plays pay dividends monthly, you can start tapping their income streams fast.

But a word of warning: all five of these stocks have edged higher in the market’s latest upswing. I know I don’t have to tell you that the higher they go, the more of that critical downside insurance we lose—and the smaller their dividend yields get.

Do not miss out! Click here to get full details on all five of these pullback-proof plays, with dividends up to 8.5%. You get everything I have on these ironclad stocks and funds: names, tickers, buy-under prices and more.

Source: Contrarian Outlook