If you’re confused about the direction of interest rates, don’t worry—Fed Chair Jerome Powell can’t figure it out either!

And today I’m going to show you 4 “Powell-proof” stocks set to explode in 2019—whether rates take off or freeze in place. First, back to Powell.

An Epic Flip-Flop

You may recall October 3, when the Fed chief, momentarily forgetting his words can tank the market, said, “We’re a long way from neutral, probably,” in reference to rates.

Here’s what followed:

Loose Lips …

Powell has since changed tack. His new line? Rates are now “just below” neutral.

Powell has since changed tack. His new line? Rates are now “just below” neutral.

Traders betting through the Fed Fund futures market took the bait. They now see the Fed hiking at next week’s meeting and then heading to the sidelines, possibly for all of 2019. That’s a huge shift from a few weeks ago, when they were handicapping 4 rate hikes next year.

Heads You Win, Tails You Win

So what the heck do we buy in this hall-of-mirrors market, where rates have a long way to rise one day and are just fine the next?

Here’s why: if rate hikes do tail off, you can bet first-level investors will flock back into dividend stocks—particularly those with yields of 3% or more, around the rate on the 10-year Treasury note now.

And if rate hikes pick up again, dividend growers win out, too.

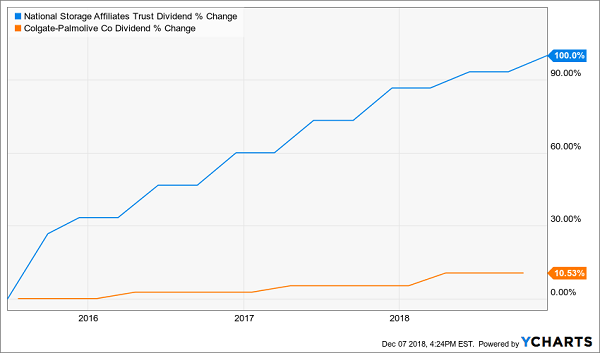

But we need dividend hikes that “outrun” the yield on the 10-year—not stale “bond proxies” like Colgate Palmolive (CL), which yields just 2.7% and dribbles out meager one-cent (and sometimes two-cent) annual hikes.

Compare Colgate with our next dividend grower and, well, there’s no comparison:

Colgate (Orange) is Barely a Dividend Grower

With payout growth too weak to grab the herd’s attention and boost the share price, CL has gotten crushed since the Fed started hiking rates 3 years ago:

With payout growth too weak to grab the herd’s attention and boost the share price, CL has gotten crushed since the Fed started hiking rates 3 years ago:

Weak Payout Growth = Weak Share Performance

So where does that leave us? Our “profit-either-way” plays should boast 2 things:

So where does that leave us? Our “profit-either-way” plays should boast 2 things:

- Current dividend yields at or above the 10-year Treasury rate, and

- Outsized—and ideally accelerating—dividend growth, to keep the payout ahead of interest rates and put some updraft under the share price.

Let’s dive into the 4 names I have for you now.

“Profit-Either-Way” Play No. 1: National Storage Affiliates

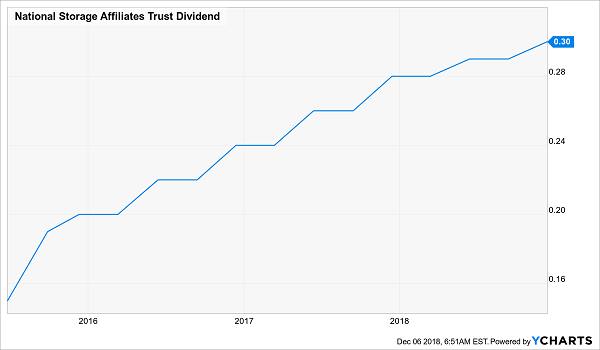

National Storage Affiliates (NSA) certainly ticks our dividend-yield box: with a 4.3% payout, it crushes the 10-year Treasury rate. And the payout is growing like a weed, having doubled in just the past 5 years!

In fact, management of this self-storage real estate investment trust (REIT) is so confident that it regularly hikes the dividend more than once a year. Check it out:

NSA’s Accelerating Dividend

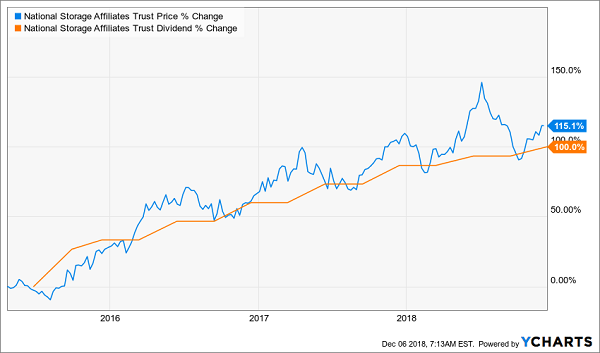

In other words, if you’d bought NSA a little more than three years ago, just after its IPO in April 2015, you’d already be yielding an incredible 9.5% on your original buy now, thanks to that rapid payout growth! And if you need any convincing that a rising dividend drives up share prices, NSA delivers that, too:

In other words, if you’d bought NSA a little more than three years ago, just after its IPO in April 2015, you’d already be yielding an incredible 9.5% on your original buy now, thanks to that rapid payout growth! And if you need any convincing that a rising dividend drives up share prices, NSA delivers that, too:

NSA’s Dividend Kick

NSA isn’t the cheapest REIT, trading at 20.8-times funds from operations (FFO—a better measure of REIT performance than earnings), but that’s more than fair given its accelerating dividend and surging FFO (up 9%+ in each of the last 4 quarters). Buy now, before the next payout hike sends this one higher.

NSA isn’t the cheapest REIT, trading at 20.8-times funds from operations (FFO—a better measure of REIT performance than earnings), but that’s more than fair given its accelerating dividend and surging FFO (up 9%+ in each of the last 4 quarters). Buy now, before the next payout hike sends this one higher.

“Profit-Either-Way” Play No. 2: AbbVie

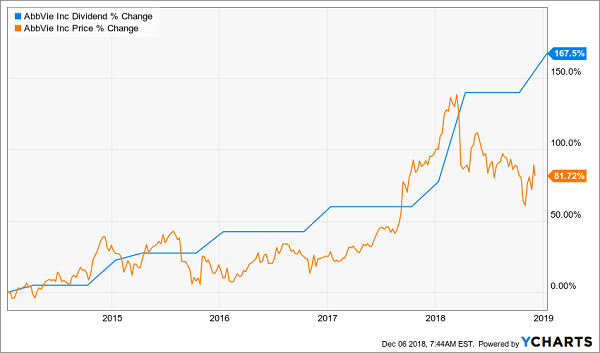

The selloff has made stalwart dividend grower AbbVie (ABBV) cheaper than it’s been in years, trading at just 11.5-times FCF. And talk about an accelerating dividend. This payout has nearly tripled in just 5 years!

But as you can see in the chart below, the dividend and the share price parted company starting in February, due to the overdone selloffs we’ve seen this year. That gives us plenty of upside as the share price inevitably rises to close the gap:

Selloff Gives Us Our In

The thing I love about AbbVie is that it maintains this payout growth while spending just 43% of FCF on dividends. That leaves lots for R&D, and that’s exactly where the company puts its cash, pumping a high 18% of sales into its development pipeline.

The thing I love about AbbVie is that it maintains this payout growth while spending just 43% of FCF on dividends. That leaves lots for R&D, and that’s exactly where the company puts its cash, pumping a high 18% of sales into its development pipeline.

And, yes, that pipeline is stuffed, with 38 development drugs, many of which are in Phase 3 trials or higher.

“Profit-Either-Way” Play No. 3: UDR Inc.

You may have seen my recent article about “pullback-proof” dividends. As the name suggests, these are wonderful companies whose share prices hold their own in a downturn, letting us collect their outsized dividends without losing sleep!

UDR Inc. (UDR) fits that description to a T; the apartment landlord’s stock didn’t fall nearly as far as the market did in this latest selloff, and it’s actually gained since Powell made his infamous “long way to go” comment in October:

Powell Can’t Sink This REIT

UDR is so steady it sports a “beta” rating of just 0.37 (anything less than 1 is more stable than the market, above 1 is less). So if you’re looking to add consistency to your portfolio, UDR should be high on your list.

UDR is so steady it sports a “beta” rating of just 0.37 (anything less than 1 is more stable than the market, above 1 is less). So if you’re looking to add consistency to your portfolio, UDR should be high on your list.

The REIT’s yield of 3.1% doesn’t really get our hearts racing, but hikes come year in and year out, like clockwork. The payout has grown a nice 37% in the last 5 years.

And that payout—which has gone out to shareholders for 46 straight years—is safe, eating up 73% of FFO, a very manageable level for a well-run REIT like UDR.

Finally, the stock trades at 23.7-times FFO, but it’s earned that multiple, given its stellar dividend history, modern buildings in growing coastal cities and sky-high 97% occupancy rate. Grab UDR now and let it steady your portfolio in the next meltdown.

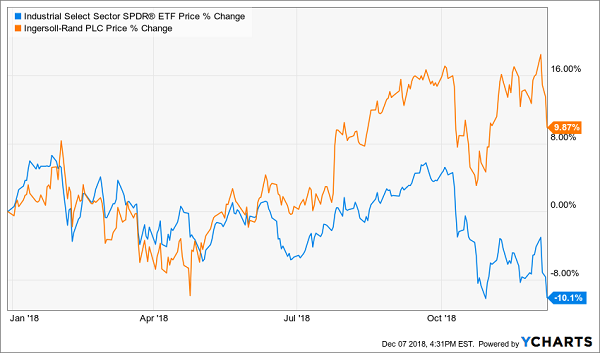

“Profit-Either-Way” Play No. 4: Ingersoll-Rand

Industrial stocks have taken a pounding this year, with the Industrial Select Sector SPDR ETF (XLI) plunging 9% amid worries about tariffs and slowing global growth.

But Ingersoll-Rand (IR) has bucked that trend, gaining 11%. And thanks to the selloff, it’s time to back up the truck on this hidden gem:

IR Shakes Off the Trade War

How is this possible?

How is this possible?

Simple: three-quarters of IR’s business comes from heating and refrigeration, locking it into the trend toward energy efficiency.

As CEO Michael Lamach recently told CNBC: “As the world gets warmer and more urbanized, people are concerned about greenhouse-gas emissions, and we’ve got solutions to eliminate 99.5% of those emissions in commercial buildings.”

If that doesn’t make IR a megatrend stock, I don’t know what does! And the numbers back that up: IR’s climate business is red hot, with bookings jumping 11% in Q3, and sales surging 10%.

You’re probably wondering how all this squares with President Trump’s trade war. The truth is, it’s not an issue: IR smartly makes most of the products in the US that it sells in the US; it does the same in the Chinese market.

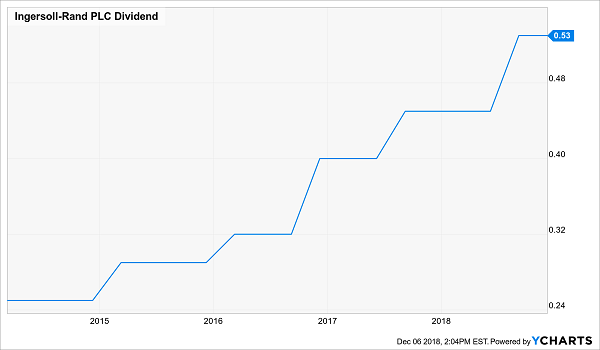

One place IR does fall a bit short is in its current yield: just 2.1%. But with a dividend that’s more than doubled in the last 5 years—and is accelerating—we’ll take that deal; the yield on our original buy will clear 3% in short order:

Trade War Rages; IR’s Dividend Accelerates

The kicker? Despite its big gain, you can still snap up this rare tariff-proof industrial stock at a bargain 15.5-times forward earnings.

The kicker? Despite its big gain, you can still snap up this rare tariff-proof industrial stock at a bargain 15.5-times forward earnings.

— Brett Owens

Exposed: My Top 7 Buys for Soaring Dividends and 100%+ Upside [sponsor]

If you’re considering devoting more of your cash to dividend growth in 2019—and you should be—you’ll want to take a close look at my top 7 stocks to buy now.

Each of the companies on this exclusive list is quietly handing investors growing income streams PLUS annual returns of 12%, 17.3% or more.

These hidden gems will double your initial stake in short order—no matter what happens in Washington or at the Fed.

So what stocks am I talking about? Here’s a snapshot of just 3 of these 7 low-key winners:

- This company is “locked in” for huge upside, trading at an absurd 6 TIMES free cash flow. The last time it was that cheap, it went on a monster 252% run!

- Another has $5 billion parked overseas. And thanks to tax reform, it’s set to drop that cash straight into shareholders’ pockets as dividends and share buybacks—but incredibly, the herd hasn’t picked up on this … yet.

- A third has been growing earnings by an astounding 129% since 2013 … but it’s so cheap you’d think it’s on death’s door!

It’s only a matter of time before investors twig to the incredible hidden assets these 7 unsung dividend-growth plays are sitting on. When they do, these stocks will gap higher—making now the perfect time to buy in.

Here’s the bottom line: these 7 stocks are growing their bottom lines—and dividends—so fast that they’ll DOUBLE your initial investment in 6 years (and that’s being very conservative).

But these bargains won’t last. Each of these 7 companies is just one positive headline away from its next surge higher, and you’ll want to be aboard well before then.

Don’t miss out! Click here to get everything I have on these 7 companies: names, ticker symbols, buy-under prices and everything you need to know before you buy.

Source: Contrarian Outlook