On average, an American retiree spends about $4,000 per month. But few of those retirees are getting $4,000 from their nest egg—which is partly why bankruptcy rates among retirees have been soaring for years.

And that’s the problem with today’s low-yielding stock market. To get $48,000 per year from the S&P 500, you’d need $2.76 million to put in the market. That’s because the S&P 500’s dividend yield is a crummy 1.7%—far lower than US Treasuries and way below its long-term average!

We can do better—and with little effort. For example, the 4 funds below will give you dividends that average out around $4,000 a month and diversify you across multiple asset classes, like common stocks, bonds and preferred stocks.

That gives you an extra margin of safety without limiting your income through “dead-end” investments like low-yield US Treasuries, which pay a pathetic 2.8% if you buy 10-year notes, meaning you’re guaranteed about a 0% return after inflation!

And speaking of inflation, don’t forget it hits retirees harder, since costs for things like health care grow much faster than what you’ll pay for many other routine purchases.

The bottom line?

We need to get more creative. We’ll start by doing an end run around US bonds and into bonds from some of the world’s biggest cash-producing international corporations. Now that corporate profits are rising in the double digits and company bankruptcies are falling, it just makes sense.

A New Approach to Income

We’ll need to do more than just buy a couple corporate bonds from a broker, though. That’s because brokers often sell some of the worst-quality bonds to smaller clients, since the big institutions have already snapped up the best issues.

But don’t worry; we can easily invest alongside the big institutions. To do it, we’ll use funds that diversify across hundreds of bonds while still paying big dividend yields. And we’ll use “smart beta” funds that avoid many of the pitfalls of dumb index funds, which force investors into a lot of losers alongside the winners.

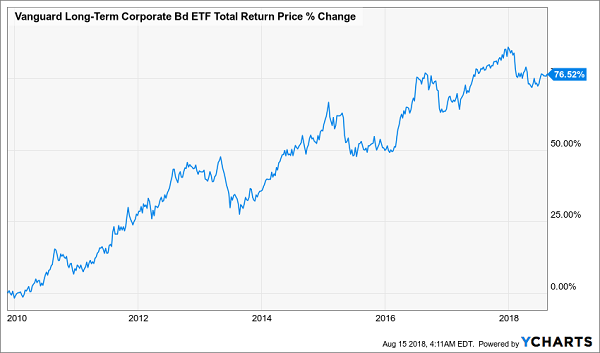

Which brings me to the first fund I want to show you today: the Vanguard Long-Term Corporate Bond ETF (VCLT), which pays a 4.4% yield that has helped this fund’s total return soar since its IPO nearly a decade ago:

High Yield Gooses VCLT’s Return

VCLT is attractive because it limits itself to investment-grade, high-quality companies and diversifies across 77 investments. Its biggest positions are in companies known for financial prudence and steady cash flow, such as Regions Financial (RF) and Dow Chemical (DOW), with the rest of the portfolio spread across other multinationals.

Big Dividends From Blue Chip Stocks

On top of bonds, our portfolio will need stock exposure, as well.

We all know the market has been on a tear since 2009, and while we can’t expect it to go up forever, we know that stocks have a tendency to rise steadily over the long term. We also know that dividend stocks tend to provide more reliable long-term growth and that we can count on the best ones to keep up their dividends in most market conditions.

So let’s get a piece of this action with two “smart beta” ETFs focusing on strong dividend-paying companies: the Global X SuperDividend US ETF (DIV) and the SPDR S&P 500 High-Dividend ETF (SPYD). With just these two funds, we’re getting a diversified portfolio of over 70 companies across different sectors, with exposure to everything from technology to real estate to health care.

You could get similar diversification with an index fund, like the SPDR S&P 500 ETF (SPY), but then you’d be stuck with dividends of 2% or less. No thanks!

Instead, DIV and SPYD can give us a diversified portfolio and an average dividend yield of 5.3%. And thanks to their stalwart portfolios, these funds have provided steady gains over the past year, in addition to their big dividend payouts.

2 “Steady Eddie” Picks

Even so, neither fund has fully caught the market’s attention to this point, but that’s not too surprising; both are relatively new, and many investors just don’t know they’re out there.

The Power of Preferreds

There’s one other secret that many investors aren’t really clued into: preferred stocks. They act like common stocks, but the market for preferreds is much smaller and tougher for everyday investors to get into.

That doesn’t mean they’re illiquid, though. Big institutional investors, such as hedge funds, love these things and buy them often. Back in 2008, Warren Buffett bought a ton of preferred stock in Goldman Sachs (GS), an investment that ended up getting him a 19% annualized return by the time he sold out.

So how can we follow the Oracle of Omaha’s lead? These aren’t the kinds of assets we can just buy through our online brokerage accounts; we need an insider’s help. Luckily, there are a few actively managed funds that give us just that. And they have big dividends, because preferred stocks tend to have much higher yields than common stocks.

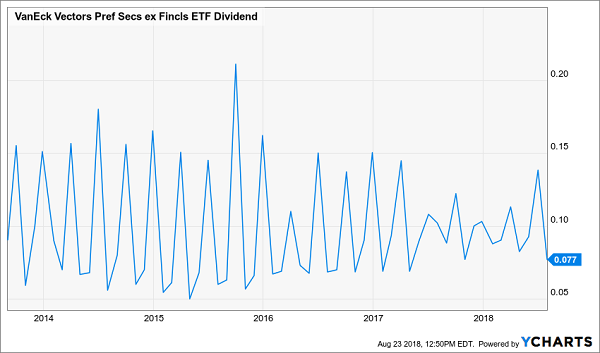

For instance, the Market Vectors Preferred Securities Ex-Financials Fund (PFXF) is paying a 6.0% dividend thanks to the 111 preferred stocks in its portfolio. And although the fund’s dividend is choppy because preferreds pay out at different times of the year, PFXF’s payout has remained around the same level, on average, over the last few years:

A Reliable Income Generator

Putting It All Together

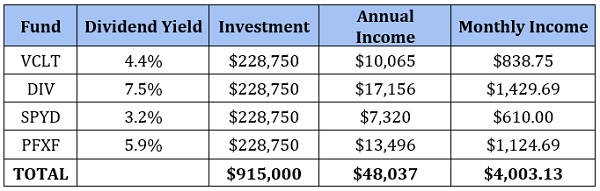

Combined, you can use only these four funds to get a bit over $4,000 per month in retirement income if you have $915,000 to invest. Here’s how the numbers break down:

With $228,750 in each fund, we’re getting a bit more than $4,000 in monthly income, thanks to the average 5.3% yield on these 4 funds. We’re also getting bonds, stocks and exposure to high-quality companies boasting familiar names and sterling profit histories.

— Michael Foster

Forget $915,000: Here’s How to Get $4,000 a Month on a Lot Less [sponsor]

But what if you don’t have $915,000? Or what if you have that kind of cash but want to have some left over—beyond the $4,000 a month the average retiree needs—to spend as you like?

It’s not impossible. In fact, it’s quite easy. With 5 other funds I’m pounding the table on now, we can goose those dividends all the way up to an average of 8.2%!

Think about that for a moment: at an 8.2% average payout, $915,000 will get you $75,030 in income, or over $27,030 more than the average retired couple spends!

And if you don’t have a $915,000 nest egg, don’t worry. These 5 largely unknown funds will still let you hit our $4,000-per-month income target on a retirement account that’s $325,000 smaller!

That’s not all. My team and I also fully expect 20%+ price upside from each of these 5 funds in the next year, because each one trades at a ridiculous discount to its “true” value—and that just can’t last.

That’s especially true when you consider the top-flight management teams at each of these superbly run funds. Like my No. 1 pick, an off-the radar fund that employs actual medical doctors and pharma researchers to pinpoint the companies set to release the next blockbuster drug.

The results speak for themselves:

Top-Flight Management Comes Through for Shareholders

Oh, and before you ask, yes, these yields are safe: all 5 funds easily generate enough investment returns on their holdings to cover their massive payouts, so you can count on this ironclad 8.2% dividend stream for years to come.

I can’t wait to show give you everything you need to know about these 5 little-known funds. Simply click here to get the full story and kick-start your own safe 8.2% income stream now!

Source: Contrarian Outlook