What could be better than a booming business that feeds an ever-growing dividend?

How about a “wide moat” to protect the payout’s upward trajectory? We’ll rank five dividend growers and their competitive advantages in a minute. First, let’s talk about disruption.

Tesla (TSLA) CEO and “Chief Disrupter” Elon Musk recently stormed the castle of investing theory when he challenged the importance of moats – the idea of corporate competitive advantages that make it difficult for other companies to whittle away market share.

I highly value economic moats as an important way to determine whether my long-term dividend holdings will be able to stand the test of time.

In fact, the five income plays I want to evaluate today all have sizable lakes defending their fortresses. But I’ll also say this:

On the topic of wide moats, both chiefs are right.

Musk’s attack on moats came during a quarterly earnings call when he was asked about why Tesla allowed its network of chargers to remain open to other carmakers, rather than closing it off, making it a “moat” of sorts. Musk’s response:

I think moats are lame. It’s nice sort of quaint in a vestigial way. If your only defense against invading armies is a moat, you will not last long. What matters is the pace of innovation. That is the fundamental determinant of competitiveness.

A couple days later, at Berkshire’s annual shareholder meeting, Buffett was told about Musk’s comment and actually acknowledged the idea that various moats were increasingly “susceptible to invasion” thanks to the march of technology, but ultimately still defended their worth and said companies should continue working to build those moats. He closed with a parting shot:

“I don’t think he’d want to take us on in candy.”

What followed that was a tongue-in-cheek Musk rant on Twitter in which Tesla’s top exec jokingly threatened to make his own candy company to challenge Berkshire’s famous See’s Candies holding – which he often points to when demonstrating the worth of “wide moats” – and even invoked the idea of “cryptocandies.”

This humorous back-and-forth between two of Corporate America’s greatest minds made for brilliant Wall Street theater, but it also laid to bare something that needed to be said: Wide moats, while an important quality to look for when selecting income investments for a retirement portfolio, still aren’t a guarantee of success – long-term or even short-term.

Today, I’m going to highlight five stocks yielding up to 6% that have enormous moats of one sort or another. And while some indeed reflect the worth that Buffett puts in this corporate quality, some demonstrate that even a gigantic lake isn’t enough to keep competition from burning the castle down.

Apple (AAPL)

Dividend Yield: 1.4%

Apple (AAPL) seems an odd start to this group of companies with wide moats, seeing as how Apple makes gadgets such as iPhones and iPads, and the personal-tech space is among the most crowded out there. The iPhone alone has competition from Samsung (SSNLF), Huawei, Oppo, Xiaomi, ZTE, LG and Lenovo (LNVGY), among a host of others.

But Apple does stand out as nearly untouchable in an important way: It caters to the upper crust. Owning an iPhone has essentially become a socioeconomic statement of sorts – one that commands a considerable premium and allows Apple to be one of the few companies to turn around smartphones at a profit. During Q4 2017, Apple only accounted for 18% of all global smartphones sold yet generated 87% of the industry’s profits – up from its 72% share in Q3. Considering Samsung accounted for another 10% of profits, and you quickly realize that there’s nothing but crumbs left for the dozens of other players undercutting one another to be relevant in the low-cost space.

Apple’s dominance of the premium space has allowed it to amass a legendary cash hoard, much of which it held overseas for years. Fortunately for investors, Apple is really starting to put it to work following the one-time repatriation mandated by Republicans’ corporate tax cuts. Apple recently said it will buy back another $100 billion in stock; it made the announcement during its quarterly report, in which it also said it had bought back $23.5 billion in shares during the prior three months, which was a record for any company.

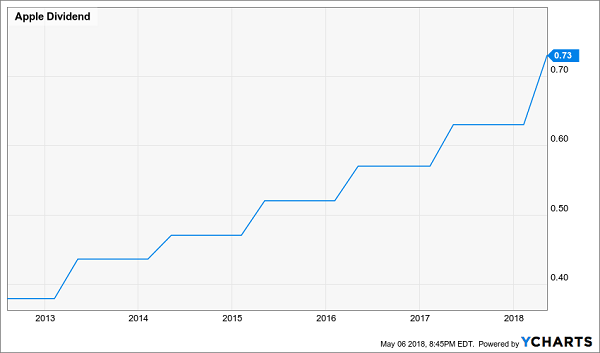

Also tucked into that report was a 16% dividend increase to 73 cents per share quarterly – its biggest hike on a percentage basis since it reinstituted its regular payout back in 2012. The dividend has now jumped about 93% since that time, fueled by the absurd margins on the iPhone and Apple’s other tech products.

Apple (AAPL) Turns Pricey Smartphones Into Giant Dividend Hikes

Grupo Aeroportuario del Pacífico, S.A.B. de C.V. (PAC)

Dividend Yield: 3.2%

Airline operators have pretty natural wide moats. It’s a brutally competitive space on price, and one where fluctuations in oil prices can make a quarter’s profits or chop it at the knees. It’s uncommon that the industry actually adds a competitor.

That’s nice. But if you’re looking for a real lack of competition, consider the companies that operate airports. Very few cities have multiple airports in the first place, and those that do have mostly stared down their competitors for a long time. It’s downright rare to see a city tack on a new airport.

Grupo Aeroportuario del Pacifico (PAC) is the largest airport operator in Mexico, running 12 of the country’s airports in total, including five of the 10 most important airports by passenger traffic. Its portfolio includes:

- Major airports: Guadalajara and Tijuana

- Mid-size airports: Mexicali, Hermosillo, Los Mochis, Aguascalientes, Guanajuato and Morelia

- Tourist-centered airports: La Paz, Los Cabos, Manzanillo and Puerto Vallarta

Grupo Aeroportuario also has a presence in Jamaica, operating Montego Bay Airport and owning Desarrollo de Concesiones Aeroportuarias, which controls a majority stake in the operator of Sangster International Airport.

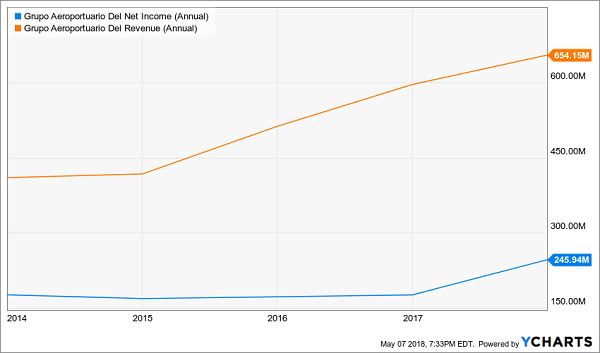

Air travel is rapidly growing in Mexico, and the company’s results continue to reflect that. Earlier this year, Grupo guided 2018 traffic growth at 8% year-over-year, revenue growth at 13% and EBITDA at 13%. Total terminal passengers for the first quarter improved by 12.9%, revenues ended up growing by 12.9%, first-grew 7.6% and EBITDA jumped by about 12.8%, so the company seems well on its way to meeting its set goals.

Moreover, PAC has been growing its dividend like a weed, including a 33% boost in the annual payout (divided into two payouts to be paid in August and December), agreed upon at its regular shareholders meeting in April.

Grupo Aeroportuario (PAC): Don’t Drink the Water, But the Air Is Just Fine

Host Hotels and Resorts (HST)

Dividend Yield: 4.0%

Host Hotels and Resorts (HST) is the largest hotel real estate investment trust (REIT) there is, holding 90 U.S. and six international properties spanning roughly 53,000 rooms, leased out to luxury players such as Hyatt (H), Hilton (HLT) and Marriott (MAR), as well as a number of smaller resort operators.

The company isn’t shy about its competitive moats, either, and in fact displays them for all to see on its basic company overview page:

Superior Diversified Portfolio – Own a geographically diverse portfolio of hotels located in major urban centers and resort destinations with relatively higher barriers to entry.

As we see with Apple, there’s something to be said about catering to the upper classes. It’s one thing to try to outpunch the likes of Motel 6 near the airport, but it’s another to try to go into a major metropolitan or resort area and try to build a following against established hotels with sterling reputations in an industry in which rewards programs foster strong brand loyalty.

The company had a great first-quarter. In addition to growing net income 59% year-over-year, it also upgraded its full-year 2018 guidance on several fronts. A few highlights:

- Total comparable hotel RevPAR, from 0.5%-2.5% growth to 1.5%-2.5% growth

- Net income, from $547m-$616m previously to $617m-$657m

- Adjusted FFO per diluted share, from $1.60-$1.70 to $1.67-$1.73

I do have one complaint: Host’s dividend has been stagnant for years, at 20 cents quarterly, and that’s more problematic when you consider HST’s merely OK yield of around 4%.

But given Host’s market positioning and dominance among the upscale hoteliers, this is at worst a safe REIT and at best a potential growth play going forward.

Anheuser-Busch InBev (BUD)

Dividend Yield: 4.5%

Anheuser-Busch InBev (BUD) is one of the globe’s megabrewers, responsible for a number of massive brands including Budwesier, Corona, Stella Artois, Beck’s, Hoegaarden and Foster’s. And for years it enjoyed a wide moat in that there were few serious competitors to its big-brand empire.

But my, how things have changed.

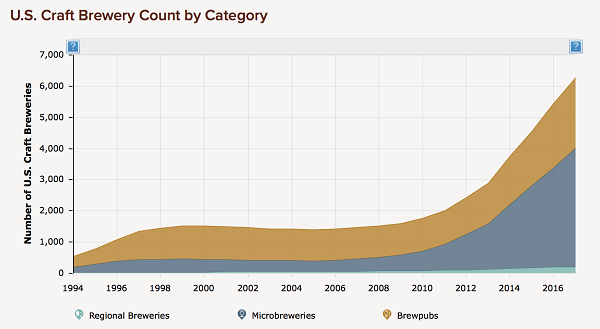

Craft Breweries Have Exploded Over the Past Decade

Source: Brewers Association

Now, Anheuser-Busch InBev still has a significant moat in that its distribution network is enormous – those thousands of craft brewers simply can’t produce at InBev’s level, nor can they reach the outlets InBev can. Nor can they compete on price, for that matter.

However, those craft brews are increasingly gobbling up market share, with volume share leaping from 7.8% in 2013 to 12.7% in 2017. In response, Budweiser has been trying to buy up well-known craft brands – such as Kona, Devils Backbone and Goose Island – to make up for growing weakness in its core Budweiser products. But Budweiser can only buy up so many brands, and it’s still not able to make up for the declines in its core mega-brands.

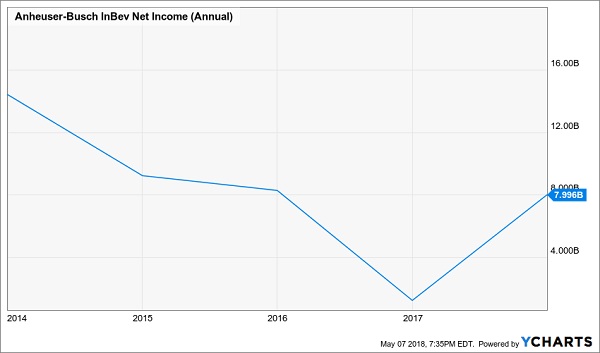

I panned Anheuser-Busch InBev a few months ago, and it is off a few more percent since then versus a slight recovery in the S&P 500. I think the craft trend will continue weighing on Budweiser long-term, keeping it from ever being the growth play it once was.

Anheuser-Busch InBev’s (BUD) Bottom Line Lacks Fizz

AT&T (T)

Dividend Yield: 6.1%

AT&T (T) has such a wide moat in the U.S. telecommunications market that it’s said it holds a “virtual duopoly” alongside Verizon (VZ). Yes, there are other competitors, such as lower-cost providers such as pending merger buddies Sprint (S) and T-Mobile (TMUS), or regionals such as Cellcom or Bluegrass Cellular.

It also has as high of a yield as you can find on a traditional stock without having to worry that the dividend is in significant jeopardy.

But ultimately, AT&T’s moat is only good for defense – and lately, even that’s not holding up too well.

AT&T shares were hit hard recently after its first-quarter earnings report failed to impress Wall Street’s pros. Earnings of 85 cents per share were 2 cents short of expectations, while revenues of $39.3 billion were about $1.3 billion shy. Linear video subscribers dropped by 187,000 in Q1, too, as users continue to migrate to streaming options. Meanwhile, U.S. postpaid wireless additions were a mere 49,000 as it continues to tread water in a fully saturated American market.

That means all focus is on AT&T’s bid to buy Time Warner (TWX), which currently is being fought in court against the Justice Department. A win would at least allow AT&T one avenue of growth by putting it in the content game, but at this point, it’s still just a gamble.

— Brett Owens

The Best Moats to Retire On: 8% Dividends Paid EVERY MONTH [sponsor]

If you’re looking for steady dividend income today, don’t settle for stocks like BUD and AT&T that are banging their heads against the wall. Instead, I recommend my handpicked portfolio of payout winners that will not only pay you far more, but will pay you 3x more often.

When you retire, chances are you’ll be relying heavily on dividend income to get you through your regular expenses: the house, the car, power … you name it. But while most publicly traded companies tend to pay dividends out quarterly, your bills sure aren’t quarterly. They come every single month, rain or shine.

That’s why monthly dividend stocks make so much sense for long-term retirement planners. A reliable stream of income that doesn’t vary from month to month allows you to budget with precision. And with the right plan, you can collect $3,000-plus in dividends every single month – and do it with a smaller nest egg than even the suits at Merrill Lynch say you need to retire well.

My “8% Monthly Payer Portfolio” checks off every box investors need from retirement:

- Monthly income to use against your monthly bills.

- Dividends large enough to allow you to live off investment income entirely. That means no selling your stocks and shrinking your nest egg, which ultimately shrinks your regular dividend paycheck.

- Better returns on any dividends you choose to reinvest. If you don’t need the income from your portfolio right away, you don’t have to wait every three months to put dividends to work – you can sink them back into new investments just about every 30 days!

These monthly dividend payers include a few picks that have remained mostly under the radar despite their high payouts and general quality. For instance, this portfolio includes an 8.7% payer trading at a bizarre 5.3% discount to NAV, and an 8.5% payer that not 1 in 1,000 people even know about.

Because these big dividends compound quicker, they’ll turbocharge your net worth and allow you to enjoy the retirement you’ve worked so dearly to reach. Don’t delay! Click here and I’ll send you my exclusive report, Monthly Dividend Superstars: 8% Yields with 10% Upside, for absolutely FREE.

Souce: Contrarian Outlook