Many investors will tell you gold is the ultimate safe haven, but here’s the thing – silver is poised to deliver extreme outperformance over the next several years.

Let me explain how I know this.

So I know silver is, without a doubt, the most undervalued resource right now, based on a number of metrics.

In fact, some of the best research to be gleaned on this very topic comes from the Silver Institute’s World Silver Survey 2018, the 28th annual edition of this global analysis.

For anyone studying the sector as I do, it’s an indispensable tool providing an in-depth view of the state of the silver markets.

And for those who don’t study it, I’m going to show you my condensed review of this year’s survey, as well as a suggestion for how you can leverage silver’s bullish outlook.

Let’s take a look…

Survey Analysis No. 1: Silver Demand

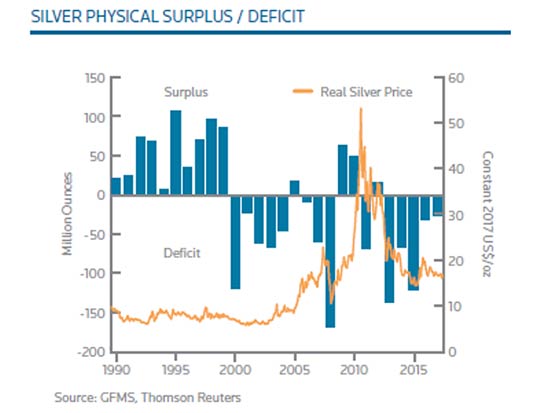

2017 marked the fifth consecutive year of deficit in the world silver market. Though smaller than in recent years, the 26 million-ounce shortfall was still significant.

Total supply of 991.6 million ounces was unable to keep up with total physical demand of 1,017.6 million ounces. Stockpiles once again had to be tapped to make up the difference.

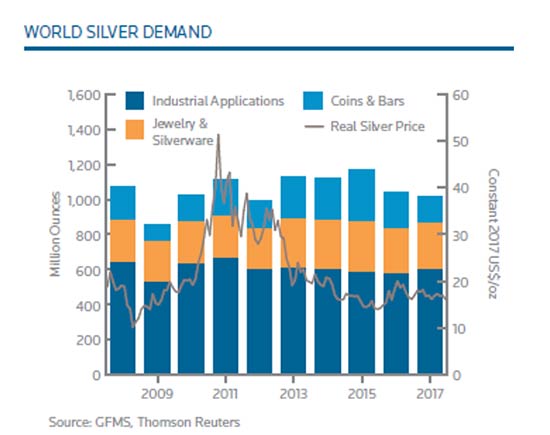

Demand from industrial silver applications grew by an impressive 4% last year, reaching 599 million ounces and accounting for nearly 60% of total physical demand. 2017 marked the first increase in silver industrial fabrication since 2013.

The biggest contributor by far was photovoltaic (solar panels), which required 19% more silver thanks to a massive gain of 24% in worldwide solar panel installations.

Industrial applications like brazing alloy and solder silver enjoyed a 4% year-over-year increase to 57.5 million ounces, with China and Japan fueling most of that growth. At the same time, the automotive sector remained robust from a silver demand perspective.

The production of semiconductors was foremost within the electrical and electronics segments to help this category enjoy its first demand increase since 2010, representing 243 million ounces in 2017. Silver used to produce ethylene oxide (mainly for industrial chemicals) and in photography saw decreases last year, with the latter application seemingly stabilizing.

Silver jewelry demand was up 2%, to 209 million ounces, with India as the main contributor, as that nation’s volumes rose 7% year over year. In addition, the United States showed a strong 12% increase, setting its own all-time demand high. Silverware’s demand increase was a robust 12%, reaching 58.4 million ounces, as India led with a healthy appetite here as well.

Physical investment demand was the one silver subsector that decreased, contributing to an overall physical demand drop of 2% as coin and bar demand fell by 27%. That most likely was the result of waning sentiment as equities gained globally and attracted capital. However, total world demand of exchange-traded products (ETP) gained by 2.4 million ounces, to reach 669.8 million ounces.

Survey Analysis No. 2: Silver Supply

Now, let’s drill down and have a close look at what developments there were on the supply side.

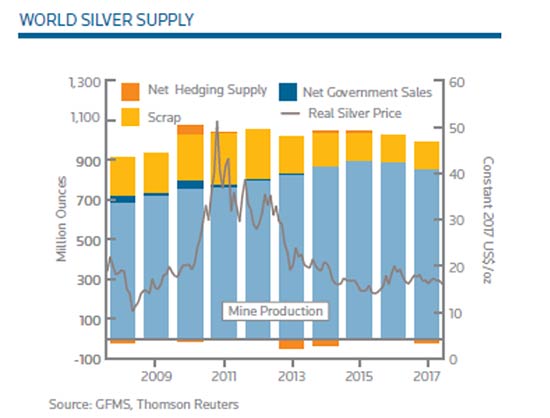

World silver mine supplies dropped 4.1% last year, falling to 852.1 million ounces and marking the second consecutive year of decline. A number of mine disruptions in the Americas and faltering output at primary silver and gold mines led to 36.5 million fewer ounces.

Guatemala was the standout, bringing 15.3 million fewer ounces to market. Both Peru and China registered small output drops, but Australia and Argentina recorded more significant drops, while Mexican output saw a boost in production.

Accounting for credits from byproduct metals, like gold, lead, and zinc, led to a drop in total cash cost plus capital expenditures of $10.54 per ounce, a decrease of 5% over 2016. So producers have been getting leaner.

Soft silver prices also contributed to weaker scrap supply, which fell to 138.1 million ounces, marking the sixth consecutive year of deterioration. Asian scrap supplies from industry and consumers were down, while supply was mildly higher in the West, with Europe and the United States leading.

As you can see, with decreasing mine output and robust demand, the fundamental picture for silver couldn’t look any better. Investment demand remains the wildcard, and I think an imminent shift in sentiment will soon power silver prices higher.

So, without further ado, here’s my favored way to partake in the upside ahead for the most undervalued resource.

Play the Silver Upside

The Global X Silver Miners ETF (NYSE: SIL) is an ideal choice for investors wanting exposure to silver equities.

It’s a one-stop buy that gives you instant diversification across the biggest silver miners on the planet, with $400 million in assets allocated to over two dozen silver producers. These include Wheaton Precious Metals Corp. (TSE: WPM), Fresnillo Plc., Pan American Silver Corp. (TSE: PAAS), Coeur Mining Inc. (NYSE: CDE), Tahoe Resources Inc. (TSE: THO), SSR Mining Inc. (TSE: SSRM), and Hecla Mining Co. (NYSE: HL).

Holdings are somewhat geographically diverse as well, with 39% allocated to Canada, 18% to Mexico, 13% to Russia, 12% to the United States, 12% to South Korea, and 6% to Peru.

The 2018 World Silver Survey demonstrates that, with supplies remaining challenged and fabrication demand at elevated levels, it won’t take that much for revived investment demand to kick silver prices into high gear.

— Peter Krauth

According to one of the world's top AI scientists, there's a major event coming as soon as three months from today that could cause expensive tech stocks like Microsoft, Google, and NVIDIA to double or triple in price in the months ahead... but whatever you do, don't go all in on big tech before you have all the details. Click here.

Source: Money Morning