The biggest complaints about the Dividend Aristocrats tend to come from new money. That’s because many of them, while generously raising their payouts year after year, offer skinflint yields that average 2.35% – almost right on par with the 10-year T-note.

You can find a little more relief from a similar club: The High Yield Dividend Aristocrats. This is a group of roughly 110 S&P Composite 1500 stocks that has paid and increased dividends for at least 20 consecutive years.

I’ll beat this idea like a drum: Dividend growth is a vital component of any retirement portfolio.

While you need a high enough income yield to ensure you can pay the bills once your salary is gone, dividend growth will ensure that inflation doesn’t erode the buying power of those regular payouts – and ensure that you always have enough to live on.

But dividend growth also acts as a telltale sign of equity quality.

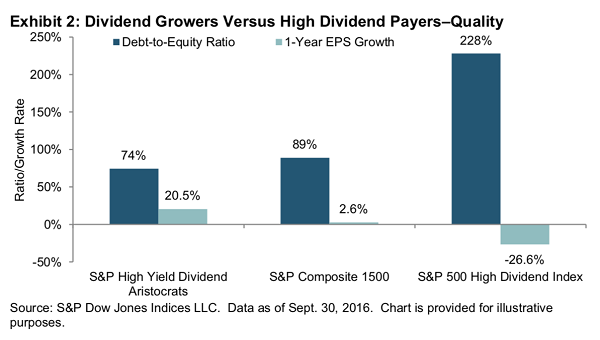

Consider a 2016 study from S&P Dow Jones Indices on dividend growth strategies, which compares the S&P 500 High Dividend Index, S&P Composite 1500 and S&P High Yield Dividend Aristocrats.

Not only does this group of high-yield royalty deliver payout growth – its stocks also boast more tenable debt-to-equity situations and far better earnings growth.

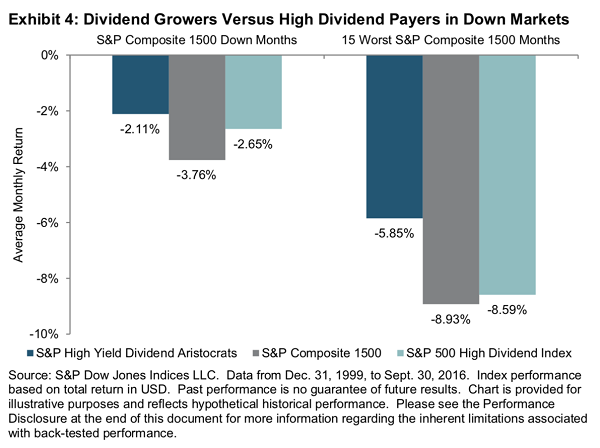

The same study shows how resilient High Yield Dividend Aristocrats are in down markets.

The same study shows how resilient High Yield Dividend Aristocrats are in down markets.

Long story short? On the whole, these high-yield dividend growers can punch far above their weight. But, like with any group of stocks, you need to be selective – if they were all gems, no one would own anything else.

Long story short? On the whole, these high-yield dividend growers can punch far above their weight. But, like with any group of stocks, you need to be selective – if they were all gems, no one would own anything else.

That said, here are the best and the worst of the High Yield Dividend Aristocrats:

People’s United Financial (PBCT)

Dividend Yield: 3.7%

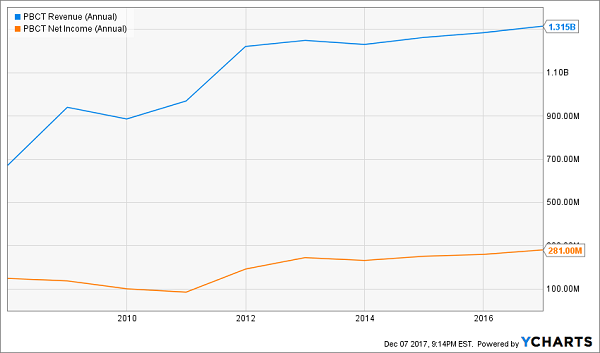

People’s United Financial (PBCT) is a mid-cap regional bank stock that operates as People’s United Bank. The bank boasts more than 300 branches across the Northeast – states such as Massachusetts, Vermont and Connecticut, among others.

There’s nothing out of the ordinary about People’s – it provides retail banking services such as checking and savings accounts, commercial banking and wealth management products.

But it’s hard not to love what’s underneath the hood. People’s has rebounded well out of the 2007-09 bear market and financial crisis, and has grown its top and bottom lines each year since 2014. People’s United is on track to finish 2017 up as well, and Wall Street analysts project more of the same going into 2018. Investors should feel even more optimistic about next year, as Jerome Powell – President Donald Trump’s nominee to replace Janet Yellen as the Federal Reserve’s chair – said he supports “tailoring” regulations to take some weight off the backs of smaller banks, which is good news for the likes of PBCT.

People’s United also is a serial dividend raiser that has boosted its payout for 24 consecutive years. Considering the prospects for better business, a potentially more friendly regulatory environment and tax cuts, PBCT should be able to keep its foot on the dividend pedal.

People’s United (PBCT): Mid-Size Stock, King-Size Results

Kimberly-Clark (KMB)

Kimberly-Clark (KMB)

Dividend Yield: 3.2%

It rarely pays to bet against consumer staples stocks. After all, their recession-resistant wares and typically sturdy dividends will ensure that they stay afloat. But your objective in retirement isn’t to tread water – it’s to get ahead.

Kimberly-Clark (KMB), despite its 45-year streak of consecutive dividend hikes, won’t get you there.

Yes, this staples giant boasts incredible geographic reach of 175 countries, with the company claiming that a quarter of the world’s population uses KMB products such as Huggies diapers, Kleenex tissues and Scott paper towels.

But conscientious “mom-sumers” are gravitating away from the likes of Kimberly-Clark and toward companies such as Jessica Alba’s Honest Co., which offer “non-toxic” baby products. Thus, despite expanding economies in the U.S. and across the globe, Kimberly’s revenues have been thinning out for years. In fact, 2017 is an outlier in that the company should deliver top-line growth – but just 0.5% worth, or so Wall Street’s pros expect.

Tanger Factory Outlet Centers (SKT)

Dividend Yield: 5.6%

2017 has been a mostly grim year for retail, with mall-based operators such as JCPenney (JCP), Sears (SHLD) and Macy’s (M) plunging between 30% and 60% as Amazon.com (AMZN) sucks the life out of brick-and-mortar rooms.

Retail REITs – some of which own the malls that are suffering from store closures and lower occupancy – have cracked, too. But a few babies are being thrown out with the bathwater.

Take Tanger Factory Outlet Centers (SKT), for instance.

Tanger owns, operates or has an ownership interest in 44 upscale outlet malls across 22 states, featuring stores that are diversified across 510 different companies – factory stores from Adidas (ADDYY) and Ecco to Kate Spade and Tumi.

Now, SKT has been absolutely pelted this year, to the tune of 26%, which has juiced its dividend yield to its highest point since 2009. But the company now boasts 56 consecutive quarters of same-center net operating income, continues to grow adjusted funds from operations and even raised its year-end occupancy guidance to 96.5%-97%.

Investors should be cautious about the retail space, but the selloff in Tanger is grossly overdone. New money has a chance to jump into a quality, high-yield name that doesn’t face the same pressures as traditional mall retailers, and at a value price of just 12 times FFO. And next year, investors likely will take part in what would be the company’s 25th consecutive annual dividend increase.

National Retail Properties (NNN)

Dividend Yield: 4.6%

In the same vein is National Retail Properties (NNN), which has lost about 6% this year – not as ugly as Tanger’s result, but undeserved nonetheless considering what the company has to offer.

National Retail Properties is a retail-centric REIT, yes. But this isn’t a traditional mall operator – instead, the company focuses its energy on single-tenant leases to businesses such as Sunoco gas stations, LA Fitness gyms, SunTrust (STI) banks, AMC Theaters (AMC) and Frisch’s restaurants.

You see any real potential Amazon victims there? I don’t. I also don’t see an occupancy problem, either. Portfolio occupancy was 98.8% as of Sept. 30, admittedly down year-over-year, but consider this – the company’s lowest rate in 14 years was still a high 96.4%, and NNN’s average remaining lease still has 11.4 years left on it.

Better still, this REIT operates via “net leases,” which put the onus of things such as property taxes, insurance and repairs on the tenant – NNN simply cashes the rent check, which makes its operations far more consistent and predictable.

That helped National Retail Properties deliver its 28th consecutive annual dividend hike this year. The REIT bumped its quarterly payout up by 4.4% to 47.5 cents per share as of its late July distribution, and should continue to reward investors in a similar matter for years on end.

Target (TGT)

Dividend Yield: 4.1%

Target (TGT) – also a member of the actual S&P 500 Dividend Aristocrats, at 46 straight dividend hikes and counting – is starting to show a little fight in the back half of the year after cratering since late 2016. That’s in large part because of optimism about the holiday shopping season, with more customers hitting stores than expected.

The problem is, more people shopped online, and from mobile, than ever before – and that doesn’t play into Target’s hand.

Amazon.com has long been eating the lunch of large retailers such as Target and Walmart (WMT). But while the latter has fought back strong via its purchase of Jet.com, Bonobos and other online operators, the former has become relatively stagnant – its most recent big online initiative is GiftNow, a neat feature that allows people to send gifts online, then allows recipients to swap colors and sizes. It’s great, but so far this year, Walmart has been the web’s growth juggernaut, growing online sales 50% in the third quarter – more than double Target’s growth rate.

Speaking more broadly, Target simply can’t and doesn’t compete on price as well as Walmart does, with its only positive differentiation being the in-store experience – something that’s becoming less important as e-commerce takes up a bigger portion of the pie. That’s reflected in Wall Street’s expectations, with the pros forecasting a mere 2.4% rebound in sales, then another decline in 2019.

Target may be a more appealing brand than Walmart, but as an investment going forward, it’s second-rate.

— Brett Owens

3 Ways to Safely Bank 8% Dividends [sponsor]

Most of the stocks you read about in the mainstream media that pay 5% or better are train wrecks. They have big stated yields for the wrong reason – namely, because their prices have been axed in half or worse over the past year!

For example, retailer Macy’s (M) pays 7%+ on paper. But its business model is toast. Next quarter’s payment may happen, but that’s a risky game I’m not willing to play.

Instead, I’d rather look in corners of the income world that aren’t combed over as regularly. There are three in particular that I like today. You won’t hear about them on CNBC, or read about them in the Wall Street Journal, because they don’t buy advertising like Fidelity and other firms.

Their relative obscurity is great news for us 8% dividend seekers.

Play #1: Closed-End Funds

If you feel trapped “grinding out” dividend income with classic 3% payers (like dividend aristocrats), you can double or even triple your payouts immediately by moving to closed-end funds, or CEFs. In fact, you can often make the switch without actually switching investments.

I’ll discuss my favorite CEFs in a minute.

Play #2: Preferred Shares

Not familiar with preferred shares? You’re not alone – most investors only consider “common” shares of stock when they look for income.

But preferreds are a great way to earn 7% and even 8% yields from the same blue chips that only pay 2% or 3% on their “common shares.”

I’ll explain preferreds – and my favorite tickers to buy – after we finish our high yield hat trick.

Play #3: Recession-Proof REITs

The IRS lets real estate investment trusts, or REITs, avoid paying income taxes if they pay out most of their earnings to shareholders. As a result these firms tend to collect rent checks, pay their bills and send most of the rest to us as a dividend. It’s a sweet deal.

Not all REITs are buys today, however – landlords with exposure to retail space should be avoided.

That’s easy enough to do. I prefer to focus on REITs that operate in recession-proof industries only. I want to receive my rent check powered dividends no matter what happens in the broader economy.

Now let’s discuss how you can get a hold of my complete “8% No Withdrawal Portfolio” research today, along with stock names, tickers and buy prices. Click here and I’ll share the specifics – and all of my research – with you right now.

Source: Contrarian Outlook