If you’re a dividend fan and you spot an 18% yield, you’re going to sit up and take notice.

Which brings me to the weird funds I’m going to show you today.

Their 18% average yield masks something shocking: they’re not only dangerous but they’re not even income investments! They’re something else entirely—and if you fail to pick up on that and buy, they could blow a hole in your retirement portfolio.

Let me explain, starting with…

Where We Found These 18% Payouts

The funds I’m talking about are called exchange-traded notes (ETNs), a close cousin of exchange-traded funds (ETFs), another asset class I recommended staying clear of in a September 12 article.

But there’s a crucial difference between ETNs and their ETF cousins: ETNs are more like a debt that issuers release that’s tied to the performance of a particular asset class.

It’s an unusual structure I’ll break down more in a moment, but the key takeaway for now is that it lets these funds use a lot of leverage, and that’s where those big dividends come from. (Yes, that’s risk No. 1 with ETNs, but stay with me, there’s more.)

There are quite a few ETNs out there paying high dividends, but I’m going to focus on three of the most popular ones today. They yield 17.6% on average:

- The UBS ETRACS 2xLeveraged Long Wells Fargo Business Development Company ETN (BDCL)

- The UBS ETRACS Monthly Pay 2xLeveraged Closed-End Fund ETN (CEFL)

- The UBS ETRACS Monthly Pay 2xLeveraged Mortgage REIT ETN (MORL)

Those are long, odd names that are all similar, so let’s unpack each one.

Each fund is issued by UBS, the Swiss investment bank that also provides a few ETFs.

And as you’d expect from their yields, all three ETNs are tied to specific asset classes investors often look to for income—business development companies (or BDCs in the case of BDCL), closed-end funds (or CEFs in the case of CEFL) and mortgage real estate investment trusts (or mREITs in the case of MORL).

ETRACS is just UBS’s brand for their ETNs, so that part doesn’t matter much. But then we get to the “2xLeveraged” bit, and yes, that means exactly what you think it does: each fund borrows a dollar for every dollar it owns and uses those two dollars together to get as much yield as it can from mREITs, CEFs or BDCs.

In other words, owning these ETNs means you’re literally doubling down on the underlying asset class. Obviously, if you’re bullish on BDCs, CEFs or mortgage REITs, buying these funds could get you a short-term pop.

The downside is that you have to pay for that leverage, since the ETNs will borrow cash to fund it. What’s more, since the Fed is raising interest rates as fast as they can, that leverage is going to get more expensive. That’s one of the risks in these ETNs, but it’s far from the biggest one.

A Hall of Mirrors

Before we get to the biggest risk ETNs pose, let’s take a quick look at how they work.

First, as they’re ETNs, not ETFs, they aren’t actually buying and selling the stocks in their indexes, which are designed to track the asset class the ETN follows. Instead, the fund manager tracks the performance of the index constituents and calculates a dividend payment as a result.

At the same time, investors bid the price of the ETN up or down during trading hours based on their estimates of how much the ETN would be worth if it did actually own the shares in its indexes.

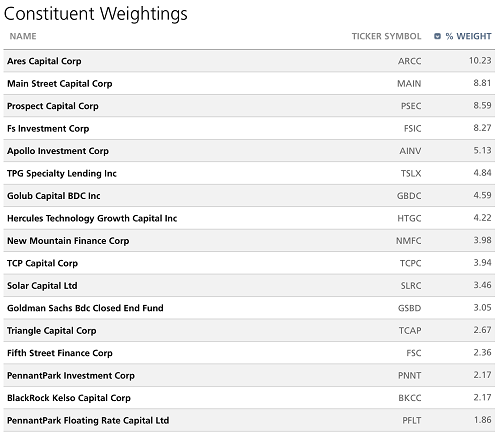

To take an example, look at the constituents in BDCL:

Note that these are just the top 17 stocks in the Wells Fargo Business Development Company Index, and BDCL doesn’t actually own any of these BDCs—rather, the fund managers are tracking the performance of these names and paying out dividends accordingly.

A lot of these are familiar names. Ares Capital Corporation (ARCC), the biggest BDC out there, makes up the largest portion of the fund’s holdings, followed by other large and top-performing BDCs.

The fund managers calculate how much income these BDCs collectively pay on a quarterly basis, then distribute that to investors. Since BDC dividends go up and down all the time—take, for instance, the solid payout hikes from Main Street Capital (MAIN) over the years versus the ever-declining dividend offered by Prospect Capital (PSEC)—BDCL’s dividend will be volatile.

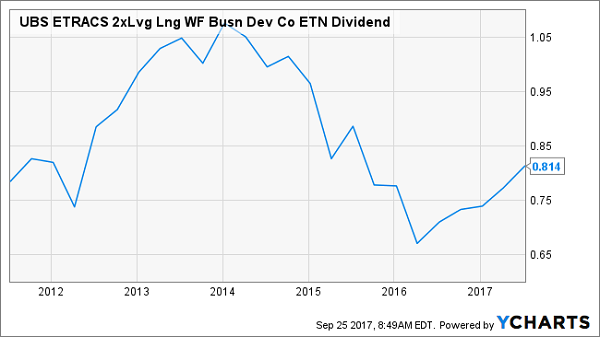

Just look at its dividend payouts since its IPO:

Don’t Bet Your Retirement on This Payout!

If this all sounds a bit abstract, it’s because ETNs are exotic derivative products—which means there’s a lot of risk. These are technically unsecured debts from UBS that don’t actually own any stocks or give shareholders a right of ownership to anything at all, so if the bank goes bankrupt, there’s a good chance these ETNs will be worthless.

Quick Wins and Brutal Losses

That doesn’t mean these funds can’t be used for a pretty big payout in the short term, however. For instance, the mortgage-REIT ETN, MORL, has clobbered the market in the past year with a 41.2% total return:

MORL Buyers Double Down—and Win

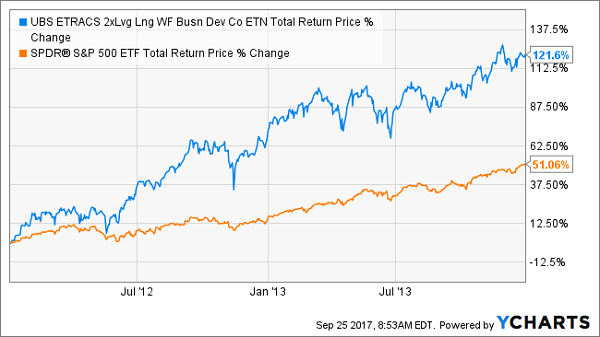

But runs like these can be short-lived. Take BDCL, which had a whopping 121.6% total return from its IPO from 2012 to the end of 2013, more than doubling SPY’s gain, even after SPY took off in 2013, one of the best years in stock-market history:

BDCL Soars …

But BDCL’s later performance shows why you can’t hold these funds forever. Since 2013, BDCL is far behind SPY in terms of total return.

…Until Now

This unveils an interesting paradox about ETNs. They were originally designed to give investors a very high stream of income—and they will do that. But that doesn’t mean they’re best for income investors. If you want a high dividend you can rely on—and you don’t want to worry about your portfolio’s payout being slashed overnight—these ETNs are not for you.

The bottom line? Buying these funds is more like speculating than investing. If you’re bullish on a particular asset class, like BDCs or mREITs, and want to make a short-term bet, they might be worth a look.

–Michael Foster

Sponsored Link: For the rest of us, let’s stay clear and build a solid income stream with 4 other, much safer funds. These 4 stout dividend plays are poised to hand us a hefty 7.4% yield and 20% upside in the next 12 months.

Here’s how.

4 “No-Brainer” Buys for Safe 7.4% Yields and Fast Gains

These 4 must-have income plays are all closed-end funds with some of the safest dividends out there.

In fact, thanks to their massive 7.4% average payout, you’ll kick-start an instant $37,000 income stream right away if you invest a $500,000 nest egg in them. That could let you to retire on dividends alone!

And unlike folks sitting on the 3 “ticking time bomb” ETNs I told you about above, you’ll sleep soundly at night knowing your income—and nest egg—are safe.

Plus there’s one other urgent thing I have to tell you: All 4 of these income titans are trading at ridiculous discounts to their net asset value.

I won’t get into the weeds on this, but here’s the upshot: if the market takes a dive, these funds’ steep discounts throw a nice floor under their share prices—and we’ll still collect 7.4% in CASH!

But I expect we’ll do far better than that: my team’s latest analysis points to massive 20%+ price upside in the next 12 months, on top of that gaudy 7.4% payout!

For a limited time, I’m going to give you exclusive access to ALL my research on these powerhouse funds with no obligation whatsoever. Simply CLICK HERE to discover their names, tickers, buy-under prices and everything you need to know before you buy.

Source: Contrarian Outlook