We’re riding a historical era of low volatility and market fluctuations.

The S&P 500 hasn’t made a 5% pullback since July 2016.

And the current low market volatility and higher valuations have been a puzzle for investors…

Political uncertainty seems high. Domestic politics haven’t been this tumultuous in decades. That’s spreading into foreign policy. Great Britain is leaving the European Union. Russia is manipulating the world via the Internet. Bitcoin is soaring and North Korea keeps firing off wobbly missiles.

We don’t think investors are complacent. We think they’re confused.

As legendary value investor Benjamin Graham explained, you can think of the market as a weighing machine in the long term… But in the short term, it’s a voting machine.

It tallies everyone’s guess about the future and spits out a price.

When investors get information that shifts their view, the market moves…

But in the “post-truth era,” information ain’t what it used to be.

For investors, the regular flow of mainstream information has become worthless…

Think about it. When Obamacare is being repealed one day, then the bill gets dropped, then it comes back in a different form, and then stalls in the Senate, what should you expect from health care stocks? When the next headlines hit the news cycle, investors won’t react because they don’t know what’s real and what’s not.

The same goes for Wall Street regulations, coal prices, and everything else that becomes an issue in the media.

All told, we don’t think the lack of volatility stems from investor complacency… We think the lack of volatility causes the complacency. There is a dearth of valuable information. And when markets don’t move, investors get complacent.

Of course, there’s a way to navigate the new era of strange, polarized, and indecipherable information…

When there’s a lot you can’t know… you must focus on what you can know.

For years now, we’ve lamented that the market was all “macro.” Breaking down businesses and snooping out value did little to contribute to earning extra profits. You were either long stocks or you weren’t. You either bought tech or made the right moves on oil… or you didn’t. Correlations between stocks soared, and momentum kept pushing everything higher.

Had you simply bought an S&P 500 index fund at the bottom of the market in 2009, you’d have earned 327% through last month, including dividends.

Now, in the post-truth era, the broader trends are harder to suss out.

While we argue that the market’s confusion has kept volatility low, stock prices have still marched up. That’s due to one simple fact…

With little else to go on, investors have focused on earnings. That’s good. Earnings are what matter. And they’ve been growing at strong levels…

In the first quarter of 2017, earnings grew 17% year-over-year. That’s the highest reading since 2010. A full 75% of companies announced earnings that matched or exceeded expectations, led by tech stocks, health care, and financials.

And the early numbers for this quarter are looking even better.

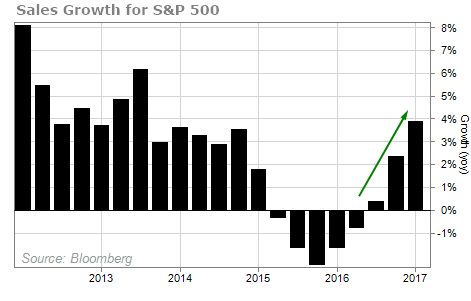

The most valuable insight from these earnings is the revenue. Over the past 12 months, revenue per share has risen 3.8%… what looks like the start of a strong upcycle in revenue growth.

This is a change from much of the past decade…

This is a change from much of the past decade…

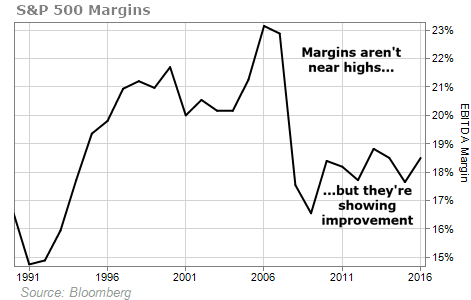

Much of the S&P 500 earnings growth in recent years hasn’t been from growing sales, but from tightening up waste to boost profit margins. But improving margins by those methods is unsustainable. We want businesses with growing sales.

Margins from earnings before interest, taxes, depreciation, and amortization (EBITDA) have risen from 16% in 2009 to 18.7% in 2016 as businesses have gotten leaner. And margins still have room to grow before they hit the highs we’ve seen in past business cycles.

That’s enough of a reason for stocks to keep grinding higher. But another one is that folks are out there buying…

That’s enough of a reason for stocks to keep grinding higher. But another one is that folks are out there buying…

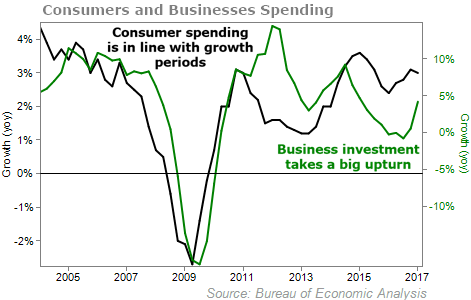

Consumer expenditures have grown 3% over last year, after inflation. That’s within the steady band of 2%-4% growth we see during strong economies.

More broadly, private fixed investments – businesses making capital investments to increase production or expand – leapt to 4.2% growth in the last quarter. That’s a big upturn and a great result for a number that’s been stubbornly low for two years.

To summarize, we’re in the “Goldilocks” part of the earnings cycle. Growth is picking up, but none of the measures look overheated.

To summarize, we’re in the “Goldilocks” part of the earnings cycle. Growth is picking up, but none of the measures look overheated.

Quality earnings will drive stocks going forward. We’re already seeing it happen. So today, we’ll be rewarded more by focusing on businesses again.

Here’s to our health, wealth, and a great retirement,

Dr. David Eifrig

[ad#stansberry-ps]

Source: Daily Wealth