I (Porter) know a headline like that will leave me with only about five people still reading. So let me try again…

The next 18 months will likely see: a terrible bear market… a substantial economic recession… and a great opportunity for you to buy high-quality businesses at reasonable prices – but only if you raise cash now.

[ad#Google Adsense 336×280-IA]Don’t believe me? Let me explain…

Seriously… I think we’re approaching another critical nexus…

One of two things is about to happen.

Either a significant restructuring of our tax code frees up billions and billions of capital currently stranded overseas and provides big incentives for U.S. corporations to invest heavily in America… or the credit cycle I’ve been reporting on since late 2015 is going to continue to roll over into a default cycle.

That would cause a serious bear market late this year or at some point in 2018.

I realize that saying either of these events could happen doesn’t help you much right now. But that’s why I think prudent investors should begin to hedge at least some of their portfolios to account for the possibility of either outcome.

Today, however, I simply want to show you the most important facts behind this forecast.

Two powerful economic forces are about to collide…

The first is reversion to the mean.

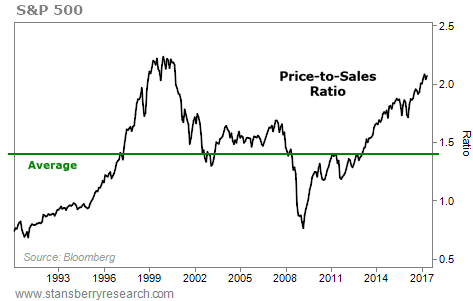

Right now, large-cap U.S. stocks (represented by the benchmark S&P 500 Index) are trading at higher levels than at any other time in history, except for during the huge tech bubble of 2000.

The chart below shows you the ratio between the market value of these companies and their annual sales. This “price-to-sales” ratio is one of the best ways to measure the real value (or lack of value) in the stock market because there are ways to inflate other measures, like book-value ratios and earnings…

One vital point to remember, however: Just because stocks are extremely expensive compared with history doesn’t mean they can’t become more expensive. I don’t advocate shorting individual stocks just because they’re expensive in terms of their ratios. Nor do I advocate shorting markets merely because they’re expensive relative to history. Valuation doesn’t equal timing.

One vital point to remember, however: Just because stocks are extremely expensive compared with history doesn’t mean they can’t become more expensive. I don’t advocate shorting individual stocks just because they’re expensive in terms of their ratios. Nor do I advocate shorting markets merely because they’re expensive relative to history. Valuation doesn’t equal timing.

On the other hand, reversion to the mean is inevitable. Every bubble will eventually find a pin.

The second economic force I want to talk about today is likely to be the pin that bursts this big stock-market bubble…

I’m talking about debt.

Everyone loves to borrow money. Few people enjoy paying it back. Many won’t.

This bull market has been powered by four important credit drivers: record levels of auto loans… record levels of student loans… record levels of corporate-bond issuance (much of it “junk”)… and an unprecedented monetization of the Federal Reserve’s balance sheet.

As I’m sure you’ll agree, these four big drivers of credit growth have now stalled. And as the credit spigot turns off and borrowers are unable to borrow more, defaults will skyrocket.

Let’s start with autos…

The average new car price (about $35,000) is the highest price ever. Compared with average wages (about $50,000), cars are vastly more expensive than ever before. So how have Americans been driving record numbers of new cars? Two ways: leases and very easy credit policies.

Since 2014, we’ve been warning that auto-lending standards were far too loose and that sooner or later, rising defaults would greatly reduce demand for new vehicles (and wreck the balance sheets of auto lenders). Were we right?

The value of auto loans that are at least 30 days in default currently totals $23 billion – up 14% in just the last year. And since 2014, the leading independent auto lender, Santander Consumer USA (SC), has seen its stock fall in half. I believe it will soon fall in half again.

The automakers themselves have been leasing a record percentage of their new-car sales (30%). That seems great until all those cars come back to the dealers. Off-lease used-car supply has doubled since 2012 and will continue to increase by another 25% over the next two years. Banking giant Morgan Stanley believes this will cause a 50% drop in used-car prices.

Remember what happened when housing prices fell?

Lots of folks who borrowed way too much money to buy their houses decided there was no point in paying the mortgage because they were “underwater” on the loan. They mailed the bank their keys and bought a cheaper house down the street.

Just remember that record percentages of new-car buyers over the last five years were subprime borrowers. Given the small down payments and the extended loan terms (up to seven years!), these buyers have never had any equity in their cars. Their cars have never been worth the loan. What do you think they’ll do with those cars? They will mail back the keys and buy a cheaper used car.

An incredible 32% of all outstanding auto asset-backed securities (ABSs) issued in 2016 were “deep subprime” – up from just 5% in 2010. I guarantee we’ll see the first-ever auto ABS default. These debt instruments are currently rated “AAA” – just like the subprime mortgage bonds were. And that’s why bad car loans will shake up the whole banking system.

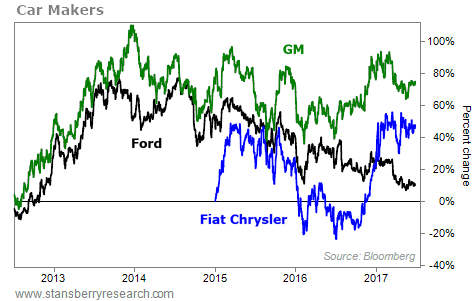

What have the automakers said about these problems so far? Ford Motor (F) was the first to even mention the problems, saying its earnings would fall 50% this year. What did its stock do? Not much… but it will…

I’m not going to waste your time with the details behind the student-loan debacle…

I’m not going to waste your time with the details behind the student-loan debacle…

Just ask yourself: Would you lend $1 trillion to a bunch of 18-year-olds?

The U.S. Department of Education makes it next to impossible to calculate an accurate default rate, but Bloomberg has sifted through the data to get a reliable picture – and it’s horrifying…

Some 41.5 million Americans collectively owe nearly $1.3 trillion on their federal student loans… About one in every four borrowers is either delinquent or in default. Total indebtedness has doubled since 2009.

Navient (NAVI) handles most of the loan servicing on behalf of the Department of Education. It has also invested several hundred million dollars in packages of student loans. And it’s currently being sued by the government for trying to collect on student loans. Go figure.

Its stock is down by roughly half since its peak in 2015. Think it can fall in half again? Or do you think it’s more likely that college students suddenly become financially responsible?

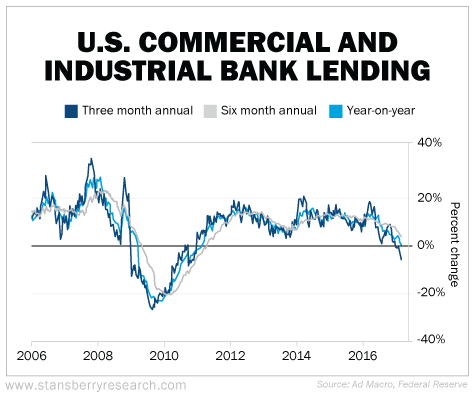

In regards to corporate lending, we’ve seen banks begin to reduce outstanding corporate lending for the first time since 2008…

We also track corporate-default rates and corporate-debt downgrades in our trading service, Stansberry’s Big Trade.

We also track corporate-default rates and corporate-debt downgrades in our trading service, Stansberry’s Big Trade.

So far this year, Standard & Poor’s has downgraded 465 U.S. companies. We’re on pace to see around 900 downgrades this year. That would fall short of last year’s total, but it would be more than each of the years from 2010 to 2015.

The high-yield “junk” bond default rate reached 5% in 2016. It now stands at 4.5%. But the credit cycle has certainly rolled over. Defaults and downgrades are continuing to rise.

Finally, and perhaps most important…

The Federal Reserve says it will now begin to “unwind” the $4 trillion credit stimulus it has been providing the market. That’s like taking 25% of GDP out of the credit market. I’m fairly confident that won’t be good for interest rates, default rates, or the stock market.

The “Trump Trade” – the big rally we’ve seen since the presidential election – has investors feeling confident, even euphoric. I’d certainly admit that if Trump can push through significant tax reform, it’s possible this default cycle could be cut short.

Especially important are Trump’s efforts to flatten the progressive nature of the tax code through a border adjustment tax (which would allow for the top marginal rate on income taxes to fall to around 30% and would allow for taxes on capital gains and dividends to fall to around 20%).

Trump’s effort to change the rules on corporate taxation and depreciation schedules is also crucial. Allowing companies to expense all capital investments in full would create a significant boom in corporate spending.

But – barring some significant restructuring of the U.S. economy – you should be looking to hedge your portfolio going into the second half of 2017.

The credit problems aren’t going away. They’re going to get worse. It’s only a matter of time before they upend the stock market.

Regards,

Porter Stansberry

[ad#stansberry-ps]

Source: Daily Wealth