Since March, my Wealthy Retirement contributions have mainly focused on options trading. And while the response from readers has been fantastic, I’ve decided to step away from options for a couple of weeks…

(If you missed any of my articles, you can check out the archives here.)

That’s because I want to share one of the most lucrative income opportunities I have been focusing on. It’s not glamorous by any means, but it’s steady and dynamic.

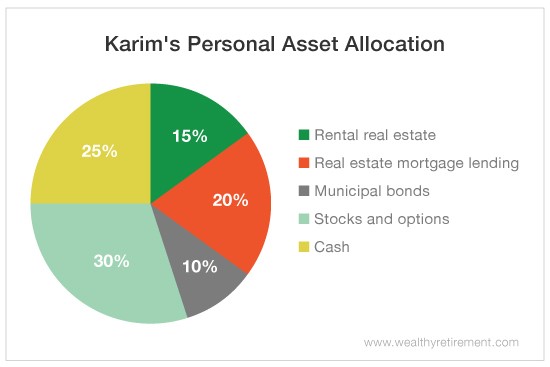

I like to diversify. My current overall investment portfolio looks like this…

Just yesterday, I closed on another mortgage. This is not a mortgage for me, however. In this case, I am the lender.

Just yesterday, I closed on another mortgage. This is not a mortgage for me, however. In this case, I am the lender.

If you have never been the lender on a mortgage, it’s a very different experience from being a buyer or a seller. When you’re the moneyman, everyone is nervous… except for you. If you don’t show up, the deal falls through.

[ad#Google Adsense 336×280-IA]While any type of lending can be risky, there are ways to mitigate risk.

And when I put together a mortgage, I pay close attention to every detail.

The first thing you want is a very, very competent attorney.

You can expect about $1,200 of each deal to go toward attorney fees.

I have the buyer pay for the fees.

I want to pay only the mortgage amount out of pocket – nothing else.

And when you’re the lender, it’s a pretty easy position to negotiate from.

The borrowers I look for are people who are in business for themselves. They have great credit scores and ample cash for down payments. That said, they can still have difficulty getting loans because they are self-employed.

Often, the application process takes too long, and some sellers just aren’t willing to wait – especially in neighborhoods where getting buyers is not an issue. On the other side, lenders have an aversion to lending to those who are self-employed because, well frankly, many fudge their returns. Not the majority, mind you, but enough to cause angst.

For me, it’s important that I either know the person or they have ironclad references. Tax returns for at least three years from the IRS must be provided. They can be requested for $57 per return for at least the past six years.

I lend only in neighborhoods that I know intimately. This is one of the most important factors when it comes to real estate lending. The neighborhood has to be excellent in terms of surrounding homes, maintenance, tax base and – most importantly – school district.

The last family that I held a mortgage for would have spent close to $200,000 for private schools if they hadn’t bought in a neighborhood with the best-rated public schools. They made a smart financial decision and will probably make money on their house as well!

Outside of a strong attorney, qualified borrower and great neighborhood, I aim for returns that are at least 50% above those from a conventional 30-year mortgage. My latest deal was for an adjustable-rate mortgage starting at The Wall Street Journal’s prime rate, plus 2%. It adjusts every year but can never fall below the original rate.

The buyer must put at least 20% down, pay all closing costs and recording fees, and must have at least another 10% of the purchase price in cash or liquid assets after closing. And he or she must also sign a personal guaranty.

The purchase price also must come in below appraisal.

You may be thinking that I look for too much from a borrower.

Guess what? I want to make sure that my money is safe. So I can ask for anything I want – even more than a conventional lender. If the borrower doesn’t like the terms, he or she can walk.

The mortgage itself has a five-year term with a balloon payment due after five years. A balloon mortgage requires that interest and principal be paid monthly according to an amortization schedule. The remaining principal must be paid in full at the end of the balloon period (in this case, five years). At that time, the borrower can apply for a mortgage or refinance to pay you off – or you can extend the terms.

I personally inspect the house and will do it only if I know that I can resell, rerent or move into the home myself in the event that I have to foreclose. Obviously, I can’t move into every home if they all foreclose at the same time. That’s why the ability to rerent is critical.

In the long run, this is another steady source of income for cash that I just have sitting around. Worst case, I add another rental property to my portfolio.

Of course, crashes do happen, and that is always a risk. But if you pick the right house and borrower, in the right neighborhood, that risk can be mitigated.

And just like any investment, you should never invest money that you are going to need tomorrow.

Good investing,

Karim

[ad#agora]

Source: Wealthy Retirement