The ideal “no withdrawal” retirement portfolio is a diversified one. Since you’re reading this, I know you know stocks. But how comfortable are you buying bonds – especially the more obscure issues (which provide the best yields and value?)

Probably not as comfortable as you are with good ol’ dividend paying stocks. But here’s the good news – it doesn’t matter.

[ad#Google Adsense 336×280-IA]You can diversify your portfolio, bank safe 9% yields and hire one of the best bond managers on the planet.

For free, to boot! It just requires a bit of contrarian thinking – and knowing which publicly traded funds these guys are managing behind the scenes.

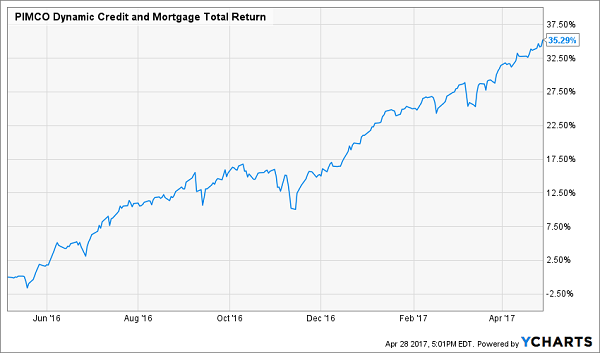

Pick the right fund, and you can actually enjoy total returns up to 35% per year.

Here’s how.

Hire the Bond King’s Heir for Free

You probably know the “Bond King” Bill Gross. How about his successor, Dan Ivascyn?

When Gross left PIMCO, a tide of cash followed him out the door. But the flow of money quickly subsided when Ivascyn stepped to the plate and outperformed Gross himself. No wonder PIMCO let the King walk out the door – they had their next superstar in waiting!

A money manager of Ivascyn’s caliber will usually cost 2% annually (plus 20% of profits). And it’d take a million bucks or two to get his attention.

But as recently as a few months ago, you could have hired him for free. And this time last year, you’d have been paid to give him your money!

Plus, you could have done it all with one-click from your computer (or tap from your phone) by purchasing PIMCO’s Dynamic Credit and Mortgage Total Return Fund (PCI).

PCI charges a 2% management fee. But it’s easy to get the fee comped – if you simply buy the fund when it trades for a discount.

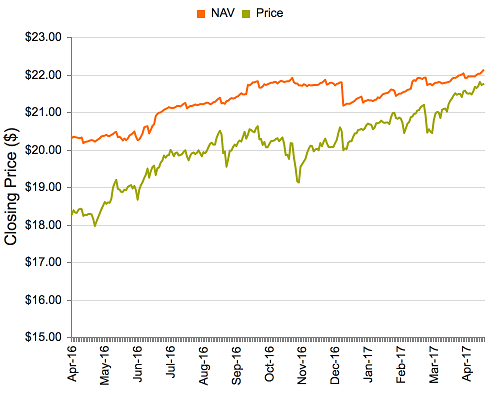

Since PCI is a closed-end fund (CEF), it has a fixed pool of shares (versus a mutual fund, which can simply issue more shares anytime it wants). The restricted supply means the fund’s price trades like a stock – which means it can stray from its net asset value (NAV).

For top-notch managers like Ivascyn, the fund’s price usually wanders above its NAV. Investors are willing to pay more than $1 for a dollar in assets just to get in:

Big PIMCO Premiums Today

But I always demand a discount. A 2% discount means our management fee is comped. A bigger bargain means we have some upside (as the discount window closes) and our yield is higher than it would be if the fund traded for fair value (because income is earned per NAV unit – so the less we pay for it, the better).

But I always demand a discount. A 2% discount means our management fee is comped. A bigger bargain means we have some upside (as the discount window closes) and our yield is higher than it would be if the fund traded for fair value (because income is earned per NAV unit – so the less we pay for it, the better).

The three funds above are trading at big premiums however. Is it possible to ever get Ivascyn’s expertise at a discount? You bet.

First-Level Worries to the Rescue

PCI had been neglected by investors because of its strategy focused on mortgage-backed securities (MBSs), which had the lead role in the last financial crisis. They have recently been immortalized in the book and movie The Big Short. MBSs blew up the financial system in 2008 and have been outcasts ever since.

But a “second-level” look at mortgage payments showed these assets have successfully completed financial rehab. They quietly began to enjoy the benefits of clean living – with mortgage defaults and delinquencies trending down. Ivascyn and his team capitalized on this misplaced despair.

Twelve months ago, we added PCI to our Contrarian Income Report portfolio. The fund traded at a 10% discount to its NAV and yielded an incredible 10.7%. This “free lunch” was gradually gobbled up:

PCI’s Discount Window Closes…

And anyone who bought PCI benefited handsomely:

And anyone who bought PCI benefited handsomely:

Ivascyn Worth Every Penny: 35% Net of Fees!

PCI still trades for a 1.7% discount today, which means we can still get most of Ivascyn’s well deserved fees comped. But I want it all for free – and I want upside to boot.

PCI still trades for a 1.7% discount today, which means we can still get most of Ivascyn’s well deserved fees comped. But I want it all for free – and I want upside to boot.

— Brett Owens

Sponsored Link: Too much to ask? Not at the moment. My favorite fixed-income play today is positioned for secure 15%+ total returns in the year ahead. We’ll get 9% in dividends alone, with a bond manager every bit as smart as Ivascyn working for us for free.

It’s one of three “slam dunk” income plays in the No Withdrawal Portfolio I mentioned earlier. If secure 8%+ yields with 10% to 15% upside to boot is appealing to you, then you’ll love my top three CEF recommendations. I also have some recession-proof REITs and easy-to-buy “preferred” shares to share as well. Click here and I’ll explain the details, tickers and full analysis on these underappreciated (and for now, under owned) 8% payers.

Source: Contrarian Outlook