I wouldn’t buy any old dividend payer right now, with most stock prices on the high side. But, believe it or not, there are a few quality dividend growers that are still pretty cheap.

[ad#Google Adsense 336×280-IA]This time last year, we discussed four fast dividend growers selling below book value.

It’s almost hard to believe now that the four-pack of banks we highlighted then were selling for as cheap as 70 cents on the dollar.

But that’s how you make money with stocks – by buying good names when nobody else wants them.

And since my column last April, this group gained an average of 53%:

Easy Contrarian Gains Averaging 53%!

Book value was an accurate valuation metric for these banks because most of their assets and liabilities are marked to market. It’s often thought of as the bank’s liquidation value. When you buy a bank for book value, it means you’re getting its underlying assets for fair value with the actual businesses tossed in for free. This is the closest thing to a free lunch we’ll ever see on Wall Street.

But these free lunches have been served, with these banks now all selling above book. Which means we’ll have to look elsewhere for our next contrarian meal.

5 Dividend Growers at “Free Lunch” Prices Today

There aren’t many firms growing their payout meaningfully every year and selling below book today. Metlife (MET) is the cheapest big name on the board, trading for us 85% of book.

Insurers are like banks – when you see them trading below book, you should immediately ask yourself: “Why?” And if you can then debunk the headline concerns, you should then buy.

In recent years, insurance stocks had fallen out of favor, with low interest rates to blame. Reason being, insurance firms typically invest their float – the premiums they collect – into safe interest-bearing securities for additional income. Low rates bring low insurance profits.

Many insurers rallied along with rates beginning last August, but Metlife has lagged. MET is getting set to spin off its US retail business, while at the same time arguing for the removal of its designation as a “systemically important financial institution,” and the costly regulatory burdens that come with it. The spinoff and/or progress on the SIFI front may spark the stock to catch up with its peers – and its dividend, which is up 45% in the last four years.

Meanwhile reinsurer Everest Re (RE) has rallied above its liquidation value, but it still trades for just seven times free cash flow (FCF). That’s “easy money” for management, which loves to repurchase shares when they are too cheap. Over the last five years, they’ve bought back nearly one-quarter of the company while boosting their payout by 160%:

Higher Dividend + Lower Share Count = Higher Prices

Prudential (PRU) has been a dedicated regular on my “too cheap” list. Last May I said it had 25% upside, and that proved conservative – the stock has rallied 34% in just 11 months!

“Pru” now trades for book, but just 3.2 times FCF. The company is still atoning for its 2013 dividend cut in investors’ eyes, but management has repented since then by boosting its payout by 88% over this time period while reducing shares outstanding by 8%. The firm’s focus on retirement solutions should serve it well in the years ahead, with 10,000 baby boomers hanging it up every day. Shares pay 2.8% today.

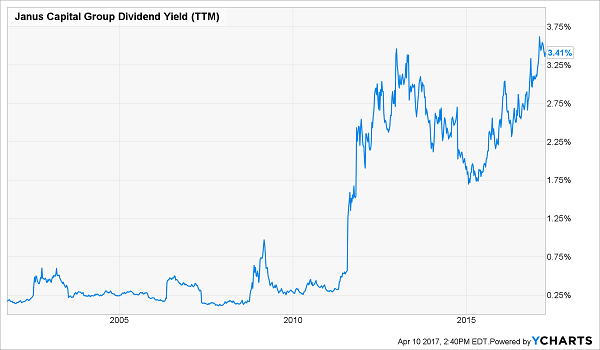

Bill Gross’ new home hasn’t been hospitable to shareholders after the stock’s initial “Bond King pop.” Janus Capital (JNS) sits lower today than it did when the legendary bond strategist joined the firm.

But Janus has increased its dividend by 38% during Gross’ reign, and it’s due for another hike. Shares pay 3.4% today, their highest mark ever. As I’ve said before, while buying stocks at all-time highs can be scary, buying yields at all-time highs is often a simple yet effective market timing strategy:

Janus Capital Has Never Paid More

We’ll close with a small bargain name boasting big dividend growth – Federal Agriculture (AGM) aka “Farmer Mac.” If there’s one thing I love more than payout hikes, it’s dividends that actually accelerate higher. When this happens, the attached stock price often has trouble keeping pace – and that’s exactly what’s happening with Farmer Mac’s price and payout:

Struggling to “Catch Up” With the Dividend

“Farmer Mac” buys and guarantees farm loans. It was hit hard in 2008, but business is booming today. Investors, however, continue to suffer post-traumatic stress about this name – which is why shares trade for less than three times annual FCF.

— Brett Owens

And 3 Slam Dunk “Free Lunches” That Yield 8%![sponsor]

Closed-end funds (CEFs) are great vehicles for bargain buys because they often trade at discounts to their net asset value (NAV). Since their assets must be constantly “marked to market” – or fairly priced according to how much they’d fetch today – NAV is a real-time look at a fund’s liquidation (and really, book) value.

The CEFs in my “No Withdrawal” Retirement Portfolio yield an average 8%. This means if you have a million dollars invested in these nine positions, you’re earning $80,000 annually in dividends alone – without having to sell any principal.

Compare that salary with your friends who instead invest in “safe” Treasuries. At 2.4% on the 10-Year, your nest egg is generating more than three times as much income as theirs!

Plus we can further improve on this “No Withdrawal” strategy by buying stocks and funds when they are out-of-favor. Not only do we secure outsized yields when we purchase with a contrarian mindset, but we can also enjoy upside as prices normalize and discount windows close.

What discount windows are likely to close next? The widest open ones, of course.

My three favorite CEFs to buy today trade at 10% to 15% discounts to their net asset value (NAV) today. That’s easy price upside, which could be realized in a matter of months. And these funds already yield 8% annually!

Add up these big dividends and price upside, and we’re probably going to be patting ourselves on the back next April congratulating ourselves on our 23% to 33% “free lunch” gains.

Don’t read this column in a year with regret! Cash in these 8% meal tickets now. Click here and I’ll share my full analysis along with fund names, tickers and buy prices.

Source: Contrarian Outlook