Master limited partnerships (MLPs) are among the most frustrating sources of yield out there. Yes, it’s common for MLPs to yield in the high single digits and even low double digits, and yes, they enjoy a number of tax benefits. But they also come with a ton of tax hassles, including dealing with K-1s for every one in your portfolio – unless, of course, you invest in one of the three high-yielding MLP funds I’m about to show you.

A quick refresher on the sector…

MLPs must derive a minimum of 90% of cash flows from commodities, natural resources or real estate, which is why most of the MLPs you see out there are related to energy pipelines and storage.

[ad#Google Adsense 336×280-IA]They enjoy certain tax advantages as long as they pay most of their earnings out as distributions to shareholders, so they typically throw off extremely juicy yields.

Better still, most of those distributions are taxed as return of capital.

That means they’re subtracted from your cost basis, and you’re only taxed only when you sell.

If you can get your cost basis down to zero, you get taxed at much more favorable long-term capital gains rates!

And then … there’s the catch.

Note that I said most of the distributions are taxed as ROC. However, about 10% to 20% is taxable income. This, and other MLP tax complications, ultimately falls to you. You have to deal with Schedule K-1 tax forms, which is an inconvenience so big that Vanguard calls it out in its “User’s guide to master limited partnerships”:

“The direct method of investing in MLPs — buying partnership units — involves the receipt of Schedule K-1 tax forms, which some may find too complicated. … Given the risks and complications, MLPs may not make sense for most investors.”

But there’s a better way – you can actually avoid the tax nonsense without foregoing MLPs altogether. How? Let’s discuss three MLP exchange-traded notes that gives us yield hunters exactly what we want: the ability to buy into high-yield master limited partnerships without the headache come tax season.

JPMorgan Alerian MLP Index ETN (AMJ)

Yield: 5.7%

Expenses: 0.85%

The JPMorgan Alerian MLP Index ETN (AMJ) is the most popular exchange-traded note that invests in MLPs, and it tracks the exact same index used by the well-known Alerian MLP ETF (AMLP).

So, why an ETN?

An exchange-traded note doesn’t actually hold any stocks, bonds … anything. Instead, it’s simply bank debt that is wrapped up as an exchange-traded product, and rather than just paying back interest, it pays back (minus fees) the return of the index it’s designed to track. In the case of the AMJ, then, it produces the return of both the Alerian MLP ETF index, and the “distributions” it’s supposed to pay out.

There are some downsides to this, of course. For one, you don’t get the favorable tax treatment of MLPs, and because ETNs are debt, there is the possibility (however small) that if the underlying issuer’s credit is hammered, it will negatively affect the returns of the ETN.

On the upside, ETNs track their indices far more closely than their ETF counterparts, and taxation couldn’t be simpler: ETN distributions are taxed at individual income rates. If you sell the ETN, you’re taxed at capital gains rates, just like a stock.

As far as the AMJ itself is concerned, then, you’re getting the returns and distributions of an index of more than 40 energy-focused master limited partnerships. It’s a pretty top-heavy index that includes Enterprise Products Partners LP (EPD) at nearly 19% of the fund, and Energy Transfer Partners LP (ETP) and Magellan Midstream Partners LP (MMP) at roughly 9% weights each.

The result is a simple, easy-to-understand way to trade MLPs that has significantly outdone its ETF counterpart over the long haul.

JPMorgan’s AMJ: An Ideal Way to Buy MLPs’ Big Yields

ETRACS Alerian MLP Index ETN (AMU)

ETRACS Alerian MLP Index ETN (AMU)

Yield: 5.8%

Expenses: 0.80%

The ETRACS Alerian MLP ETN (AMU) is another exchange-traded note that will look awfully familiar at a close glance – because it tracks the exact same index as AMJ. The companies are the same. The weights are the same.

The devil is in the details.

The most straightforward advantage is the lower cost. Yes, at 0.8%, AMU is just 5 basis points cheaper than AMJ, but remember: a few basis points can add up to hundreds and even thousands of dollars of extra return over time!

Also, ETNs do have an expiration date. Right now, the AMJ is set to expire in 2024, while the AMU won’t expire until 2042. That could make a difference to investors who are thinking very long-term – say, estate planning.

Lastly is a little something for the wonks: ETFs and ETNs create and redeem shares as investors buy and sell, which keeps the price on par with their underlying assets. AMJ stopped doing this in 2012, and as a result, AMJ can actually trade at premiums and discounts to its NAV. That means, depending on whether you’re buying when AMJ trades at a premium, you can actually get a better deal by buying into AMU.

ETRACS’ AMU: A Smart Pick for Super-Long-Term Investors

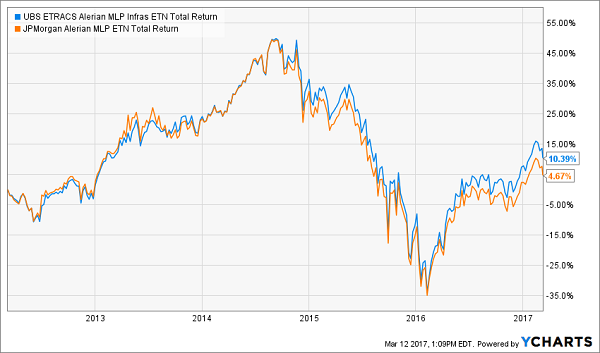

ETRACS Alerian MLP Infrastructure Index ETN (MLPI)

ETRACS Alerian MLP Infrastructure Index ETN (MLPI)

Yield: 6%

Expenses: 0.85%

The MLPI is another exchange-traded note that gives investors a little more specific exposure to the MLP space, and also a little higher yield.

Whereas the AMJ tracks the broader Alerian MLP Index, the MLPI instead invests in a 22-holding subset that focuses exclusively on midstream MLPs. In other words, these are companies involved with transportation (pipelines) and storage. That knocks out AMJ “holdings” such as AmeriGas Partners LP (APU) and Suburban Propane Partners LP (SPH).

Still, many of the top holdings are the same, with Magellan tops at 10.5%, Enterprise Products Partners at “only” 10% of the fund, and Energy Transfer Partners at 9.8%.

On top of that, MLPI isn’t simply market cap-weighted – it’s float-adjusted (excludes shares held by insiders, for instance) and also capped at several tiers.

The narrower construction of MLPI has resulted in slightly better performance over AMJ across every major time frame since inception in 2010, and a bit more padding on the yield at current prices.

ETRACS’ MLPI Specializes in Squeezing More Out of MLPs

— Brett Owens

The Retirement Portfolio You NEVER Have to Touch! [sponsor]

When it comes to MLPs, though, it feels like you’re always sacrificing something. Do you want the most tax-efficient yield possible? Here’s a stack of forms. You want something nice and easy? Sorry, but you’ll have to pay.

That’s why your money is far better off in the 8%-plus winners I’ve featured in my “No Withdrawal” retirement portfolio.

The problem with most retirement picks is that they’re designed to merely get you to retirement. So you build up your nest egg, say goodbye to the workplace … and then what? Even if you hoard away dividend-paying blue chips, they’re probably yielding 3%, 4% tops. That means even if you have a million-dollar nest egg, you’re only raking in $30,000 or $40,000 a year. That’s not much, and you could quickly find yourself clawing away at the nest egg to make ends meet.

Do not settle for that kind of retirement!

My “No Withdrawal” retirement portfolio is a set of picks that generate 6%, 7%, 8% and even higher so you can live off dividend income alone and never touch your nest egg. In fact, this portfolio is designed to even grow your nest egg thanks to a few holdings that offer 7% to 15% upside!

What makes this portfolio so effective is that it picks and chooses from all corners of the market. Preferred stocks, REITs, closed-end funds … this set of high-yield stock picks selects from the best holdings across the high-yield spectrum.

Don’t spend your retirement calculating and recalculating how many years your nest egg has left, leaving you with nothing but your Social Security check. Instead, collect regular dividend checks that will pay the bills, finance your vacations and even let you spoil your family.

Let me show you the way to a no-worry retirement! Click here and I’ll provide you with THREE special reports that show you the path to building a “No Withdrawal” portfolio. You’ll get the names, tickers, buy prices and full analysis of their wealth-building potential – and it’s absolutely FREE!

Source: Contrarian Outlook