Investment Thesis

j2 Global (JCOM) was founded in 1995 and went public in 1999. During their first few years as a public company, j2 Global generated operating losses; however, since 2002 the company has strung together an impressive record of rapid growth.

They initiated their first dividend in 2011, and on February 9, 2017 they increased their dividend to 2.8%, which remarkably marked their 22nd successive quarterly dividend increase.

[ad#Google Adsense 336×280-IA]Although the company only offers a current yield of 1.8%, it has grown its dividend at a compound average growth rate of 27.1% since they initiated one in 2011.

Importantly, j2 Global is currently available at a sound valuation relative to its expected future earnings growth of 16% on average over the next 2 years.

Consistent with their long-term track record, j2 Global reported better-than-expected earnings per share in the 4th quarter of 2016.

Consequently, I offer this research candidate for those investors interested in earning an above-average total return through a combination of capital appreciation and a growing dividend.

Thesis for Continued Growth

j2 Global offers Internet services worldwide and operates through 2 segments, Business Cloud Services and Digital Media. However, the company has historically generated growth through mergers and acquisitions. The company completed 22 acquisitions in 2016, and 6 acquisitions in the 4th quarter alone. This included Everyday Health, Inc. their largest acquisition to date by subsidiary Ziff-Davis LLC.

Importantly, this definitive business strategy implies that an investment in j2 Global today is likely to be an entirely different investment in the future. On the other hand, it is through these acquisitions where future growth might come from. The following taken from j2 Global’s website summarizes the company’s merger and acquisition business strategy:

“M & A

Core to j2’s business strategy is the acquisition of assets, companies, and intellectual property. Our M&A efforts are global and focus on Cloud Services especially in the following areas: (i) online data backup; (ii) voice services; (iii) email and email marketing; and (iv) internet based fax solutions. In addition, we also look for additional web properties in the Digital Publishing space focusing on technology and gaming.

j2 strongly believes in its ability to leverage its core strengths – successful distribution of Cloud Services on a cost effective basis, a disciplined approach to managing costs, successful integrations of companies and a data centric approach to running companies as well as access capital for transactions up to $1 billion in valuation. To date, j2 has acquired more than 40 companies/business activities around the world, providing a well-received and quickly executed “exit” path to the acquired entities’ owners. In addition, in many cases, it provides an opportunity for the acquired companies’ owners and employees to be a part of a bigger endeavor.”

For further insight into the company and its operations to include its future growth potential, I offer the following short business description courtesy of S&P Capital IQ:

“j2 Global, Inc. engages in the provision of Internet services worldwide. It operates through two segments, Business Cloud Services and Digital Media.

The Business Cloud Services segment offers cloud services to sole proprietors, small to medium-sized businesses and enterprises, and government organizations, as well as licenses its intellectual property rights to third parties.

This segment provides online fax services under the eFax and MyFax names; on-demand voice and unified communications services under the eVoice and Onebox names; online backup solutions under the KeepItSafe, LiveDrive, and LiveVault names; hosted email security, email encryption, and email archival services under the FuseMail name; email marketing service under the Campaigner name; and cloud-based CRM solutions under the CampaignerCRM name.

The Digital Media segment operates a portfolio of Web properties, including PCMag.com, IGN.com, Speedtest.net, AskMen.com, and TechBargains.com that offers technology products, gaming and men’s lifestyle products and services, news and commentary related products and services, speed testing for Internet and network connections, and online deals and discounts for consumers, as well as professional networking tools, targeted emails, and white papers for IT professionals.

This segment also sells display and video advertising on its owned-and-operated Web properties and third party sites, as well as targeted advertising across the Internet through various networks; sells business-to-business leads for IT vendors; promotes deals and discounts on its Web properties for consumers; and licenses the right to use PCMag’s Editors’ Choice logo and other copyrighted editorial content to businesses.

The company was formerly known as j2 Global Communications, Inc. and changed its name to j2 Global, Inc. in December 2011. j2 Global, Inc. was founded in 1995 and is headquartered in Los Angeles, California.”

Investing Principles

It is often said that the best things in life come in small packages. However, as it relates to investing in common stocks, it seems to be widely held that bigger is better. But, if a high total return is your objective, you might want to consider that the bigger a company gets, the harder it is for it to grow fast. This is important, because if you invest in a stock at a reasonable valuation, your ultimate long-term returns will be a function of how fast the company grows.

Consequently, size matters if you’re looking for long-term above-average growth. In this regard, j2 Global with a market cap just under $4 billion has plenty of room to continue to grow. Although it could be argued that there is greater safety in larger companies, safety often comes with a price. When investing in common stocks, that price typically comes at the expense of a lower future total potential return.

On the other hand, j2 Global’s small size might partially explain why it is under followed and often overlooked in spite of its incredible long-term track record of earnings growth and more recently dividend growth. As the title of this article indicates, it might be a mistake to overlook this attractive growing business just because of its smaller size.

So yes, I will acknowledge that there might be a little more risk investing in a company like j2 Global in contrast to investing in its larger peers such as Microsoft (MSFT) or Oracle (ORCL). However, it can also be argued that the future growth potential of these larger companies is behind them, whereas much of j2 Global’s future growth may possibly be still ahead of them.

j2 Global a Fundamental Snapshot Analysis

Now that I discussed what j2 Global does and how it grows, it is time to take a deeper look into the company’s fundamentals, its long-term growth history and most importantly, j2 Global’s potential for future growth. Let’s start by looking at their historical accomplishments.

As an investor, I tend to admire companies that have strung together a consistent record of earnings and cash flow growth. I believe this provides insights into the attractiveness of the company’s business as well as the competency of its management team. Consistent long-term above-average growth is rarely an accident.

Although history does not guarantee the future, I would rather commit to a company with a great track record over a company with weak or sporadic historical results. j2 Global has put together a very impressive record of historical growth and operating excellence.

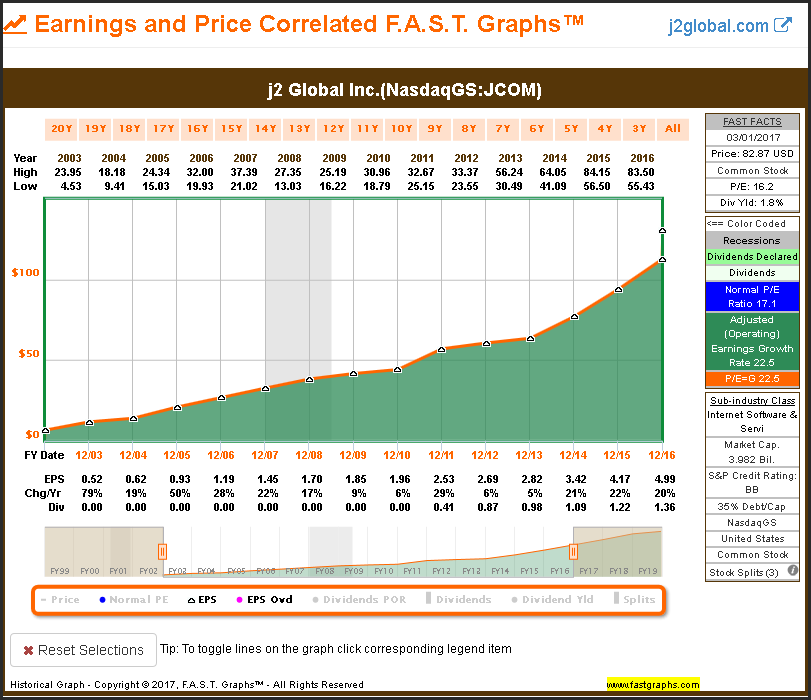

The following F.A.S.T. Graphs™ plots j2 Global’s historical adjusted operating results over the timeframe 12/31/2002 through 12/31/2016. Adjusted operating earnings have grown at a compound annual rate of 22.5% per annum. There are two important aspects of this excellent track record of growth that should be noted. Number one, the incredible reliability and consistency of year-over-year adjusted operating earnings growth has been close to impeccable. Second, there are no forecasts included; this is the actual historical record.

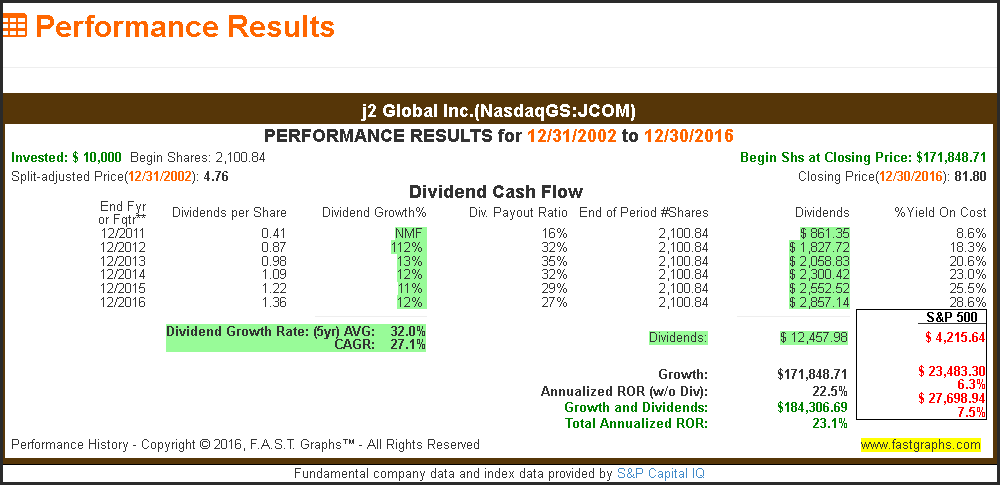

When looking at the company’s performance to shareholders over the above timeframe, it is not a coincidence nor is it an accident that capital appreciation of 22.5% equates to the company’s earnings growth rate achievement. Furthermore (and not shown on the above graph) is the addition of more than $12,000 in dividend income from a one-time initial $10,000 investment.

When looking at the company’s performance to shareholders over the above timeframe, it is not a coincidence nor is it an accident that capital appreciation of 22.5% equates to the company’s earnings growth rate achievement. Furthermore (and not shown on the above graph) is the addition of more than $12,000 in dividend income from a one-time initial $10,000 investment.

Personally, I prefer evaluating a stock based on non-GAAP adjusted earnings and/or cash flows. The reason I prefer adjusted earnings is because I feel they more practically reflect how the business is performing on an operating business.

Personally, I prefer evaluating a stock based on non-GAAP adjusted earnings and/or cash flows. The reason I prefer adjusted earnings is because I feel they more practically reflect how the business is performing on an operating business.

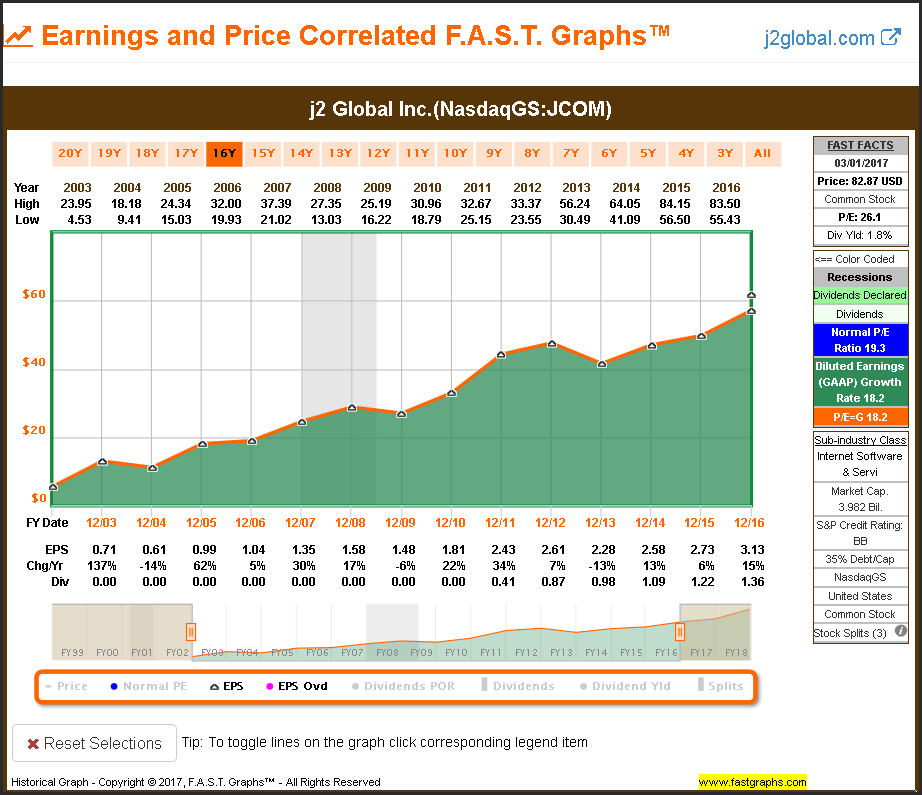

This is in contrast to GAAP (diluted) earnings which may include significant one-time accounting events and/or non-cash charges. However, for the GAAP earnings purists out there, j2 Global’s historical diluted earnings record is also quite impressive. This is especially true when you consider that this company engages in significant merger and acquisition activity.

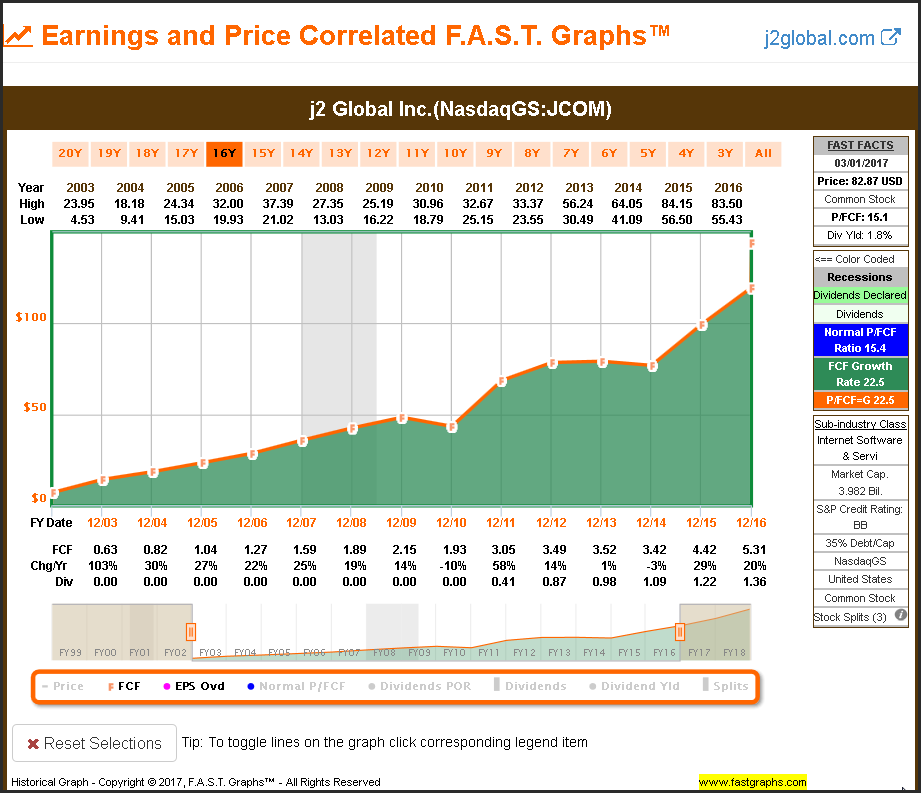

Additionally, an examination of a company’s record of free cash flow generation can also be quite revealing. This is the measure of the company’s financial performance calculated as operating cash flow minus capital expenditures. In other words, this is the cash flow left over after the company has spent the necessary money required to maintain or expand its business. j2 Global’s historical record of generating free cash flow is also quite impressive.

Additionally, an examination of a company’s record of free cash flow generation can also be quite revealing. This is the measure of the company’s financial performance calculated as operating cash flow minus capital expenditures. In other words, this is the cash flow left over after the company has spent the necessary money required to maintain or expand its business. j2 Global’s historical record of generating free cash flow is also quite impressive.

F.A.S.T. Graphs Video: Offering A More Comprehensive Look At j2 Global’s Fundamentals and Dividend Paying Capacity

F.A.S.T. Graphs Video: Offering A More Comprehensive Look At j2 Global’s Fundamentals and Dividend Paying Capacity

Summary and Conclusions

I believe that investors should make investment choices that meet their specific objectives. Moreover, once made, I believe those investment choices should be judged based on meeting the objective they were chosen for. For example, if the investor was desirous of achieving the highest current yield available, they should also recognize that this might limit their capital appreciation potential.

It is very rare to find investments that offer both high-yield and high-capital appreciation potential. But perhaps more importantly, on the rare occasions where both might be present, the risk is typically also higher.

Consequently, for the investor seeking high yield, it only makes sense to me that their focus should be on the income that the investment is throwing off. Capital appreciation, if any, should be considered a side effect or bonus under those conditions. In other words, I believe it’s important, and only makes sense to be realistic with your expectations.

The reason I bring this up is because my personal investment quest currently is looking for fairly valued dividend growth stocks with yields exceeding 3%. Unfortunately, I have been very frustrated in identifying many large blue-chip dividend stocks that meet my quality standards and valuation requirements in today’s low interest rate environment.

As a result, I’ve been forced to look beyond the normal channels of Dividend Aristocrats, Champions or Contenders. Unfortunately, expanding my universe has continued to provide few investment opportunities under that criteria. On the other hand, and perhaps more fortunately, it has opened my eyes to other currently attractive investment opportunities such as j2 Global.

When I came across j2 Global as I searched for high quality dividend growth stocks, I could not help but be impressed by what I saw. Therefore, I thought it was also worthy of sharing this moderately yielding but high total return potential research candidate with my regular readers. Therefore, if your investment objective is high total return with a growing dividend kicker, then j2 Global might just be what the doctor ordered.

— Chuck Carnevale

[ad#wyatt-income]

Source: FAST Graphs