The “Dogs of the Dow” are back. And this year, the biggest dogs are not just generous yielders – they’re cash cows with price upside to boot.

For the uninitiated, the Dogs of the Dow strategy is simply buying the 10 Dow Jones stocks with the highest yields, typically at the beginning of a given year.

[ad#Google Adsense 336×280-IA]The basic premise is that, when it comes to blue-chip stocks, high relative yields are the best sign of value. They simply highlight firms at the weakest part of their business cycles.

Blue chip names are rarely cheap, which is why we only want to buy them when their businesses are in the tank.

As sales and profits recover (as they almost-always do), we enjoy outsized price gains along with our dividends.

Since 2000, the Dogs of the Dow have returned an average of 7.9% as a group.

That beats both the 5.8% return of the S&P 500, and even the 6.3% average return of the Dow Jones Industrial Average itself.

The strategy is so popular that it even inspired an ETF – the ALPS Sector Dividend Dogs ETF (SDOG) – which invests in the highest-yielding stocks in each sector.

So, who are this year’s dogs? In escalating order of yield:

- Merck & Co. (MRK): 3.2% yield

- Caterpillar (CAT): 3.3% yield

- Exxon Mobil (XOM): 3.3% yield

- Coca-Cola (KO): 3.4% yield

- Cisco Systems (CSCO): 3.4% yield

- IBM (IBM): 3.4% yield

- Boeing (BA): 3.6% yield

- Chevron (CVX): 3.7% yield

- Pfizer (PFE): 3.9% yield

- Verizon Communications (VZ): 4.3% yield

Today, I’m going to take a look at the three “doggiest” Dogs – Chevron, Pfizer and Verizon. Not only do they currently offer the highest yields, but all three are excellent safety plays to boot.

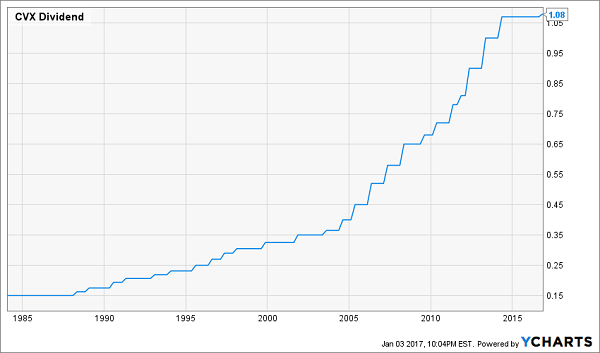

Chevron (CVX)

Integrated oil major Chevron isn’t quite what most people have in mind when they think about the Dogs of the Dow. That’s because many of the highest-yielding Dow stocks will be coming off more modest previous-year returns, breakeven performance or even decent-sized losses.

CVX, which ripped off 30%-plus gains in 2016, is precisely none of the above.

It’s almost laughable to think that at one point, a $220 billion energy behemoth could somehow have been at risk of a dividend cut, but that’s where we were sitting earlier in 2016 after ConocoPhillips (COP) slashed its payout by 66%. Low oil prices were gutting the sector, and Chevron took to cutting capital expenditures to protect its status as one of only two energy stocks with Dividend Aristocrat status. (Exxon is the other.)

Yes, it seems counterintuitive to think about a stock that lost more than 40% from 2014 peak to 2015 trough – and that many people considered a dividend risk – as “safe.” But oil’s plunge during that time was an extraordinary event that rocked an entire sector. And Chevron was so well-capitalized that it only had to reduce spending to keep its very generous dividend intact.

Meanwhile, CVX is back on the upswing, not just from a share-price perspective, but operationally speaking, too. Third-quarter results released in October included declines on both the top and bottom lines, but Chevron was plenty profitable and beat Street estimates. That was thanks in large part to capex spending and workforce reductions.

Perhaps most importantly: CVX upped the ante on its payout. It was only by a penny, but still – Chevron made good to investors during an ugly, ugly period for energy.

Chevron: A Dividend Aristocrat Through Thick and Thin

Now, Chevron is operating even more lean and mean while oil prices are recovering. Its debt is considerable at $45 billion, but decently offset by $42 billion in cash and investments. Meanwhile, CVX has left no doubt about the importance of paying out its dividend to shareholders.

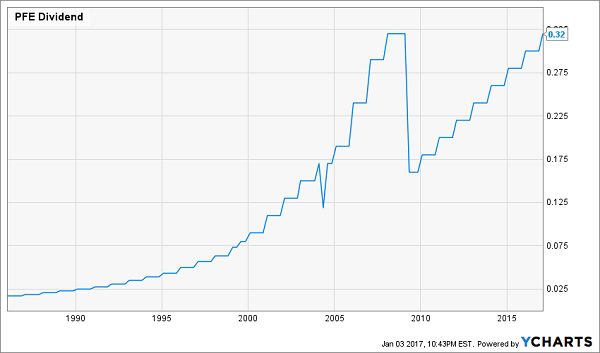

Pfizer (PFE)

Pfizer is no Dividend Aristocrat – in fact, the company halved its payout in 2009 alongside other gasp-worthy cuts, such as General Electric (GE). But the pharmaceuticals giant has been trying to make amends ever since – and in fact, with its most recent hike in December 2016, Pfizer’s payout of 32 cents per share has officially returned to pre-recession levels.

Investors might be worried about Pfizer’s payout ratio, which at current levels is more than 100% of the company’s earnings. But it’s worth noting a few asterisks, like the fact that one-time items have skewed this figure higher, and the fact that Pfizer’s earnings are expected to grow more than enough to cover the payout. And if you look at Pfizer’s dividend as a percentage of free cash flow, the figure is a much more reasonable 56.6%.

Pfizer’s Payout Is Back!

As far as Pfizer itself is concerned: It’s no mega-growth biotech, but expected five-year earnings growth of nearly 7% on top of its already generous dividend is encouraging.

Current drug offerings such as nerve and muscle pain treatment Lyrica and cancer medicine Ibrance are providing Pfizer with a strong baseline. Meanwhile, PFE’s growth prospects are being fueled by acquisitions such as Medivation and Anacor Pharmaceuticals, both made in 2016, as well as new indications for Ibrance and other medicines.

Moreover, Donald Trump’s election helped keep Hillary Clinton out of office – a boon for pharmaceutical and biotech companies alike, which likely faced reforms that would’ve clamped down on profitability.

PFE has been rangebound for several years now, but this Dog of the Dow could be primed for a big 2017. At the very least, investors’ money should be safe in this fine-yielding Big Pharma stalwart.

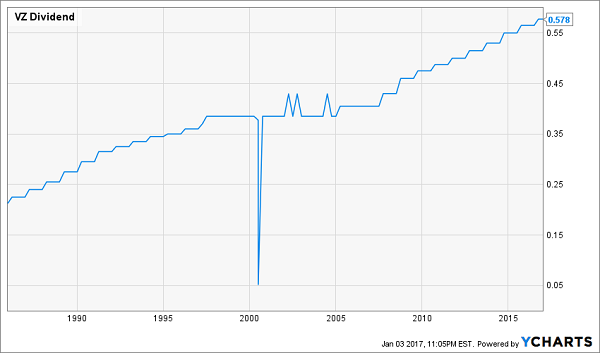

Verizon Communications (VZ)

Nothing screams safety quite like telecom’s duopoly of AT&T (T) and Verizon.

Mobile telecommunications are a basic human necessity at this point, giving T and VZ license to print recurring revenues from customers who are locked into service – even if they’re not necessarily always locked into a particular provider. But the options are few, with Sprint (S) and T-Mobile US (TMUS) the only other telco majors in the country who can compete at any kind of scale.

As a result, Verizon has posted positive returns in seven of the past eight years. And for as much as many pundits refer to telcos as “sleepy” and “glorified utilities,” the returns are far from boring – in five of those years, VZ has logged gains between 13% and 20%.

Investors might be skeptical of what’s ahead for Verizon in the wake of its $4.83 billion purchase of Yahoo’s (YHOO) core business, with the company reporting 500 million and more than 1 billion user accounts affected across a pair of data breaches in 2013 and 2014, respectively.

But the plan is a shrewd one that also involves its $4.4 billion purchase of similar seeming Internet dud AOL, as well as mobile ad marketplace Millennial Media, in 2015. Namely, Verizon is building a digital advertising business that will help provide growth as the mobile telecom business slows.

All the while, Verizon pays a 4%-plus dividend on a payout ratio that sits at about two-thirds of the telecom’s earnings. That leaves a little room to grow the dividend, even if modestly, and it’s certainly well outside the realm of concern that VZ can’t afford to write its quarterly checks.

Verizon Grows Its Dividend … And Has Room to Spare

Verizon might not always produce returns like the market-beating 16% it pulled off in 2016, but its leadership role in the telecom space should make it a secure dividend play at the very least – and its digital ad aspirations have the potential to drive outperformance in the future.

— Brett Owens

An 8% Yield You Can Depend On [sponsor]

2017’s Dogs of the Dow are blue-chip dynamos with bulletproof balance sheets and substantial dividends. That said, while 4% yields are nice, it’s difficult to retire on dividends alone.

No, you need about 8% in annual returns to get to where you want to be.

That’s a tall task for mega-cap companies like these Dow Jones companies. But my favorite stock can get you that – in cold, hard cash alone!

Let’s say you have a half-million dollars invested for retirement. Even with interest rates ticking higher, bonds will still net you, what, $15,000 every year? Even with Social Security tacked on, that’s not a comfortable retirement.

Thanks to medical advances, you and I are going to live much longer lives – but that means our money has to work harder, and longer, for us. Realistically, we need to be making about $40,000 annually on every $500,000 invested. That’s about 8%, which is more than the market returns on average.

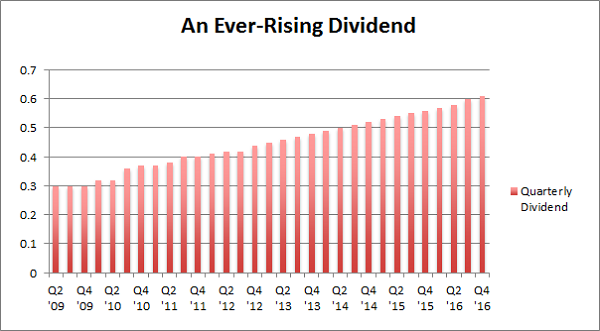

That’s why I’ve set my sights on a particular dividend stock right now that not only yields 8.5% right now, but also raises its dividend each and every quarter! So forget 8% in annual returns – if you also add in the projected capital gains on this sure-fire pick, you can expect a total return 17% between dividends and capital gains every single year!

I specialize in uncovering contrarian 8%+ income opportunities like my ever-rising dividend pick. Click here and I’ll explain more about my strategy and my favorite stocks and funds to buy for a secure retirement on just $500,000.

Source: Contrarian Outlook