With the election in the rear-view—and Inauguration Day just a few weeks off—plenty of investors have asked me what they should do with their portfolios now.

I’ll name five bargain dividend growers that should be on your buy list in a moment. But first, here are 2 sectors—and 9 stocks—you need to handle with care.

Let These 4 Growth Rockets Cool Down

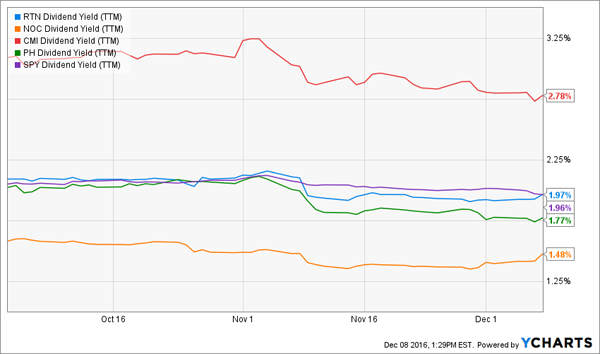

On October [4], I pounded the table on defense stocks, namely Raytheon (RTN) and Northrop Grumman (NOC), and infrastructure plays Cummins (CMI) and Parker Hannifin (PH).

I hope you followed that advice, because all four have beaten the SPDR S&P 500 ETF (SPY) since then.

If you missed out, I’m afraid you’re too late. Even though all four companies are great long-term holds, President-elect Trump’s infrastructure and defense plans (or at least what we know of them) look baked in, with RTN, NOC, CMI and PH all boasting price-to-earnings (P/E) near five-year highs.

If you missed out, I’m afraid you’re too late. Even though all four companies are great long-term holds, President-elect Trump’s infrastructure and defense plans (or at least what we know of them) look baked in, with RTN, NOC, CMI and PH all boasting price-to-earnings (P/E) near five-year highs.

The rise has also sent their dividend yields south, with all four yielding much less than they did in early October.

The rise has also sent their dividend yields south, with all four yielding much less than they did in early October.

To be sure, all four are prolific dividend growers, having hiked their payouts 53.8%, on average, over the past five years.

To be sure, all four are prolific dividend growers, having hiked their payouts 53.8%, on average, over the past five years.

[ad#Google Adsense 336×280-IA]But jumping in now puts you on the back foot if you want to build, say, a 10% yield on your initial buy.

The bottom line?

If you own these four stocks now, keep riding them for their soaring payouts.

If not, put them on your watch list and consider making a move if they pull back to pre-election levels in 2017.

5 Utilities With Little Spark

Before I get into where utility stocks could go under Trump, let’s bust one of the biggest myths about them: that they underperform when rates rise.

On the surface, it makes sense: utilities typically carry high debt loads. And as Treasury yields rise, they compete with Treasuries and other so-called “safe” investments for investors’ attention.

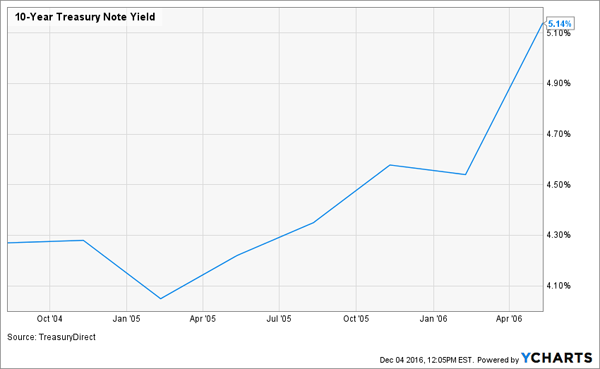

But their stock performance doesn’t back that up. Here’s how the Utilities Sector SPDR ETF (XLU) performed in the last rising-rate period, from July 2004 through June 2006:

That gain came in what should have been a brutal rate environment for utilities: in just this two year span, the Federal Reserve hiked rates from 1.25% to 5.25%, and 10-year Treasury yields spiked to 5.14% … yet investors still stayed true to utilities.

That gain came in what should have been a brutal rate environment for utilities: in just this two year span, the Federal Reserve hiked rates from 1.25% to 5.25%, and 10-year Treasury yields spiked to 5.14% … yet investors still stayed true to utilities.

It just goes to show that you need to question so-called truisms like these.

It just goes to show that you need to question so-called truisms like these.

With that in mind—as well as Trump’s promise to slash environmental regulations and revive coal mining—you might think now’s the time to pile into utilities like Duke Energy (DUK) and Southern Company (SO), both of which run large fleets of coal-fired plants.

Not so fast. Because in this case, I don’t think history is going to repeat.

For one, no matter what Trump does, utilities are well on their way to ditching King Coal: 94 coal-fired plants were mothballed in the US in 2015, with another 41 likely to go dark this year, according to the Energy Information Administration.

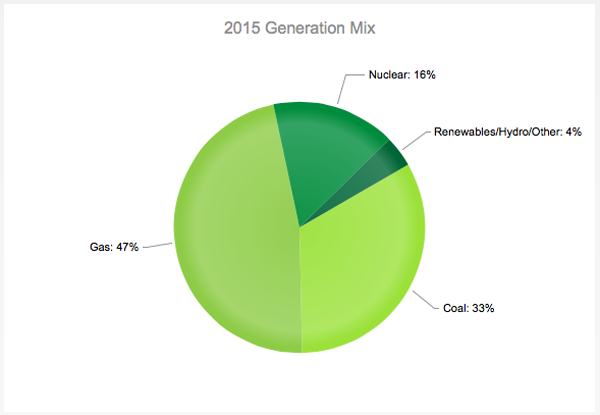

Natural gas is quickly filling the gap … and I mean quickly. Take a look at Southern Company’s generation mix, which went from 40% coal and 40% gas in 2014 to 33% and 47% just one year later:

Source: Southern Company

Source: Southern Company

So forget about coal rising from the grave and slashing utilities’ fuel costs. Meantime, despite the steep correction utilities have suffered since July, XLU remains well above its early 2016 lows:

Here’s where that leaves us. With both Duke and Southern trading at 18.1 and 17.9 times trailing-twelve-month earnings, they’re cheaper than they were in the summer but still above year-ago levels. On the less regulated side—which means automatic profits aren’t baked in—Exelon (EXC) boasts a P/E of 25.5; Calpine (CPN) is at a ridiculous 189, and NRG Energy (NRG) earned negative $18.31 a share in the past 12 months.

Here’s where that leaves us. With both Duke and Southern trading at 18.1 and 17.9 times trailing-twelve-month earnings, they’re cheaper than they were in the summer but still above year-ago levels. On the less regulated side—which means automatic profits aren’t baked in—Exelon (EXC) boasts a P/E of 25.5; Calpine (CPN) is at a ridiculous 189, and NRG Energy (NRG) earned negative $18.31 a share in the past 12 months.

My take? We’ll find much bigger upside—along with higher yields and faster dividend growth—in the 5 other stocks I’ll show you now.

Lock in These 3 REITs at a Discount…

Real estate investment trusts (REITs) are another asset class investors shun when rates rise. But as I showed you with utilities, doing so is a great way to miss out on gains. Here’s how the Vanguard REIT Index ETF (VNQ) did from July 2004 through June 2006:

Fast-forward to today, and VNQ is down 11% from its July highs and boasts a trailing-twelve-month yield of 3.7%. Add in accelerating economic growth and rising consumer spending (which boost demand for REITs’ offices, shopping centers and self-storage units) and you get a terrific time to jump in.

Fast-forward to today, and VNQ is down 11% from its July highs and boasts a trailing-twelve-month yield of 3.7%. Add in accelerating economic growth and rising consumer spending (which boost demand for REITs’ offices, shopping centers and self-storage units) and you get a terrific time to jump in.

Here are 3 great REITs to target:

Crown Castle International (CCI) is the largest provider of shared wireless infrastructure in the U.S. Mobile data usage is doubling every two years, and CCI owns cell towers and rents antenna space to carriers.

The company converted to a REIT structure two years ago. Since then, it’s hiked its dividend by 171%. The stock is down 2.0% year-to-date, and its trailing-twelve-month dividend yield sits at 4.2%—near the highest it’s been since CCI’s REIT conversion:

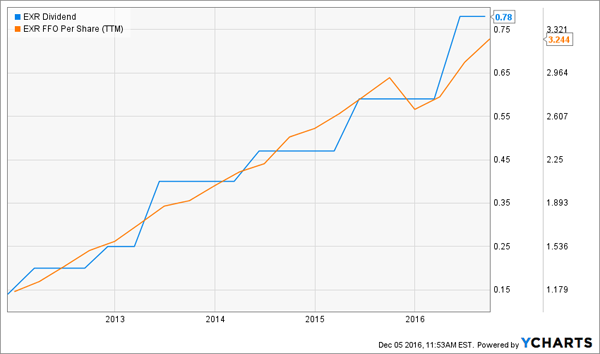

ExtraSpace Storage (EXR): Self-storage is about as recession-proof a business as you’ll find, as consumers buy more stuff when times are good and downsize their homes—and need a place to put their stuff—when the economy is weak.

ExtraSpace Storage (EXR): Self-storage is about as recession-proof a business as you’ll find, as consumers buy more stuff when times are good and downsize their homes—and need a place to put their stuff—when the economy is weak.

It’s a great business model, and it’s translated into soaring funds from operations (FFO; a better measure of REIT performance than earnings) for EXR—driving 457% dividend growth in the past five years.

The stock is also down 21% from its July peak, letting us lock in its 3.7% yield at a discount. And this is a payout you can count on, thanks to EXR’s rising FFO and reasonable (for a REIT) payout ratio of 69% of adjusted FFO. Buy this one now and store it away for years.

The stock is also down 21% from its July peak, letting us lock in its 3.7% yield at a discount. And this is a payout you can count on, thanks to EXR’s rising FFO and reasonable (for a REIT) payout ratio of 69% of adjusted FFO. Buy this one now and store it away for years.

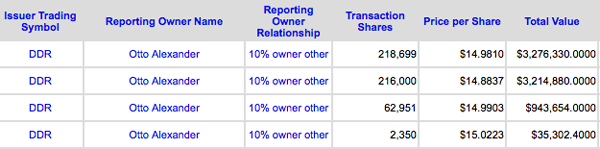

DDR Corp. (DDR): As I pointed out on [December 4], C-level executive Alexander Otto has been snapping up shares of his company of late: an eye-popping $7.5 million worth in November alone.

Source: InsiderTrading.org

Source: InsiderTrading.org

That’s worth paying attention to, because his buys line up perfectly with a jump in the stock’s yield, to over 5.0%—a six-year high—in early November. The payout currently sits around 4.8%, the highest of my 3 REIT picks:

DDR owns 352 malls across the U.S., and right now it’s a better buy than popular retail REIT Realty Income (O), trading at 17.3 times FFO, compared to 18.5 for O. DDR also tops O on the yield front and has delivered 138% payout growth over the last five years, more than tripling up O’s 39%.

DDR owns 352 malls across the U.S., and right now it’s a better buy than popular retail REIT Realty Income (O), trading at 17.3 times FFO, compared to 18.5 for O. DDR also tops O on the yield front and has delivered 138% payout growth over the last five years, more than tripling up O’s 39%.

A 2-Pack of Bargain Techs

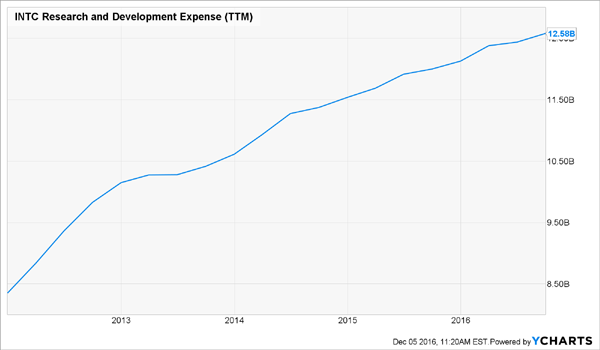

Intel (INTC) is one of many big-name techs that have lagged the market this year; the chipmaker now trades at a reasonable 16.9 times earnings and boasts a 2.9% trailing-twelve-month dividend yield. Payout growth is strong, too, with the dividend up 24% in the past five years.

First-level investors dismiss Intel as “old tech,” but they’re ignoring its surging R&D spend, which clocks in at 22% of its last 12 months of revenue:

That’s translating into big growth in areas like the Internet of Things, where Intel saw its revenue soar 19% in the third quarter. The company is also pushing into self-driving cars, carving out a separate division for that business and teaming up with Mobileye (MBLY) and Delphi Automotive (DLPH) to develop related tech.

That’s translating into big growth in areas like the Internet of Things, where Intel saw its revenue soar 19% in the third quarter. The company is also pushing into self-driving cars, carving out a separate division for that business and teaming up with Mobileye (MBLY) and Delphi Automotive (DLPH) to develop related tech.

Further payout growth is a lock: Intel pays out just 46.5% of its earnings as dividends, and its balance sheet sparkles, with $27.6 billion of debt—or just 17% of its market cap—and $17.8 billion of cash on hand. Snap this one up now.

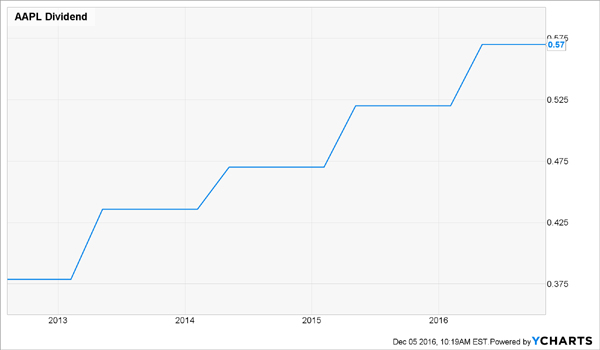

Apple (AAPL) is up 6.6% year-to-date, well below SPY’s 10.5% rise, and trades at just 13.5 times earnings. For that, you’re getting a stock yielding 2.0% but growing its payout at a 10.1% annualized clip. If Tim Cook and Co. keep that up, you can expect your payout to double every eight years.

iPhone 7 sales appear to be slowing, but that’s likely because Apple die-hards are holding out for next year’s iPhone 8, which will be a complete overhaul to mark the device’s 10th anniversary.

iPhone 7 sales appear to be slowing, but that’s likely because Apple die-hards are holding out for next year’s iPhone 8, which will be a complete overhaul to mark the device’s 10th anniversary.

Apple’s dividend and share buybacks could also surge if Trump follows through on his promise to let American companies repatriate cash held outside the US at a lower tax rate. The company’s overseas hoard has ballooned to $215 billion—or an amazing 37% of its market cap.

Apple is a rare bird in this overheated market: a bargain stock in a fast-growing industry that’s handing out double-digit payout growth.

— Brett Owens

Sponsored Link: It’s a great buy, to be sure … but my team and I have zeroed in on 3 stocks with even faster dividend growth than Apple and the 4 other picks above—and they’re even better bargains! I expect each of these overlooked income generators to deliver double-digit payout growth year in and year out—driving share price gains of 200%, 300% and more in 6 years or less!

How do I know?

Because that’s exactly what they’ve done in the last 6 years. Look at how one of these stocks’ payout hikes have driven eye-popping gains for its lucky shareholders:

And yet most investors, in a panic over interest rates, still ignore these hidden gems.

And yet most investors, in a panic over interest rates, still ignore these hidden gems.

That’s too bad, because as I showed you above, the lead-up to a string of rate hikes is a terrific time to buy dividend payers—and especially dividend growers.

Imagine if you’d bought utilities or REITs, for example, back in July 2004. When the Fed took its foot off the gas just two years later, you’d be up mid-double digits—and that doesn’t include dividends!

The upshot? It’s time for us to get greedy for yield—and dividend growth, too.

Start with my 3 favorite dividend growers, which I’m ready to show you now. Go right here to get their names and discover my proven dividend-investing strategy for yourself.

Source: Contrarian Outlook