Fidel Castro, Cuba’s longtime president, died late Friday night at age 90. It would have been so much better if he had lived just a few more days.

You see… on Friday, the Herzfeld Caribbean Basin Fund (CUBA) – an exchange-traded fund of companies that do business in Cuba and other Caribbean countries – closed at a 14% discount to its net asset value (NAV). The holdings of the fund were worth $7.43 per share. But CUBA closed Friday at only $6.38 per share.

[ad#Google Adsense 336×280-IA]In other words, buying CUBA on Friday was like getting a dollar bill for just $0.86.

Since the stock rarely trades at more than 4% below its NAV, I was looking forward to buying CUBA at a much larger discount than normal. But we never got the chance.

After Castro’s death, CUBA recovered the entire discount yesterday.

Shares of CUBA traded at more than $7.43. Now, it’s like buying dollar bills for $1.

You’re not going to make money doing that.

But here’s the thing… the action in CUBA is a good reminder of one of the most profitable and lowest maintenance investment strategies ever – buying closed-end funds at a larger-than-normal discount to their NAV.

And as I’ll show you below, another sector offers a similar chance to profit right now…

Most closed-end funds trade at a discount to NAV – 2% or 3% is about normal. But when the discount nears double digits, it often indicates an extreme situation… and can lead to a profitable move.

When a fund is trading for a larger-than-average discount to its NAV, it tells you one of two things: Either the market is already discounting a selloff in the fund’s underlying assets, or a large shareholder recently had to unload the stock in a hurry.

Either way, it’s an unusual situation that creates a good risk/reward setup for investors…

Consider the current action in the municipal-bond market…

The prospect of higher interest rates combined with the possibility of lower income-tax rates as suggested by President-elect Trump has caused a selloff in the municipal bond market. In general, municipal bonds have lost about 10% of their value over the past three months. Closed-end municipal-bond funds have suffered even greater declines.

Many of these funds – which normally trade at about a 1% discount to NAV – now trade at discounts of 8% or 9%. Investors are so convinced that municipal bonds will fall in value, they’re willing to sell closed-end municipal-bond funds for $0.91 on the dollar. So the current price of these funds already reflects a future decline.

If a decline happens, the funds won’t likely lose much more value since the current price already reflects it. And if a decline doesn’t occur, the prices of the funds will likely climb back up toward their NAVs.

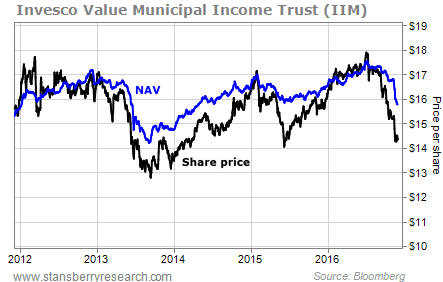

For example, take a look at this long-term chart of the Invesco Value Municipal Income Trust (IIM)…

Over the past five years, IIM has traded at an average discount of about 2% to its NAV. Today, it trades at a discount of more than 9%.

Over the past five years, IIM has traded at an average discount of about 2% to its NAV. Today, it trades at a discount of more than 9%.

IIM only traded at that large of a discount twice in the past five years – September 2013 and August 2015. Each time turned out to be a terrific buying opportunity as shares rebounded and IIM returned to trading at its normal discount.

Several other closed-end municipal-bond funds feature the same setup today.

Buying closed-end funds at a larger-than-normal discount to NAV creates a good risk/reward setup for investors.

It was a profitable strategy for anyone who owned CUBA over the weekend. And I suspect it will be a profitable strategy for folks buying closed-end municipal-bond funds today.

Best regards and good trading,

Jeff Clark

[ad#stansberry-ps]

Source: Growth Stock Wire