It has been an emotional couple of weeks for people in the U.S.

First, the World Series divided the nation into Chicago and Cleveland fans. Then, earlier this week, the presidential election tested their wills.

It’s the same thing with investing in the notoriously cyclical, up-and-down, swingy world of natural resources. Few resource stocks are “buy and hold” investments.

[ad#Google Adsense 336×280-IA]So as a resource investor, you need to be selective.

Today, I’ll show you the best of the bunch…

The closest things to “buy and hold” in the resource market are royalty companies.

Royalty companies make for great investments because they don’t actually operate mines.

Instead, they finance lots of mining projects at various stages of completion, then earn revenue streams (or “royalties”) on mine production if things work out.

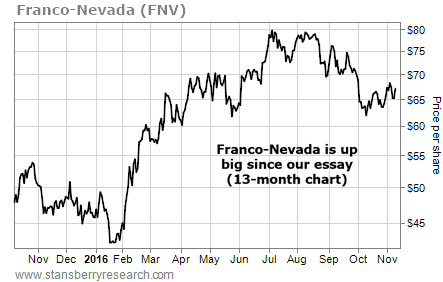

In the October 7, 2015 Growth Stock Wire, I explained why precious metal and energy royalty company Franco-Nevada (FNV) was my favorite of the group.

Back then, shares traded around $48.50. On Wednesday, they closed at $67.10 – a 38% gain. The stock pulled back yesterday, but it’s still way up since we published that essay. (Plus, Franco-Nevada has paid $0.86 in dividends since then.)

Since going public in September 2011, Franco-Nevada has vastly outperformed the VanEck Vectors Gold Miners Fund (GDX).

Since going public in September 2011, Franco-Nevada has vastly outperformed the VanEck Vectors Gold Miners Fund (GDX).

Part of that is because royalty companies are less risky bets than gold miners. In general, miners own a handful mines. Royalty companies, on the other hand, own stakes in the production of many mines. So one mine shutting down hurts the cash flows of miners far more than it does for royalty companies.

The other reason Franco-Nevada is a top royalty company is because its management is world-class.

During the precious metals market downturn that ended in early 2016, Franco-Nevada’s management focused on adding quality royalties to its stable. As a result, FNV reported blowout third-quarter earnings. It reported record revenues… record earnings before interest, taxes, depreciation, and amortization… and the highest quarterly GEOs (“gold-equivalent ounces produced,” the earned production converted to gold).

One of the royalties Franco-Nevada added was a silver stream on the Antamina copper and zinc mine in Peru. Diversified metal producer Teck Resources operates the mine.

Antamina has been in production since 2001 but has a long way to go. Franco-Nevada purchased Teck’s interest in all of the silver at Antamina for $610 million.

At today’s prices, Franco-Nevada will get nearly all of its investment back when Teck produces the reserves (the silver in the ground that Teck can produce at a profit). It will effectively get the resources (the silver that exists but may not yet be profitable) for free… And Antamina has two times more resources than reserves.

This was Franco-Nevada’s first pure silver stream. So far, so good… In the first nine months of this year, Franco-Nevada earned 25% more ounces than it expected to generate in all of 2016.

Franco-Nevada’s investment in Antamina is a great example of a management team that knows what it’s doing and is making smart deals… at the right time and for the right price.

It’s also a great example of why we like the royalty model so much.

If you’re like me and believe we’re in the early stages of a huge bull market in precious metals, pick up shares of Franco-Nevada (FNV) today.

Good investing,

Brian Weepie

[ad#stansberry-ps]

Source: Growth Stock Wire