“Uncertainty is the only certainty there is, and knowing how to live with insecurity is the only security” – John Allen Paulos

It is hard to believe that Halloween has already come and gone; and that we are now heading into the home stretch of the year with less than a week to go before a contentious election season is resolved.

[ad#Google Adsense 336×280-IA]2016 had looked very much like 2015 from an investment point of view.

The market indices have largely moved sideways, investors continue to be obsessed with the Federal Reserve’s next move, the economy continues to limp along, and there is little in the way of revenue or earnings growth within the overall market.

The third quarter did see the best GDP print in many, many quarters, but the economy has grown at an anemic 1.5% pace over the past year. The weakest post-war recovery seems to have lost a bit more steam in its eighth year.

As Yogi Berra once famously quipped “It is tough to make predictions, especially about the future”. Nonetheless, here are a couple of themes I think will play out in the market in the year ahead.

Biotech Will Bounce Back:

After the first presidential debate and some fortuitously timed videos from over a decade ago put Mr. Trump’s boorish behavior in full focus, it seemed it was possible that the Democrats would achieve a clean sweep of the House, Senate, and the White House come November 8th despite Mrs. Clinton’s own high negative ratings.

This would have given tremendous clout to the Sanders and Warren wing of the party. Their pious focus on the pharma and biotech sectors and rhetoric and tweets on drug price “gouging” are well known and have resulted in more than one pharma CEO being hauled before a congressional subcommittee.

This has been a primary driver of the 10 percent decline that the biotech sector experienced in October. The sector is currently down 35% from its last peak in the summer of 2015.

However, the presidential race was already tightening before the FBI’s bombshell last Friday that they were reopening their investigation into the broadening email scandal of the frontrunner. The House is now almost a lock to stay in Republican hands and the Senate is looking more like a 50/50 proposition to not “flip” as we go to print.

If we do get a mixed government come November 9th, I would expect a yearend rally for the sector as legislative changes that could have negatively impacted the biotech and pharma industries will be largely off the table. If Republicans manage to retain the House and the Senate, I would expect a substantial rally in this part of the market next week.

Bargains thrive in the sector as the large cap names sell at their lowest collective valuation levels in at least five years.

Bargains thrive in the sector as the large cap names sell at their lowest collective valuation levels in at least five years.

Many small caps have also fallen 25% to 30% in October for no other reason than dismal sentiment on the sector.

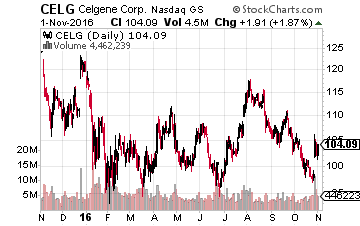

In the former category, investors should love Celgene (NASDAQ: CELG) at current levels.

This biotech stalwart easily bested expectations with its quarterly report last week on a better than 25% year-over-year surge in revenues.

The stock is selling at a deep discount to its long-term growth trajectory.

The stock is selling at a deep discount to its long-term growth trajectory.

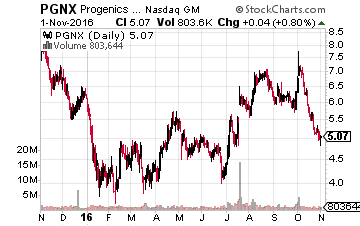

Omeros (NASDAQ: OMER), Progenics Pharmaceuticals (NASDAQ: PGNX) and Aratana Therapeutics (NASDAQ: PETX) are just some of the small cap names I have profiled on these pages that have gotten way too cheap.

Oil Should Move Higher In 2017:

After plunging from over $100 a barrel in the summer of 2014, crude oil put in a bottom in the low $20s after the panic selling that opened 2016. Over the past six months or so, oil has traded in a relatively tight range of approximately $40 to $50 a barrel. Both the floor and the ceiling of this range have been tested many times in previous months but this seems to be the range we are locked into through at least yearend.

Provided we do not see a global recession in 2017, crude should probably move somewhat higher. Hundreds of billions of dollars in long-term energy projects have been shelved, postponed or canceled over the past two years as energy producers have slashed capital budgets. In addition, the huge fall in oil prices have severely hurt oil producing states’ finances. I predict the long rumored hard “production freeze” agreement among OPEC nations and Russia will get done sometime early in 2017.

I think we should see oil break out of its recent tight range to the upside in the first half of 2017. I don’t expect oil to get anywhere close to levels we have seen in the recent past, however. North American shale plays have become the “swing producer” in the global market. They have also drastically cut production costs and can ramp up relatively quickly. That being said, I would not be surprised if oil drifts up into the $60 the $75 range in 2017.

This should be of great help to domestic Exploration and Production companies, especially those with good acreage, relatively low debt loads and attractive operational costs.

This should be of great help to domestic Exploration and Production companies, especially those with good acreage, relatively low debt loads and attractive operational costs.

I have started to dip my toe into this sector for the first time in over a year recently.

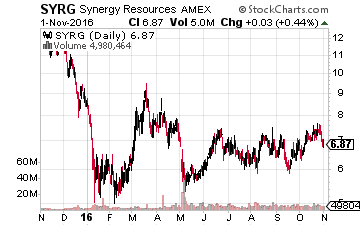

A well-positioned producer like Synergy Resources (NASDAQ: SYRG) is one of my recent purchases.

The company has great acreage, low costs and has also seen insider buying in its shares recently. Synergy has also seen several buy ratings from analysts over the past month or so. If oil does break out to $60, it should be a strong performer in 2017 like other Exploration and Production plays.

— Bret Jensen

[ad#ia-bret]

Source: Investors Alley