It’s an old investing saw that should have been taken out behind the barn years ago.

You’ve no doubt heard it before: “As you get closer to retirement, you should shift out of stocks and into fixed-income investments.”

You’ll often hear it in combination with some arbitrary rule, like: “The percentage of your portfolio devoted to stocks should be 100 minus your age.”

[ad#Google Adsense 336×280-IA]An Overblown Fear

On the surface, it seems like sound advice, right?

After all, CDs, Treasuries and the like guarantee your principal, and stocks don’t.

But it’s based on a dangerous misconception: that “guaranteed principal” and “no risk” are the same thing.

They’re not. Because moving from stocks to fixed income really amounts to swapping one risk for another: market-volatility risk for its silent—and deadlier—cousin: longevity risk, or the very real chance you’ll outlive your nest egg.

Consider bonds, easily my top pick for the worst retirement investment you can own right now.

It’s true that bonds guarantee your principal at maturity (unless, of course, the issuer defaults). But by moving away from, say, dividend stocks yielding 4% and up into bonds paying around 1.8%—as 10-year Treasuries are as I write this—you’re giving up a lot of income, not to mention gain potential, for that so-called stability.

Source: T. Rowe Price Group

Source: T. Rowe Price Group

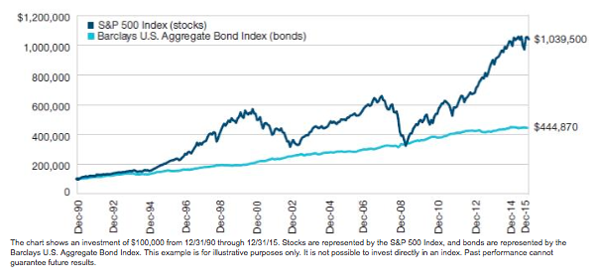

Worse, the thing you’re buying “insurance” against—the risk of racking up big losses because of a stock-market meltdown—is something that has just a 3% chance of happening for timelines as short as 10 years out.

That’s according to a recent study by T. Rowe Price Group (TROW) that looked at the 81 rolling 10-year periods between 1926 and 2015. The finding? The S&P 500 failed to post gains in just four of those periods. That’s a 97% “batting average”!

How to Build a Safe All-Stock Retirement Portfolio

Today, I’m going to give you two ways to whittle your risk down even more, starting with…

Dollar cost averaging: This is my favorite way to “time” the market because it lets you take advantage of pullbacks and hedge your bets when stocks turn pricey … literally in your sleep.

It’s dead simple—all you have to do is buy a fixed amount of stock on a fixed schedule, perhaps as more cash becomes available. In that way, it’s the reverse of the fossilized “shift to fixed income” idea above.

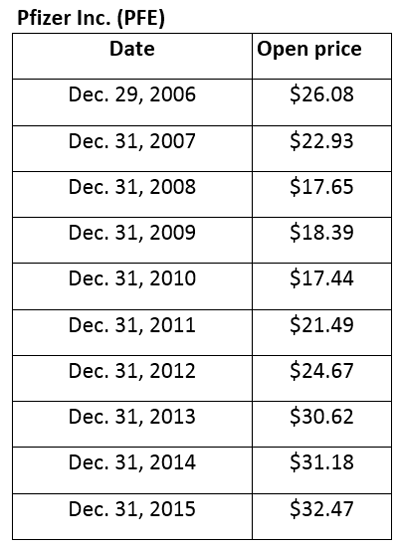

Here’s how it works, using Pfizer Inc. (PFE) as an example, because it’s a stock many investors hold, either directly or through, say, ETFs or closed-end funds. To keep with T. Rowe Price’s findings, we’ll use a 10-year timeframe, starting with your first purchase in December 2006 and your latest one in December 2015.

Let’s say your order is processed at the stock’s opening price on the last trading day of each of these years. Here’s what you would have paid:

As you can see, over that time, your purchase price would have ranged from $17.44, when your $5,000 would have gotten you 286 full shares (not including commissions) to $32.47, good for 153 shares.

However, your average purchase price would have been $24.29 a share, below both the stock’s average price of $29.28 during that time and today’s price of around $32.80.

And these numbers don’t include Pfizer’s dividend payments, which have grown in that time, too.

Which brings me to…

Dividend Payers: Your Retirement Portfolio’s Best Friend

As you can probably tell from this example, I’m a big fan of stocks that pay—and continuously grow—their dividends.

The reason is simple: dividend payers consistently outperform the market as a whole, and dividend growers do even better.

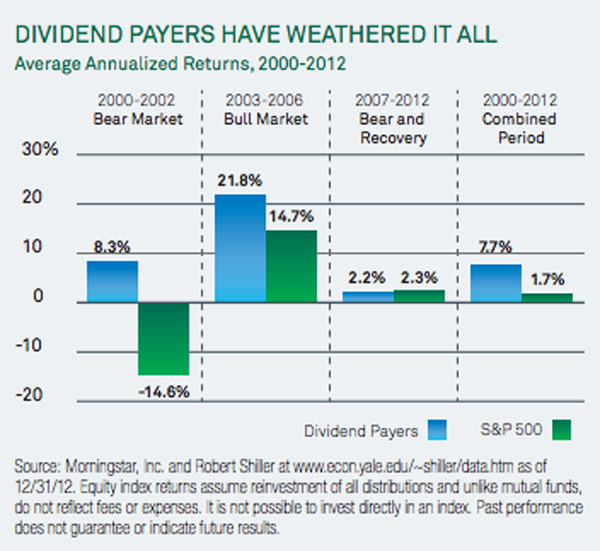

Take the 12-year period between 2000 and 2012, a span that included two nasty bear markets. During that time, dividend payers returned a respectable 7.7% annually, compared to just 1.7% for the S&P 500:

It’s obvious what you need to do to build a retirement portfolio that churns out predictable gains and the income you need once you hang it up—you need to buy dividend-paying stocks.

3 Great Retirement Stocks to Buy Now

Here are three dividend growers that would make solid additions to any retirement portfolio, either all at once, through dollar-cost averaging or a combination of the two.

Lockheed Martin (LMT) doesn’t boast the highest dividend yield out there, at 2.9%. But that doesn’t matter much when you consider that the quarterly payout’s soared 371% in the past 10 years! Heck, LMT even kept hiking through the financial crisis.

Three more factors will keep the hikes coming: rising profits, with earnings per share (EPS) expected to jump 6% in 2017 and 14% in 2018; a reasonable 40.0% of free cash flow (FCF) devoted to dividends; and a tight relationship with the US government, which is all but guaranteed to spend more on defense no matter who wins the election.

Comcast Corp. (CMCSA) also looks thin on the payout front, with just a 1.7% yield.

But as with LMT, that masks incredible dividend growth, to the tune of 340% in the past decade! That’s driven the share price up by 269%, which accounts for the low yield (because you calculate yield by dividing the annual dividend by the current share price).

If cord cutters are supposed to be decimating Comcast’s cable business, management didn’t get the memo: revenue and earnings are both on the rise, and Wall Street sees that continuing, with a forecast 8.6% EPS increase next year and a 9.9% gain in 2018.

Throw in a dividend that accounts for just 28% of FCF, and there’s plenty of room for more hikes. Buy this one now, before its soaring payout yanks the share price further away from us.

MetLife, Inc. (MET), like other insurers, is cursing low interest rates because they crimp the profits it earns by investing the premiums it collects. That’s why MET trades at just 65% of book value and 10.2 times forward earnings.

The upside? MET’s dividend yield now stands at an attractive 3.4%, and with the company’s price-to-FCF ratio clocking in at a measly 12.6%, management has plenty of room to juice that payout higher.

MET is getting set to spin off its US retail business, while at the same time arguing for the removal of its designation as a “systemically important financial institution,” and the costly regulatory burdens that come with it. The spinoff and/or progress on the SIFI front would spark the stock—and set the stage for strong long-term gains.

MetLife, Comcast and Lockheed Martin are great buys now, but the highest yielder of the bunch, MetLife, pays just 3.4% today.

— Brett Owens

Sponsor: What if you need a far greater income stream right away?

There’s a way you can have dividend growth and a healthy income stream now with my “no-withdrawal portfolio.” It lets you live off your dividend payouts without ever having to sell a share.

After all, why should you rely on stock price appreciation in an inflated market when there are secure, high-paying dividends you can simply live off of and keep your capital intact?

Most investors know this is the right approach to retirement. Problem is, they don’t know how to find 7% and 8% yields to fund their lives.

That’s why I specialize in finding safe, under-the-radar high-income options. Click here and I’ll explain more about my no-withdrawal approach—plus [more information on] my two favorite high-income plays for 7.6% and 7.7% yields.

Source: Contrarian Outlook