Investors got a good reminder last Friday that equities don’t always grind up in listless trading with low volatility. After over 40 straight sessions where the S&P 500 neither rose or fell by as much as one percent, stocks fell hard on increasing worries that the Federal Reserve might actually hike rates.

If not in September, then it is more than likely an increase will come in December. This is the scenario I am preparing for as I just don’t believe Chairwoman Yellen will interject in the markets right before a contentious and narrow presidential election.

[ad#Google Adsense 336×280-IA]That just isn’t how things are done in Washington.

The S&P 500 and the NASDAQ dropped more than two and a half percent on Friday.

Small caps and biotech were down a bit more than three percent on the day.

Shockingly, the “low-beta” Utility sector was down nearly four percent in one day as the ten-year treasury yield hit levels not seen since early summer, albeit still under an anemic 1.7%.

What this sudden downdraft should tell investors is that portions of the market are “overbought”.

Some of the high-yield stocks that income seekers have bid up to extreme valuations in their desperate search for any kind of yield in this low interest rate environment are frankly priced for perfection.

However, there are still pockets of value, such as some of the large biotech concerns that collectively sell at their lowest valuations to the overall market in over a decade. Some homebuilders are looking cheap given that housing activity should continue to strengthen over the next few years because of the large amount of pent-up demand, below-trend volume of housing starts over the past 10 years, as well as historically low mortgage rates.

I am keeping a relatively large allocation (~20%) to cash within my own portfolio at the moment as I think there is a good possibility of some better entry points in the market over the next six to 12 months.

I am keeping a relatively large allocation (~20%) to cash within my own portfolio at the moment as I think there is a good possibility of some better entry points in the market over the next six to 12 months.

The rest of my portfolio is situated in the “pockets of value” mentioned above.

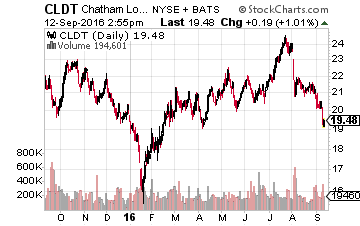

Good yield plays within a reasonable priced lodging REIT are Chatham Lodging Trust (NASDAQ: CLDT) and also other companies that either have upcoming catalysts that are likely to be positive and/or improving business fundamentals.

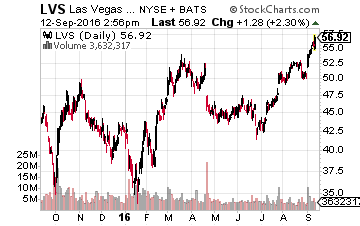

In the latter category is Las Vegas Sands (NYSE: LVS).

In the latter category is Las Vegas Sands (NYSE: LVS).

It appears after almost two years of year-over-year declines in traffic, business in the mega gambling enclave of Macau is finally starting to pick up again.

All the major casino operators are benefiting from this trend including Wynn Resorts (NASDAQ: WYNN).

However, Las Vegas Sands has less exposure to the VIP segment, which has been hurt by the Chinese crackdown on “corruption” more than any other operator. In addition, the Parisian Macao opens this year. This 3,000 room resort just got a big gaming table allocation from authorities and should be a major contributor to revenue in 2017.

The resort opens this month. It also means that capital expenditure needs will drop sharply for Las Vegas Sands over the next two years. With Las Vegas traffic picking up, undervalued luxury retail properties, and an over five percent yield, there is a lot to like about this stock right now.

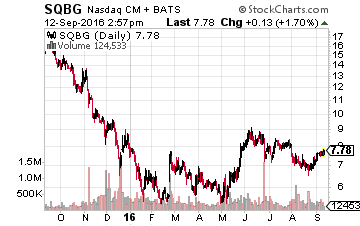

At this price, Sequential Brands Group (NASDAQ: SQBG) screams great value.

At this price, Sequential Brands Group (NASDAQ: SQBG) screams great value.

This brand manager spent most of 2015 almost doubling its global sales footprint by making four major acquisitions including the entire Martha Stewart brand.

2016 was spent integrating this business line into the company’s overall business model and processes.

Earnings this year are largely tracking to be flat to last year even as revenues surge 80%. 2017 will be the payoff with the consensus projecting earnings will increase at least 50% in FY2017. At approximately 10 times next year’s profit projections, the stock is going to look cheap when looking in your rearview mirror.

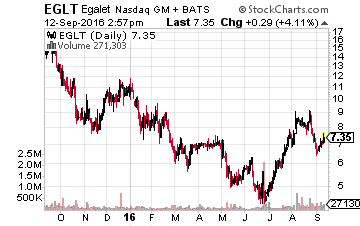

Finally, Egalet (NASDAQ: EGLT) has become a recent purchase in my portfolio.

Finally, Egalet (NASDAQ: EGLT) has become a recent purchase in my portfolio.

Its abuse resistant compound for chronic pain “ARYMO ER” has a PDUFA date with the FDA on October 14th.

In early August, the Ad Comm panel assigned to review this drug voted 18 to 1 to recommend it, so approval seems a formality.

For a company with less than a $200 million market capitalization, this will be an important catalyst and the stock is already starting to move in anticipation of approval, rising some 10% over the past week to just under $7.50 a share.

Further upside appears likely. The company has funding in place to successfully roll out ARYMO ER upon approval. H.C. Wainwright reiterated its Buy rating and $21.00 a share price target last week on Egalet noting they view this compound as superior to Pfizer’s (NYSE:PFE) competing drug, Embeda which is highly addictive and garners just less than 10,000 scripts a month.

— Bret Jensen

[ad#ia-bret]

Source: Investors Alley

Positions: Long CLDT, EGLT, LVS & SQBG