“Are dividend stocks in a bubble? Like… the NASDAQ in 1999?”

A reporter from Kiplinger called me last week, concerned investors were bidding up these issues to irresponsible heights.

While not quite a bubble, many of the “safest” names are the worst places you could put your money today. Some are doomed to grind sideways for years while others have serious downside potential. But there’s an easy test you can run to see if you should buy, hold or sell your favorite dividend stocks – simply chart the share price versus the dividend.

Your Total Returns = Current Yield Plus Payout Growth

[ad#Google Adsense 336×280-IA]Over time your stock market returns will roughly equal the yield you buy today plus the dividend growth you enjoy in the years ahead.

Notice I didn’t mention the stock price itself. Reason being, the price is easy to figure out – it grows along with the dividend.

Take General Mills (GIS), which has rewarded investors with 263% total returns over the past 10 years.

Not bad for a boring cereal maker! Almost two-thirds of the return was thanks to the growth of the payout (+174%), which the stock price tracked almost to a tee (+169%):

How To Time GIS: Buy When Price (Blue) Lags Payout (Orange)

As you can see in the chart above, you’d have made outsized gains buying GIS when its stock price lagged its payout. It’s big 2016 is thanks to another healthy dividend boost and a share price that finally caught up.

As you can see in the chart above, you’d have made outsized gains buying GIS when its stock price lagged its payout. It’s big 2016 is thanks to another healthy dividend boost and a share price that finally caught up.

Today GIS looks fairly priced with respect to dividend growth, but richly priced with respect to earnings, slowing sales growth and fresh food trends. Investors obsess over storied dividend histories, but it’s future payout boosts that are needed to drive future price gains. In this case, I’m worried that previous catalysts are fading.

Current Low Yields Mean Low (or No) Future Returns

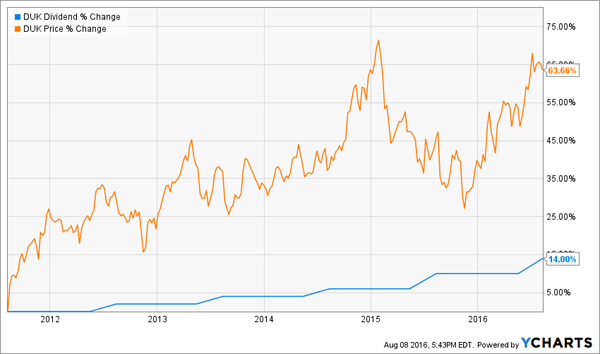

Consumer blue chips aren’t the only expensive stocks on the market today. Many popular utilities look pricey with respect to their yields, too. Slow growing stalwarts Duke Energy (DUK) and Southern Company (SO) have recently seen their share prices decouple from their anemic dividend growth:

Duke Soars as Investors Get Desperate for Dividends…

Duke recently doubled its payout growth rate to a still-sleepy 3.6% annually, while Southern last clocked a 3.2% increase. Now investors are assuming they can simply add dividend growth with the current yields (4.1% and 4.3%) to lock in secure 7-8% total returns, with about half heading into their pockets as cash.

Duke recently doubled its payout growth rate to a still-sleepy 3.6% annually, while Southern last clocked a 3.2% increase. Now investors are assuming they can simply add dividend growth with the current yields (4.1% and 4.3%) to lock in secure 7-8% total returns, with about half heading into their pockets as cash.

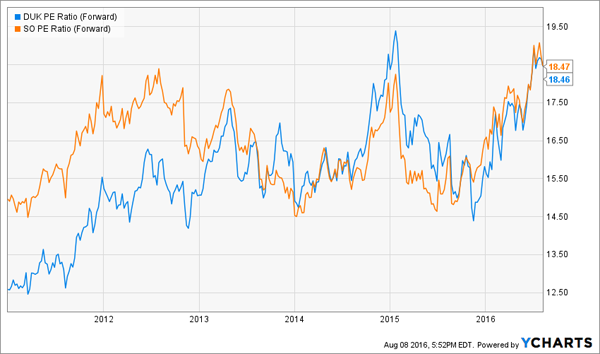

The problem with this thinking is it ignores valuation. Expanding price-to-earnings (P/E) ratios are the sole reason for these recent share price gains. And what if investors decide they don’t want to pay 18-times next year’s earnings for a slow growing utility? The P/E ratio will contract, and those 7-8% gains could quickly disappear.

Forward P/Es at Recent Highs

I pick on Duke and Southern but the absolute dumbest buys in the sector are perennial problem children Exelon (EXC) and FirstEnergy (FE). If you’re buying them for dividends, you’re playing with fire – for absolutely no reason.

I pick on Duke and Southern but the absolute dumbest buys in the sector are perennial problem children Exelon (EXC) and FirstEnergy (FE). If you’re buying them for dividends, you’re playing with fire – for absolutely no reason.

Our favorite dividend health screen DIVCON is flashing warning signs for both payouts, which are both lower than they were five years ago. Their modest yields – 3.5% and 4.1% respectively – aren’t enough to compensate for the risk of a dividend cut, which would be catastrophic to your capital.

REITs Looking Risky, Too

Remember when real estate investment trusts (REITs) were screaming bargains? If it feels like just last year – well, it was.

Late last year, the Vanguard REIT Index ETF (VNQ) was paying its highest yield this decade. The recent rush to REITs quickly corrected this – and actually launched a few of the bigger names towards bubble territory.

Healthcare REIT Ventas (VTR) paid a 6% yield as recently as February – it now pays just 4% thanks to a 45% rally since our feature six months ago . Back then, it was an obvious buy because its dividend growth had outpaced its share price gains – resulting in a yield near historic highs:

High Yield Made Ventas An Obvious Buy Then…

… And It’s Low Yield Makes It An Obvious Sell Now

… And It’s Low Yield Makes It An Obvious Sell Now

Rising prices are great if you already own the stock, but they are counterproductive for those of us looking to put new money to work! Even reinvested dividends will generate a lower return after a rally – which means we must focus on ignored areas of the income universe that still offer value.

Rising prices are great if you already own the stock, but they are counterproductive for those of us looking to put new money to work! Even reinvested dividends will generate a lower return after a rally – which means we must focus on ignored areas of the income universe that still offer value.

— Brett Owens

3 Stocks Set To “Catch Up” To Their Dividends [sponsor]

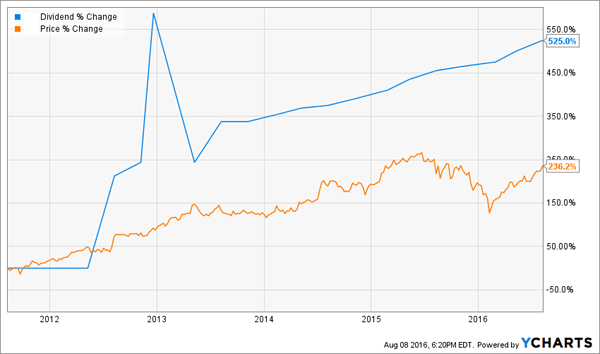

While large caps like General Mills, Duke Energy and Ventas are getting the headlines and hot money today, tomorrow’s top performers will be the midcap stocks with prices set to “catch up” with their soaring dividends. For example, my favorite firm has raised its dividend by an amazing 525% over the past five years thanks to soaring profits and a cash cow business that doesn’t require much in the way of reinvestment. But its stock price has “only” returned 236%.

As a result, its yield is near historic highs despite the fact that the business is growing faster than ever. Its stock has limited analyst coverage and simply hasn’t been able to keep pace with payouts:

This Stock Has Another 289% To Go!

This “289% lag” will correct itself soon, and likely in a hurry as the dividend bubble expands to lesser-known names. In fact, I’ve identified two more stocks that will cruise higher as their prices catch up with their dividends.

This “289% lag” will correct itself soon, and likely in a hurry as the dividend bubble expands to lesser-known names. In fact, I’ve identified two more stocks that will cruise higher as their prices catch up with their dividends.

Like Ventas, they’re all healthcare REITs. But unlike Ventas, they are lesser-known names that haven’t yet benefited from the big rush into REITs – which makes right now the perfect time to buy them, because we can actually secure yields up to 8% while we enjoy potential 50% upside. Click here and I’ll share [more information and their] dividend growth history along with my optimal buy prices.

Source: Contrarian Outlook