Around three weeks ago, I recommended a stock I called the “2016 Market MVP,” the most valuable player in one of this market’s strongest, most compelling comeback stories.

What investor doesn’t love a good comeback story? After all, they start with irresistible prices and end with outsized gains.

[ad#Google Adsense 336×280-IA]Now, my Private Briefing readers who’ve been following my recommendations have owned this innovative firm for a while now, and as a result, they’ve bagged peak gains of more than 79%.

But I’ve just seen a report that suggests this stock could more than double our money.

That’s why I wanted to “go big” and let everyone know how they can become a part of this comeback story and follow along to potential gains as high as 130%.

And with the pullback in stocks over the past few days, new investors have a golden opportunity – served up on the proverbial silver platter – to get in at a price that’s highly unlikely to come again.

The Best Gold Play on the Market

And as far as comeback stories go, you just won’t find a better one than gold.

We started closely following gold’s current “story line” back on Feb. 16. And we told you to start investing in the metal then, before it started to surge.

Those have turned out to be great calls…

Gold prices are up more than 24% since the start of 2016 amid plenty of uncertainty – including the United Kingdom’s Brexit vote, which has thrown the global economy and currencies into turmoil.

Brexit, and a backdrop of negative interest rates, have been key drivers for gold this summer, causing market players to flee to this safe-haven investment.

Last week was an interesting one for the yellow metal. Gold was once again flirting with two-year highs, as it did in June, before taking a hit behind a jobs report that was stronger than expected – that’s the key to the buying opportunity we’re looking at right now.

Once the market digests (and discounts) the jobs report, we’ll still have a vivid backdrop of not-unfounded fears of financial chaos – fears that are likely to intensify and send gold back into “rally mode,” boosting the profits in the shares I’m about to show you.

So far this year, gold has managed to hold above $1,300 per ounce and continues to trend higher.

This is a really interesting situation.

The stock market is overall in rally mode, too, with the Standard & Poor’s 500 and the Dow Jones Industrial Average hitting new highs in mid-July – and staying near there since then.

And bonds are rallying as well – not what you’d expect when the stock market breaks new highs.

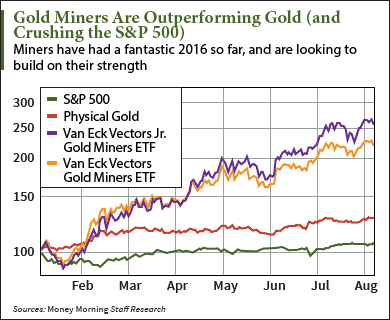

But the most interesting thing is that investors looking to chase the strong rally in gold won’t see the biggest gains in the metal itself.

The Gold Play That’s Doing Even Better Than the Metal

Gold miners have been the real outperformers in this market.

Gold miners have been the real outperformers in this market.

Truth is, the year-to-date gains for miners that produce gold have been incredible and have not faced any kind of a serious pullback.

When I wrote three weeks ago, I joked that an investor could pretty much throw a dart at a list of gold miners and pick a winner.

And this is one of the most lucrative gold miners in the game…

It’s Goldcorp Inc. (NYSE: GG).

Like I said, gold miners have had an unstoppable run this year.

Of the 28 gold-mining stocks with a market valuation of at least $300 million, every last one is outperforming the S&P 500.

What’s more, 20 of the 28 have at least doubled, with 10 of the 28 having tripled in value (or more).

But Goldcorp is something else again.

You see, over the years, Goldcorp has hammered itself into one of the mining sector’s most efficient gold producers – responding to the drop in gold prices earlier this decade by slashing costs (capital outlays will drop to about $1.4 billion this year, from $2.2 billion a year ago).

The result: According to one of the latest reports, the company dropped its “all-in” mining costs to below $850 an ounce last year. And the company said it can achieve an even lower cost this year. As gold prices move higher, Goldcorp’s margins will expand – and its share price will surge.

Since Jan. 1, shares of this best-in-class senior gold miner have soared 56%. That’s 10 times the gains than those of the S&P 500 – and almost twice as much as gold itself.

Recent high operating costs were responsible for a lack of investor interest in late 2015. But after a series of savvy moves, Goldcorp is coming back.

Management plans to cut $500 million in mine-site costs and corporate expenses over the next two years. The company is also ramping up output at two new production sites that began commercial production last year.

Goldcorp says it will produce 2.8 million to 3.1 million ounces this year at an “all-in sustaining cost” (AISC) of $850 to $935 per ounce. Even at today’s lower price of gold, that’s close to $500 in pure cream.

And its balance sheet remains impeccable. With a market cap of $15.37 billion, the company is carrying $2.7 billion in debt and has more than $3.2 billion in available liquidity.

Analysts have a high-water price target of $26.50 on Goldcorp, which is 47% up from current prices and nearly 130% above where shares were on Jan. 1.

Truth is, we’re only in the beginning stages of a bullish gold market, and that means this miner has a bright future on the horizon.

— William Patalon III

[ad#mmpress]

Source: Money Morning