Something funny has happened in the U.S. oil patch over the past couple of years…

During the U.S. Energy Information Administration’s (EIA) annual conference at the Washington Hilton earlier this month, the only oil bull in the room explained why.

[ad#Google Adsense 336×280-IA]It all comes down to money…

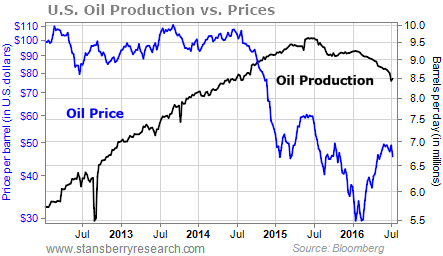

As oil prices fell 73% from mid-2014 through this past February, production continued to climb.

When production finally began to decrease, it didn’t go straight down.

We didn’t see a steep decline in production until this past January.

You can see what I mean in the chart below…

Lars Eirik Nicolaisen – a partner at energy-consulting firm Rystad Energy – was the only oil bull at the EIA conference. He said the key to understanding what has happened to oil production – and consequently, oil supply – comes down to invested dollars, which are otherwise known as “capital expenditures” (or “capex”).

Lars Eirik Nicolaisen – a partner at energy-consulting firm Rystad Energy – was the only oil bull at the EIA conference. He said the key to understanding what has happened to oil production – and consequently, oil supply – comes down to invested dollars, which are otherwise known as “capital expenditures” (or “capex”).

As oil prices started to fall and companies began the mad scramble to save cash, capex across the sector fell 20% in 2015. Companies tightened their belts and cut deeper. Nicolaisen said that it will fall another 20% in 2016, which will continue to drive oil supply lower.

You see, oilfields work like bottles of soda.

Imagine if you shook a bottle of soda and pricked it with a pin. Initially, soda would shoot out of the hole until either the level of soda or the pressure fell too low.

Oilfields work the same way. To keep production up, companies have to spend money cleaning the wells and drilling new ones to keep the oil flowing. If they do that, the average oilfield’s production will only fall about 5%-7% per year. That’s because the pressure in the field will still decline, like the pressure in a soda bottle.

However, if they don’t spend that money, a field’s production will fall faster… 10%-12% per year, according to Nicolaisen.

He believes we’ll see enough cuts to capex for U.S. production to hit that 10%-12% decline rate by the end of this year. That would take another 900,000 barrels of oil per day off the market.

It’s important to note that the difference between supply and demand is only about 2 million barrels of oil per day. The predicted decline in U.S. production would cut half of that out. As that happens, oil prices will continue to rise.

We’re not ready to jump into the oil sector with both feet today. But as the uptrend in the sector resumes, producers will benefit the most.

In my Stansberry Resource Report newsletter, we own a “basket” of producers. We’re hoping to catch the uptrend in the early stages. But we’re keeping our stop losses tight in case we’re wrong. I suggest you do the same.

Good investing,

Matt Badiali

[ad#stansberry-ps]

Source: Growth Stock Wire