Since the salad days for stocks ended with the 2008 financial crisis, the new normal has been slower than average economic growth coupled with friendly (low) interest rates.

The financial world hasn’t returned to, well, normal due to some setbacks (Brexit most recently) and more headwinds (too much debt and bad demographics in developed economies).

[ad#Google Adsense 336×280-IA]Post-Brexit, the “smart money” is now wagering that interest rates are all-but-certain to stay low for longer (til 2018, at least).

In a world where growth and yield remain scarce, assets that provide one or the other will be in hot demand. And how about stocks that provide both?

Forget about it…

Dividend growth stocks may be trendy today, but we’ve only caught a glimpse of their future fame.

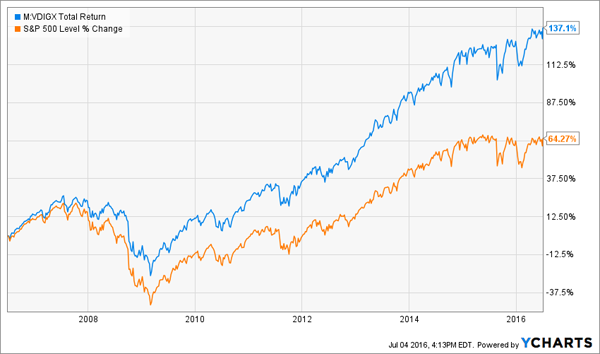

Over the last decade they have certainly delivered, with the Vanguard Dividend Growth Fund (VDIGX) doubling up the S&P 500:

Vanguard Dividend Growth Doubles Up the S&P 500

As a group they should continue to outperform as their unique combination of yield and growth become increasingly popular in a no-yield, no-growth world. But not all dividend growth stocks will rise along with the flooding tide.

As a group they should continue to outperform as their unique combination of yield and growth become increasingly popular in a no-yield, no-growth world. But not all dividend growth stocks will rise along with the flooding tide.

Some will easily rally 100% or more in the years ahead. Others, though, will languish – and may even decline in price. Why? Because investors are paying too much for them today.

The problem with popularity is that, as prices rise, yields decline. And if they drop enough, payout growth won’t save the day. Which should we buy, and which should we avoid? Let’s start with VDIGX’s top five holdings – and I’ll show you how we can do even better than this already-excellent fund.

Vanguard’s Top 5 Dividend Growers

VDIGX’s largest positions are dividend growth monsters. These firms boost their payouts by double-digits annually, and sometimes by 15 to 20%.

Its top holding is Microsoft (MSFT), which pays 2.8% today and has boosted its payout by 17.6% annually over the previous 5 years. However that’s the past, I am concerned its dividend has limited upside going forward.

Since my original piece the stock is down 2.7% and the company shelled out $26.2 billion for LinkedIn (LNKD) – an expensive deal that most likely dusted some shareholder value on the spot. MSFT trades at a rich 40-times earnings.

Microsoft’s Steady Dividend Growth, Manic P/E Ratio

UPS (UPS) is in the second spot at 3.1%. It’s a nice “pick and shovel” play on the e-commerce boom, up 12.7% since I pointed out a buying opportunity thanks to unfounded Amazon (AMZN) worries.

UPS (UPS) is in the second spot at 3.1%. It’s a nice “pick and shovel” play on the e-commerce boom, up 12.7% since I pointed out a buying opportunity thanks to unfounded Amazon (AMZN) worries.

The stock pays 2.9% today. It’s not the deal it was in February, now fully priced at 20-times earnings and about 20-times free cash flow (FCF). Every year or two UPS will sell for 15-times FCF or less – that’s the best time to buy.

Costco (COST) takes Vanguard’s bronze position. It’s another shareholder friendly firm that everyone wants to own, currently paying 30-times earnings and 37-times FCF for that right. On paper, shares yield just 1.2% today though the company likes to shell out special dividends every couple of years (which usually aren’t reflected on most financial websites.)

Finally Nike (NKE) and apparel maker TJX Companies (TJX) round out the top five. They pay just 1.2% and 1.4% respectively and neither is cheap at 26 and 23-times earnings.

This 5-stock portfolio pays just 1.8% and trades for an expensive 28-times earnings. Even a special dividend from Costco would barely lift the yield above 2%. Still it’s a better option than the S&P 500, which yields the same and is only growing its collective payouts at about half the rate of the Vanguard group.

Regular readers may know that I have my 401(k) 100% allocated to VDIGX because it is statically the best option of any Vanguard fund. Dividend growers simply outperform all other stocks over the long haul thanks to their ability to boost earnings year after year and return increasing hauls back to shareholders. Studies show that dividends account for about half of stock market returns over the long run – with the growers being the superior part of that lot.

I had to “settle” for VDIGX in my 401(k) because I’m limited to Vanguard funds there. But you can do better in your individual accounts – just as I can and do – because we don’t have Vanguard’s “curse” of having to deploy $29.6 billion, either! We can seek out and buy the best small and midcap companies if they are better bargains – which they almost always are.

Be Nimble for More Future Growth AND Current Yield

Yes, the only adjustment we need to make to find dividend boosters with more growth potential and current yield is to look beyond the megacaps.

Here’s a 5-stock portfolio with similar to superior growth potential that yields 3.2%. And don’t let its relative lack-of-size intimidate you – these issues have each doubled, tripled or even quadrupled their payouts over the past five years!

Big Payout Hikes Don’t Require Household Names

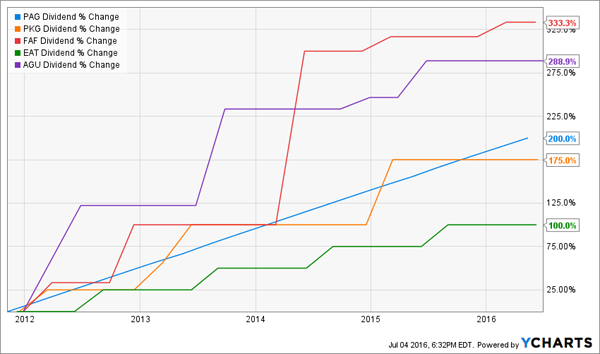

By moving beyond the comfort zone of many investors and fund managers – which is often a product they’ve used before themselves – we can boost our yield and growth. And see returns up to 335% (in a period that included the financial crisis) over ten years!

By moving beyond the comfort zone of many investors and fund managers – which is often a product they’ve used before themselves – we can boost our yield and growth. And see returns up to 335% (in a period that included the financial crisis) over ten years!

Returns Up To 335% In Ten Years

Agrium (AGU) sells agricultural products and services. Through a farming boom and bust it’s still returned an impressive 335% to shareholders over the last ten years. Shares yield a healthy 3.9% today, and the firm’s payout ratio is a manageable 49% of earnings.

Agrium (AGU) sells agricultural products and services. Through a farming boom and bust it’s still returned an impressive 335% to shareholders over the last ten years. Shares yield a healthy 3.9% today, and the firm’s payout ratio is a manageable 49% of earnings.

Brinker International (EAT) may not be a household name itself but its Chili’s Grill & Bar and Maggiano’s Little Italy restaurants sure are. EAT has doubled its dividend over the last five years and there is room for the payout to continue growing with profits (just 37% of earnings are paid in dividend today). Shares currently pay 2.8%.

First American Financial (FAF) is niche insurance and financial services firm that provides title insurance to homebuyers and sellers. A steady to rising housing market is usually bullish for FAF – and that’s been driving its 333% dividend growth over the past five years. Shares pay 2.6% today.

Penske Automotive Group (PAG), like much of the automotive industry, is dirt cheap. Shares trade for just 8-times earnings and pay a generous 3.4%. Its earnings-per-share (EPS) growth (+115%) has greatly outpaced its stock price (+33%). Shares are due to play catch up if the market ever admits that the car market is staying stronger for longer than anticipated:

Penske’s EPS & Dividend Run Laps Around Its Stock Price

Finally Packaging Corporation of America (PKG) sells protective packaging for all sorts of products like produce, retail displays and anything you’d order online. It’s another “pick and shovel” play on the e-commerce boom with much less name recognition. Thanks to its relative obscurity, shares still pay 3.3% today even after a 317% stock price move over the last decade.

Finally Packaging Corporation of America (PKG) sells protective packaging for all sorts of products like produce, retail displays and anything you’d order online. It’s another “pick and shovel” play on the e-commerce boom with much less name recognition. Thanks to its relative obscurity, shares still pay 3.3% today even after a 317% stock price move over the last decade.

— Brett Owens

But My Favorite Dividend Grower Pays 7% Already Today! [sponsor]

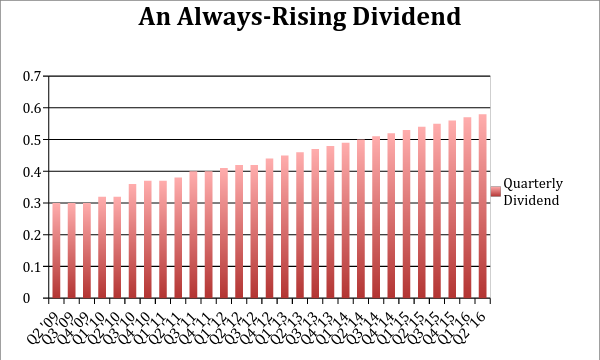

I actually like one sector even better right now for income growth investing. My favorite firm, in fact, pays a gaudy 7% today. And it increases its payout not just every year, but every single quarter:

You see, no matter what happens with Britain, this year’s election, or even China or the Fed, there’s one sure economic bet in America: The country will be older in the future than it is now, and demand for healthcare services is set to skyrocket.

You see, no matter what happens with Britain, this year’s election, or even China or the Fed, there’s one sure economic bet in America: The country will be older in the future than it is now, and demand for healthcare services is set to skyrocket.

In fact, by 2024, national healthcare expenditures are expected to climb to $5.43 trillion, or about 20% of GDP.

This growth is fueled in large part by the Baby Boom generation. They make up 28% of the U.S. population and number 77 million strong. 10,000 of them turn 65 every single day and will continue to do so every day for the next 15 years.

I’ve uncovered three particularly solid healthcare plays – including the “every quarter” dividend grower – that are set to reap massive profits from this demographic shift.

They pay yields of 6%, 7% and 8% respectively – and all three are increasing earnings and their dividends annually. Click here for [more information] to discover exactly how we’re playing the biggest demographic shift in U.S. history.

Source: Contrarian Outlook