Memorial Day weekend has come and gone. This holiday always leads me to reflect on the sacrifices current and previous generations have made to enable the liberties and freedom we are so fortunate to have in this country.

Sometimes we take this for granted. In the times we live in, forgetting sometimes comes easier than remembering.

[ad#Google Adsense 336×280-IA]Especially given that we have one of the most contentious elections in recent memory on the horizon, the country remains stuck in the weakest post-war recovery on record, and divisions within the nation have rarely been so plain.

For investors, the market remains challenging.

Profits within the S&P 500 are down from the same point a year ago as we head into the fifth straight quarter of a “profit recession.”

Equities remain at about the same point as they were in October of 2014 when the Federal Reserve ended the last of its various “Quantitative Easing” programs and the yield on the ten-year treasury bill remains below two percent.

Defaults in the energy sector have already surpassed the total from all of 2015, job growth seems to be slowing a bit recently, and retail sales are not what one would expect given the gasoline “tax cut” as the consumer remains frugal.

In times like these I take solace in that it could always be worse. At least we are not Europe. The headlines coming from the continent in any one week make you wonder if the Eurozone will ever find its way to seeing decent and solid economic growth again. Here are some of the headlines from just one day last week.

Let start with Germany. Before the market even opened on Tuesday, Moody’s downgraded the debt of Deutsche Bank once again, this time to 2 levels just above junk status. Most major banks in Europe trade about where they were in 2009. Without a healthy banking system, it is hard to see how Europe can ignite any significant growth. That same day, news broke that investor confidence in Germany slid in May, falling to 6.4 points from 11.2 in April, and way below the long-term average of 24.4 points.

Meanwhile, in the second largest economy in the EU, the French raided Google’s headquarters in Paris. That country is trying to shake down the search company for $1.6 billion in “back taxes” it believes it owes. Also, 50% of France’s gasoline refinery capacity was shut down thanks to strikes and blockades by unions – the country’s favorite sport.

The IMF also increased its call this week for unconditional debt relief for Greece which I am sure will go down well in Frankfurt and with German taxpayers who have to be tired by now of carrying the weight for its less efficient/free spending southern neighbors.

Austria also barely avoided, by razor thin margins too, being the first country in Europe to elect a far-right head of state since the Syrian crisis, by electing a far-left head of state as the Green Party just eked out putting their guy in office. It was the first time since WWII that neither of the two largest parties in the country made it to the run-off election.

The only good news [that] came out last week in Europe was that new polls showed that it is unlikely the U.K. will vote to leave the EU when that country goes to the polls on June 23rd. However, given the huge structural problems of Europe, the actual results might be closer than expected.

The Federal Reserve is looking like it will raise rates by a quarter point in June. With the European Central Bank still fiddling with a negative interest rate policy in a desperate attempt to engineer any sort of growth after years of stagnation, the dollar looks set to strengthen further against the Euro. This will be a headwind both for S&P 500 profits as well as a counterforce to the recent rally in crude, gold, and other commodities. This is a key reason I remain deeply underweight the energy and mining sectors.

It also means investors should continue to underweight large multinationals that get a good portion of their revenues from Europe such as IBM Corp (NYSE: IBM). Between the strong dollar and little economic demand, those companies could remain under pressure for the foreseeable future.

The United States remains the best house in a bad neighborhood, although it feels long overdue that our plumbing was replaced.

The United States remains the best house in a bad neighborhood, although it feels long overdue that our plumbing was replaced.

Domestic focused plays are probably your best bets in the current market.

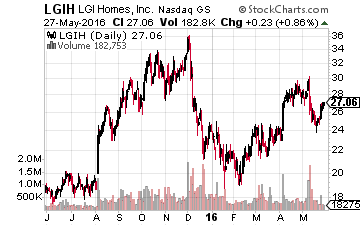

These include a lot of home building and construction plays that have been profiled on these pages in recent months such as LGI Homes (NASDAQ: LGIH) and Sterling Construction (NASDAQ: STRL).

In addition, biotech seems to be finally coming out of its long and deep slump. Helping the sector immensely is a pickup in M&A activity. Several firms in the $500 million to $5 billion range have been bought out in May. Most with premiums in the 50% to 60% range, showing how undervalued some of these names have gotten in the huge bear market that enveloped the sector starting last summer.

I look for a continued push in this area as drug giants are flush with cash to do some “bargain hunting” and mega-mergers seem unlikely to be approved by regulators at the current time.

I look for a continued push in this area as drug giants are flush with cash to do some “bargain hunting” and mega-mergers seem unlikely to be approved by regulators at the current time.

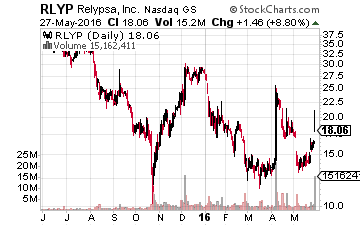

Names like Acadia Pharmaceuticals (NASDAQ: ACAD), Relypsa (NASDAQ: RLYP), Merrimack Pharmaceuticals (NASDAQ: MACK) and Synergy Pharmaceuticals (NASDAQ: SGYP) which all have highlighted in previous columns are undervalued as standalone entities but also make logical acquisition targets.

That is my view on the market as we get set to enter what could be a long and hot summer season.

— Bret Jensen

[ad#ia-bret]

Source: Investors Alley

Positions: Long ACAD, LGIH, MACK, RLYP, SGYP, and STRL