The dog days of summer are here, and you may be tempted to put your portfolio on autopilot and check out for the next three months. That would be a big mistake, though, because you could miss out on some of the year’s biggest dividend hikes.

Case in point: the four companies below, all of which are getting set to juice their payouts this summer—but I only see three as buys right now.

Medtronic: A Dividend-Growth Machine

[ad#Google Adsense 336×280-IA]Investors in Medtronic (MDT) could be looking at an 18% dividend boost in June, or at least that’s what Barron’s recently predicted.

It’s a sensible call after the company gave its shareholders Christmas in June last year, with a 25% raise. The stock currently yields 1.9%.

Big dividend hikes aren’t uncommon at Medtronic, which has hiked its payout for 38 straight years, more than enough to snag it a place in the Dividend Aristocrats club.

The medical device market will thrive as baby boomers age, and Medtronic is the biggest pure-play manufacturer there is, so it’s perfectly positioned to cash in.

The company’s board is targeting a payout ratio—or dividends as a percentage of adjusted earnings per share (EPS)—of 40% in the next few years. Medtronic expects to report full-year fiscal 2016 adjusted EPS of $4.36 to $4.40 when it releases its latest results on Tuesday, giving it a roughly 35% payout ratio. That leaves plenty of room for more growth, especially with consensus forecasts calling for EPS to jump to $4.70 in fiscal 2017.

And right now, Medtronic is a steal compared to the competition, trading at 17 times forward earnings. To put that in perspective, you’d pay 22 times for C.R. Bard (BCR) and a nosebleed 26 times for Baxter International (BAX).

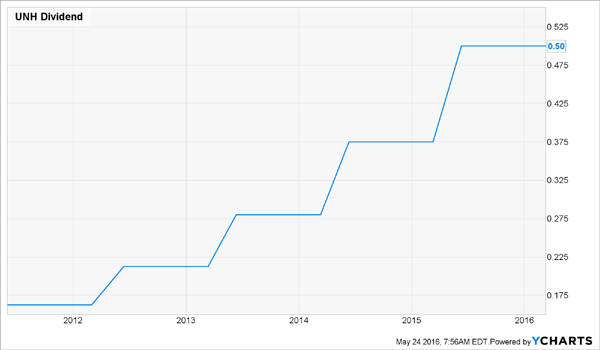

UNH: Double-Digit Payout Growth and 15% Upside

UnitedHealth Group (UNH) could deliver an even bigger dividend hike—33%—than Medtronic in June. Where am I getting that figure? It’s how much the nation’s biggest health insurer boosted its payout in June 2014 and June 2015. The stock currently yields 1.5%.

Of course, past hikes have little bearing on future ones, but the pieces are in place for something big: UNH pays out just 32% of its earnings as dividends; its balance sheet is healthy; and profits are growing fast, with EPS up 14% year-over-year in the first quarter. Profit growth like that is par for the course for the company, which has grown EPS at a 10% annualized rate over the last decade.

Management also made a smart call in April, when it said it would bow out of most Obamacare state marketplaces by 2017. This is a small part of UNH’s business, and the company is losing money on it, to the tune of $475 million in 2015.

Meantime, the stock’s forward price-to-earnings ratio clocks in at 18, a reasonable price for a well-run dividend-grower like UNH. Wall Street’s also bullish: the average 12-month price target on the stock is $150, up 13% from today’s level.

FedEx’s Dividend Takes Flight

FedEx Corp. (FDX) sports a dividend yield that’s much lower than that of UnitedHealth, just 0.6%.

But the courier giant—possibly with an eye to United Parcel Services (UPS), with a 3.1% yield—has focused on boosting its payout in the past few years. In June 2014, it bumped it up by 33%, then followed that up with a 25% hike last June.

I see at least a 20% hike coming this June, thanks to FedEx’s low 35% payout ratio and soaring profits—the company forecasts full-year fiscal 2016 earnings that will be up 20% to 22% from last year.

Two big profit drivers are its ongoing cost cuts and its acquisition of TNT Express, which closed last week. TNT is FedEx’s biggest acquisition in 43 years, and management says it will be “very accretive to earnings” starting in 2018, once all the integration costs are paid.

FedEx is a bargain, to boot, trading at 15 times forward earnings, well below UPS, at 18, and its five-year average (16).

Altria: Wait for a Pullback

No matter what doctors tell us, some people continue to smoke: one in six Americans still haven’t kicked the habit, despite the warning labels, endless PR campaigns and smoking bans.

As long as that’s the case, Altria Group (MO) will keep its sales, profits and dividends rising. The company’s cigarette brands include Marlboro, Benson & Hedges and Players. Altria is also grabbing a piece of the vaping craze, churning out e-cigarettes and the flavored liquids that go along with them.

Altria’s payout ratio stands at 79%, just below management’s stated goal of 80%, so the company will have to rely on rising earnings to power further increases. That should be no problem, however, given Altria’s steady EPS growth in the past five years:

Last August, the company delivered a 9% payout increase, and something similar is likely in the cards this year. Altria is also starting from a higher base than my other three picks, thanks to its 3.5% dividend yield.

However, the stock is up 25% in the past year and trades at around $63.90, near its 52-week high. I’d put this one on your watch list for now—and consider MO if it dips down to the $58 range (which would put its yield closer to 4%). Then again, if it’s yield you’re after, here are three bigger payouts with more upside to buy right now.

— Brett Owens

These 3 Stocks Yield 130% More Than Altria [sponsor]

The four companies above are all rock-solid dividend growers, but it will be a long time—if ever—before their yields get anywhere near the payouts on three other income wonders I just sent out an urgent buy call on.

They’re an overlooked asset class called closed-end funds, and they throw off yields of 8.0%, 8.4%—even 11%—like clockwork.

Think about that: if you bought Altria today, the cigarette maker would have to hike its payout by 129% to give you an 8.0% yield on your initial investment. So even if it continued to roll out 9% yearly hikes, you’d still be waiting a decade before you’d get to 8.0%!

If you’re looking to dividend stocks like Altria to fund your retirement, you need to do better.

That’s where my three picks come in: they give you those kinds of payouts right away, and they pay monthly, to boot. Plus they’re all trading at deep—and temporary—discounts, so you’ll also grab 7% to 15% price upside in the next 12 months, in addition to those hefty yields.

You do not want to miss out on these three bulletproof closed-end fund picks. Go right here to get more information now.

Source: Contrarian Outlook