In a world of record low interest rates, where savings accounts offer less than 1% interest, investors are struggling to find a risk-free return on their money that will outpace inflation. With U.S. Treasuries no help, many people are flocking to dividend growth stocks or junk bonds.

Unfortunately, both of these can be volatile, as we’ve seen over the past year. Which is why it’s surprising so few have jumped into a better alternative: municipal bonds.

Benefits of Municipal Bonds

[ad#Google Adsense 336×280-IA]Munis have several advantages, and a big one is their tax-free status.

Many (but not all) municipal bonds are tax free, meaning that the yield they return is actually higher than they first appear.

Another great feature of municipal bonds: they almost never default.

According to Moody’s Investors Service, who rate bonds, just 0.03% of municipals have defaulted since the financial meltdown in 2008.

Given their admirable performance during the worst economic period of our lifetime, future defaults should be far from an investor’s list of worries.

Of course, municipals pay a very low interest rate as a result of their low default rate. And thanks to falling Treasury yields, municipal bond yields have been falling too. Today, a 5-year municipal bond yields just 0.97% on average—still lower than the rate of inflation.

Buying Municipal Funds

You can secure higher returns by choosing riskier municipal bonds, or you can buy a bond fund. Bond funds are a better choice. They are more liquid, easier to buy and sell, and they spread your risk by diversifying across municipalities.

So which fund to buy? The iShares S&P National AMT Free Municipal Bond Fund (MUB) is the largest publicly traded fund. It yields 2.3% today.

Problem is, that’s roughly the rate of inflation—so we’re still not really making any money if we buy this.

Problem is, that’s roughly the rate of inflation—so we’re still not really making any money if we buy this.

An alternative would be municipal bond closed-end funds, which tend to offer higher yields. They can do this because they use leverage—borrowing money at low rates to invest in municipals with higher rates. Leverage can be dangerous, which makes these funds riskier than the low-yielding ETFs out there—but savvy managers are at the helm to ensure that the portfolio is invested in safe securities likely to pay their investors back.

What yields do these funds offer? Blackrock’s Municipal Income Trust (BFK) pays 5.8%, while Eaton Vance’s Municipal Bond Fund (EIM) pays 5.5%. One of the highest yielders is the Pimco Municipal Income Fund III (PMX) at a 6% payout.

The best part? These distributions are tax-free, so you can keep them in a taxable brokerage account, enjoy the monthly dividend checks, and not worry about a big bill from the IRS later. That’s impossible with dividend growth stocks.

The best part? These distributions are tax-free, so you can keep them in a taxable brokerage account, enjoy the monthly dividend checks, and not worry about a big bill from the IRS later. That’s impossible with dividend growth stocks.

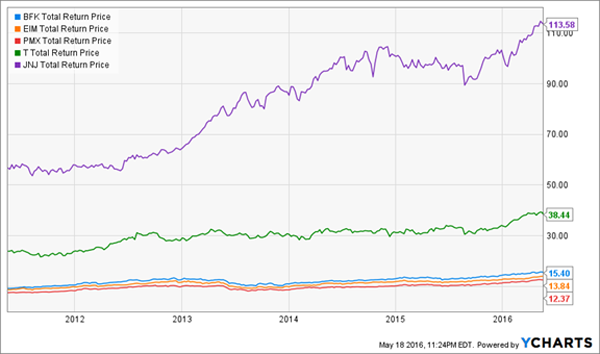

Plus, these bond funds tend to be much less volatile than stocks, even large-caps like AT&T (T) and Johnson & Johnson (JNJ), whose dividends are much smaller (and taxable).

From this chart, we see that the total return for the large cap stocks is more prone to radical ups and downs, while the smooth lines for the bond funds shows relatively limited price volatility over a long period of time. For instance, PMX is 93% less volatile than the S&P 500, so cashing in or buying more over a moderate time horizon of a year or so is easy to do.

From this chart, we see that the total return for the large cap stocks is more prone to radical ups and downs, while the smooth lines for the bond funds shows relatively limited price volatility over a long period of time. For instance, PMX is 93% less volatile than the S&P 500, so cashing in or buying more over a moderate time horizon of a year or so is easy to do.

Conclusion

If you’re building a high income portfolio, don’t forget about municipals and the big potential payouts you can get from buying into these municipal funds.

Closed-ends are the best way to buy these issues. Today, several of these funds are selling at discounts to their net asset value (NAV) – which means you’re also getting free 7-15% upside in addition to the tax-free yields.

— Brett Owens

[ad#wyatt-income]

Source: Contrarian Outlook