To call the stock markets “choppy” so far in 2016 would be a tremendous understatement. I talk to many investors who are having a hard time deciding whether to buy, sell, or stay on the sidelines.

In this type of market, it is nearly impossible for an individual investor to time investments and “buy low and sell high,” to book some attractive profits.

[ad#Google Adsense 336×280-IA]This is one of the reasons that I stick to a higher-yield dividend-focused investment approach.

Like many successful endeavors, my dividend strategy is based on a simple concept, but it can be and is difficult to put into action.

The strategy comes from the idea that stocks that increase their dividends year after year will generate both total returns from share price appreciation and a growing cash income stream.

For me, the most important step is to invest in stocks where there is a high probability of future, continuing dividend increases.

The details of which stocks to pick get tougher. One option is to go with higher-yield stocks where the expected dividend growth rates are low. For example, a stock like Ship Finance International Limited (NYSE: SFL) will grow its dividends by 2% to 6% per year, but investors get a 12% current yield.

To further improve total returns from a stock like SFL, all or a portion of those big dividend payments can be reinvested to generate a growing dividend stream. Taking 8% as cash and reinvesting the other 4% would boost the realized dividend growth rate into the high single-digits, well above current inflation.

Another approach is to invest in stocks with high dividend growth rates and relatively low current yields. Tallgrass Energy GP LP (NYSE: TEGP) has the potential to produce up to 40% annual dividend growth over the next few years, and the stock yields 4%. These two stocks are examples of the extremes in the dividend growth picture.

While I have confidence that both SFL and TEGP will be able to grow dividends going forward, there is a lot of variability in where the actual growth rates will land. I put these two towards the riskier end of the universe of dividend stocks I analyze. However, if they do meet growth expectations, investors will be rewarded with returns well above the stock market averages.

More conservative investors can find stocks with very high visibility towards future dividend growth rates. As an example, there is a very high probability that Realty Income Corp (NYSE:O) will continue its decade long run of 5% to 6% annual dividend increases.

However, the income and safety investing community are very aware of the Realty Income track record and the shares currently yield just 3.8%. That’s a higher yield than normal blue chip corporate shares with lower growth rates, but a relatively low yield compared to dividend growth stocks that are just a step or two up on the risk ladder.

Here are two stocks that offer attractive yield and dividend growth profiles at the opposite end of the spectrum of the yield and growth combination.

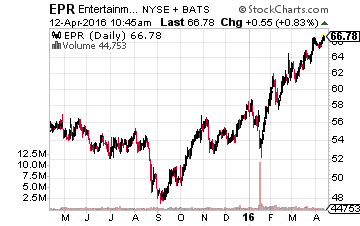

EPR Properties (NYSE: EPR) is a real estate investment trust (REIT) that owns and leases out cinema complexes, specialized entertainment facilities (TopGolf and urban ski centers), and facilities for charter and private schools.

EPR Properties (NYSE: EPR) is a real estate investment trust (REIT) that owns and leases out cinema complexes, specialized entertainment facilities (TopGolf and urban ski centers), and facilities for charter and private schools.

The mix of businesses is well balanced and has allowed EPR to grow dividends by about 7% per year.

Continued future growth prospects are very solid and the historic dividend growth rate should continue. With a current 5.8% yield, EPR is a better paying monthly dividend alternative to Realty Income.

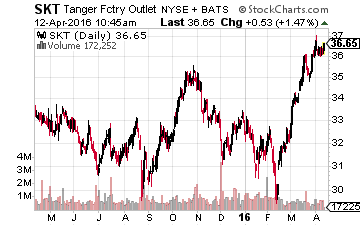

Tanger Factory Outlet Centers Inc. (NYSE: SKT) is a shopping center REIT with 26 years of uninterrupted dividend growth.

Tanger Factory Outlet Centers Inc. (NYSE: SKT) is a shopping center REIT with 26 years of uninterrupted dividend growth.

In recent years, SKT has accelerated its dividend growth into the mid-teens.

This is a very high-quality and well-run REIT.

My analysis from early in the year produced a 13.8% dividend growth forecast this year. The company just announced a 14% increase for the dividend to be paid in May 2016. SKT yields 3.1%. The returns from this type of dividend stock will come from a rising share price to match the dividend growth rates, with the actual dividends coming in as a bonus return kicker.

— Tim Plaehn

[ad#ia-tim]

Source: Investors Alley