First, it was Kinder Morgan (KMI). Then, ConocoPhillips (COP). Which sacred dividend is going to get cut next?

Regular readers know that I believe big oil is a big avoid for now. But if you insist on speculating in the goo patch, stick with Exxon (XOM).

There are payout problems outside of energy, too. A quick look at Reality Shares’ DIVCON screen reveals seven 4% payers in “DIVCON 1” territory. This means they’re more likely to cut their dividend than raise it. Let’s discuss these, and a few more high yielding problem children.

1 Shaky Telecom

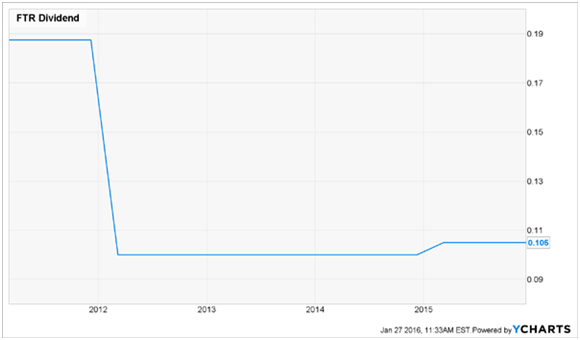

Frontier Communications Corp. (FTR) is a good example of a sky-high yield (8.8%) that should set off alarm bells. As for a low P/E, the “E” part of the equation is non-existent—the telco has posted losses in three of the last four quarters, and the Street forecasts a loss of $0.17 a share in 2016.

Add rising long-term debt (up 74% from a year ago as of the end of Q3) and a payout ratio that’s also headed in the wrong direction (81% of free cash flow, up from 67%) and you get a sense the dividend—which has barely budged since it was cut in 2011—is on borrowed time again.

FTR Hangs Up on Income-Seekers

To drive its growth, the company is paying Verizon Inc. (VZ) $10.5 billion—or roughly twice Frontier’s market cap—for its Internet, phone and TV assets in Florida, Texas and California.

To drive its growth, the company is paying Verizon Inc. (VZ) $10.5 billion—or roughly twice Frontier’s market cap—for its Internet, phone and TV assets in Florida, Texas and California.

[ad#Google Adsense 336×280-IA]The deal will triple Frontier’s size, but I’m in no way convinced it has the financial muscle to strengthen this business.

History isn’t on its side, either: when Frontier took over accounts in Connecticut from AT&T, Inc. (T), it triggered a rash of service troubles that had complaint lines at consumer-protection agencies and state regulators ringing off the hook.

2 Bad Utility Decisions

FirstEnergy (FE) already slashed its dividend by a third two years ago.

That’s not what you want to see from a utility. The company still pays 4.4% today but DIVCON believes the pain isn’t over yet.

A high 105% payout ratio is a big concern, as the company is shelling out more to investors than it’s earning. And profits are declining – earnings-per-share (EPS) have come in lower in each of the last four years. Management might be too contrarian for its own good – it recently doubled down on coal!

Exelon (EXC) got itself in trouble initially when it overextended itself – when natural gas prices were high – to purchase Constellation Energy in December 2011. “The Natty” soon dropped to historic lows, and the Exelon cut its dividend by 41% in 2013.

Its payout ratio is now a manageable 48%, and management is hinting at a modest 2.5% dividend raise later this year. I disagree with DIVCON here, as I believe this dividend is safe. But I wouldn’t buy it either, and neither should you – namely because there are 5 utility stocks with faster growing dividends.

5 REITs To Sell Now

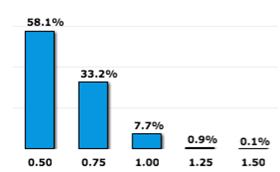

I’m not a fan of mortgage REITs here. Sure, the “smart money” is betting that there will not be another interest rate hike until December:

Fed Fund Futures Rate Probabilities – December 2016

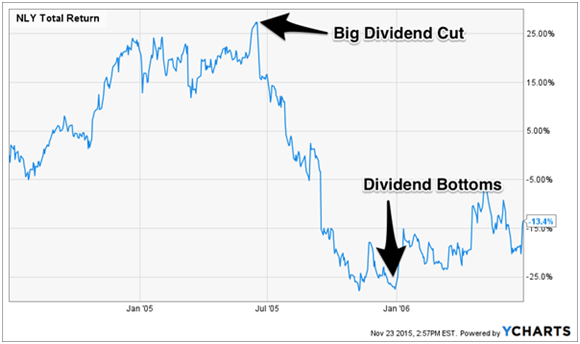

But the likelihood is that rates will eventually creep higher, and “mREITs” do not perform well when rates rise. From June 2004 to June 2006, Alan Greenspan boosted rates from 1% to 5.25%. Remember, mREITs like Annaly Capital (NLY) hold fixed-rate securities that decline in price when rates rise. Investors ran for the exits when Annaly chopped its payout in mid-2005.

But the likelihood is that rates will eventually creep higher, and “mREITs” do not perform well when rates rise. From June 2004 to June 2006, Alan Greenspan boosted rates from 1% to 5.25%. Remember, mREITs like Annaly Capital (NLY) hold fixed-rate securities that decline in price when rates rise. Investors ran for the exits when Annaly chopped its payout in mid-2005.

Higher Rates Made Annaly Cut Its Dividend

DIVCON hates Two Harbors Investment Corp (TWO) in particular – but I’d extend that to American Capital Agency (AGNC), Redwood Trust (RWT), Capstead Mortgage (CMO) and MFA Financial (MFA). If you hold any of these stocks for their double-digit yields, you should sell them right now.

DIVCON hates Two Harbors Investment Corp (TWO) in particular – but I’d extend that to American Capital Agency (AGNC), Redwood Trust (RWT), Capstead Mortgage (CMO) and MFA Financial (MFA). If you hold any of these stocks for their double-digit yields, you should sell them right now.

And if you absolutely have to own an mREIT, buy Annaly. Like Exxon, it’s the best run house on a bad block.

Now let’s address the top “yield trap” sector today…

3 BDCs I Love To Hate

Business development companies (or BDCs) have been hit hard over the past few quarters. Those with large energy investments have seen their stock prices plunge along with oil. They rely on financial wizardry to generate yield and returns for investors, and $30 oil has mucked up some best-laid plans.

Many BDCs now have yields north of 10%. But these sexy BDC yields have been achieved the “wrong way” – with a tumbling stock price.

The biggest risk to date for many BDCs hasn’t been interest rates, it’s been borrower risk – specifically in the oil patch. If the energy sector continues to struggle we can expect to see write-downs for the next three or four quarters. It’s the reason I’ve been hammering BDC firms that have too much of their portfolios in energy.

Gladstone Capital (GLAD) recently reported mixed financial results for its first quarter. By mixed I mean an increase in unrealized depreciation of $38 million and a 19% decrease in net income per share.

Meanwhile Pennant Park Investment (PNNT) reported a tough loss of $40.8 million or $0.56 per share. Pennant Park has an energy exposure of 10% of its market value and 16% of the investment cost.

In its earnings call, CEO Art Penn explained that even though they don’t believe it would happen, a total write-down for all of their energy assets would drop their NAV from $9.02 to $7.28 per share. That’s still 41% higher than the current stock price.

I’ve also been down on First Street Finance Corp (FSC) – because it never earns its shareholders any positive returns. And the company just announced that its book value declined by roughly 7% for the quarter as a result of increased unrealized losses.

Fittingly, the firm agreed to decrease its management fee a quarter point. Apparently investors started asking questions about how much they were paying management in the face of its returns.

— Brett Owens

This 7.5% Dividend Is About to Double [sponsor]

I’ve uncovered a recent spin off tapping into the aging baby boomer profit tsunami. It pays 7.5% today and the yield is expected to double fast. Recent pullbacks have created the perfect buying opportunity just in time for the next dividend payout. Click here for the name of this stock and the Billionaire’s Secret we used to find it…

Source: Contrarian Outlook