Call it China’s revenge—and the sequel to last summer’s horror show is no less terrifying than the original. Just ask the thousands of panicked investors who are, yet again, madly tossing their stocks over the side.

But time and again, history has shown you’re far better off buying into hysterical markets like these than selling. But where should you look for safety AND upside?

[ad#Google Adsense 336×280-IA]I recommend the good old US of A.

By doing so, you’ll instantly dodge two big headaches: the grinding emerging market slowdown and the surging greenback, which is pummeling any profits American companies earn overseas these days.

For an extra margin of safety, hunt for the rarest of breeds: stocks that defy gravity in times like these.

Realty Income Corp.: Built for Gyrating Markets

Case in point: Realty Income Corp. (O), a real estate investment trust that’s beaten back the New Year’s rout, rising 0.4% year-to-date, compared to an 8.0% drop for the S&P 500.

The REIT even tacked on an 11.0% rise during the “interest rate panic” of the last six months, further challenging the (overblown) fear that Janet Yellen’s rate hikes will drive investors away from REITs.

It’s easy to see why Realty Income has grabbed investors’ interest. For one, it couldn’t be further removed from the Chinese mess: the REIT owns 4,400 properties in 49 US states and boasts a sterling 98.3% occupancy rate.

Its list of top 20 tenants (the largest of which supplies just 7.0% of its revenue) reads like a who’s who of America’s most stable businesses, including drugstore operators Walgreens Boots Alliance (WBA) and CVS Health Corp. (CVS)—more on those in a moment—FedEx Corp. (FDX) and Wal-Mart Stores, Inc. (WMT).

But Realty Income—which boasts a 4.6% dividend yield—has two more benefits that don’t get enough attention: it pays dividends monthly, as opposed to quarterly, and it rents its properties under a specific kind of lease that keeps its costs low.

The Joy of Monthly Income

First, the monthly dividend. I love monthly dividend-payers for two reasons: one, if you’re relying on these payouts to cover regular expenses, getting paid monthly—the same frequency as bills come in—is very convenient.

And if you reinvest your dividends, monthly payouts let you do so more quickly, giving your long-term returns a slight lift, thanks to the magic of compounding.

The downside? Few stocks pay monthly. Right now, they’re mostly limited to REITs, business development companies (BDCs) and certain mutual funds. Realty Income is keenly aware of this, to the point that the trust has branded itself “The Monthly Dividend Company.”

Investors also get a commitment to dividend hikes that’s tough to beat: the trust has now raised its payout for 73 straight quarters. Put another way, if you’d bought Realty Income 10 years ago, when it was trading for a little less than half of today’s price, you’d be earning a 9.9% yield on your initial stake now.

Not Your Average Lease

Another thing I like about Realty Income is that it signs up clients under triple-net leases, which means that, in addition to paying rent to the REIT, tenants are on the hook for the building’s operating costs, including taxes, maintenance and insurance.

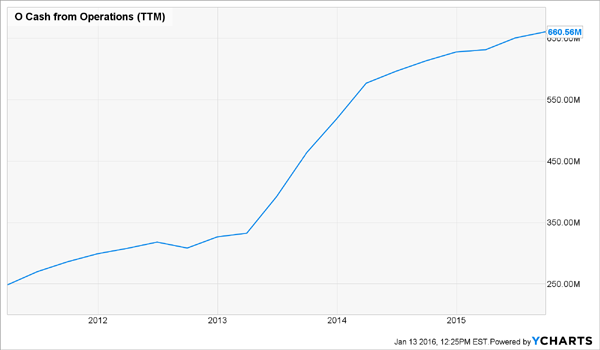

The trust’s business model has helped it nearly triple its operating cash flow in the past five years:

The odds of another quarterly dividend hike are strong: in Q3, the trust posted $0.70 a share in adjusted funds from operations (a better measure of REIT performance than earnings), up 9.4% from a year ago.

The odds of another quarterly dividend hike are strong: in Q3, the trust posted $0.70 a share in adjusted funds from operations (a better measure of REIT performance than earnings), up 9.4% from a year ago.

Meantime, it paid out $0.57 a share, up 4.0%. And while that payout ratio may seem high, at 81%, it’s pretty conservative among REITs, which pay no federal income tax so long as they pass on 90% of their taxable income to investors as dividends.

A Standout Tenant for Your Watch List

Now back to Realty Income’s tenants, which include three companies poised to cash in on the biggest demographic shift in US history: the aging of America’s 77 million baby boomers. I’m talking about the Walgreens, CVS Health and Rite-Aid Corp. (RAD) pharmacy chains.

One in particular, CVS Health, deserves a place on your watch list. The company runs America’s largest drugstore chain, a pharmacy-benefit-management business and 1,100 in-store medical clinics.

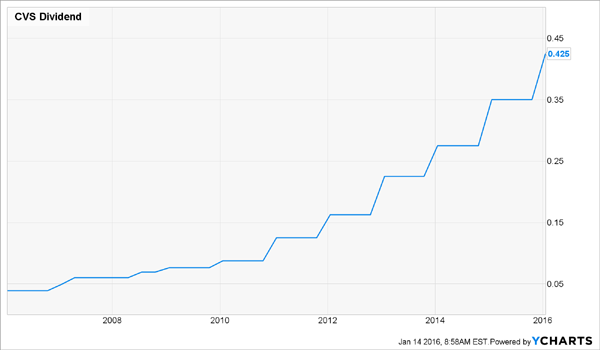

CVS’s yield is just 1.8%, much lower than Realty Income’s, but its commitment to dividend hikes is nearly as ironclad: over the past decade, it’s raised the rate at 9.9% annually, on average. So using the same scenario as Realty Income, you’d now be yielding 6.4% on an investment made in January 2006.

But unlike Realty Income, which has been issuing new shares, CVS has been on a buyback tear, slashing its total number outstanding by 19% in the last five years.

But unlike Realty Income, which has been issuing new shares, CVS has been on a buyback tear, slashing its total number outstanding by 19% in the last five years.

Buybacks are a big plus, because they cut the number of shares outstanding, boosting earnings per share and share prices. They also lead to fatter dividend hikes because they reduce the number of shares on which the company has to pay out.

CVS Invests in Itself

One fly in the ointment could be the proposed merger between Rite-Aid and Walgreens, which still has to get by competition regulators (by no means a given).

One fly in the ointment could be the proposed merger between Rite-Aid and Walgreens, which still has to get by competition regulators (by no means a given).

Together, these two chains supply 8.9% of Realty Income’s revenue, so any resulting store closings would have little impact on the REIT. But the tie-up, which would bring together the No. 2 and No. 3 drugstore chains, could put pressure on CVS.

My Call: Go With O

Of these two, I like Realty Income best right now, thanks to its smart business model, take-it-to-the bank dividend record and monthly payout.

— Brett Owens

This 7.5% Dividend Is About to Double [sponsor]

I’ve uncovered a recent spin off tapping into the aging baby boomer profit tsunami. It pays 7.5% today and the yield is expected to double fast. Recent pullbacks have created the perfect buying opportunity just in time for the next dividend payout. Click here for the name of this stock and the Billionaire’s Secret we used to find it…

Source: Contrarian Outlook