Millions of investors believe they need to invest in retail stocks because they’re a mirror for the consumer-driven economy we live in. That used to be true, but no more.

One of our six “Unstoppable Trends” has completely derailed the premise.

Before I tell you which one and why, though, please know that what I’m about to share with you is very simple.

[ad#Google Adsense 336×280-IA]Get the equation right and it could be like backing Wal-Mart Stores Inc. (NYSE: WMT) in 1994 just before it roared to 600% gains while laying waste to traditional “Mom n’ Pop” stores.

Get it wrong, and you’re more likely to back into something that’s the modern-day equivalent of Sears Holdings Corp. (NYSE: SHLD) – a once proud brand that’s entered a death spiral and fallen by 66% so far despite a legendary bull market run off 2009 lows.

Here’s the shift that matters most when it comes to your money.

Whenever I talk about this at presentations around the world, people short circuit.

“How can big retail be dead?” they wonder.

“It wasn’t too long ago that big box stores killed local retailers with their ginormous inventories and purchasing power…” goes the thinking.

Both of those things are true. Major retailers have been sticking it to Mom and Pops for more than 20 years. They’re all but extinct.

Boy, how times change!

Now it’s the big retailers who are in trouble. According to Green Street Advisors, a real estate analytics firm, more than 15% of all U.S. malls will fail or be converted to non-retail space within the next decade. Two years ago that figure stood at 10%. I think that’s conservative and that as many as 50% of all U.S. shopping malls will fail within the next 10 years.

The key is something called “anchor” stores.

If you’ve never heard the term before, anchor stores are called that because they are typically the major retailers around which customers congregate. Examples you may be familiar with include Macy’s Inc. (NYSE: M), Saks Inc. (NYSE: SKS), Nordstrom Inc. (NYSE: JWN) and, yes, Sears, among others.

Landlords, especially for the big malls, like to have one or more of these companies on their properties because they’ve got tremendous name recognition that will attract other retailers and, by implication, shoppers.

The problem is that the big retailers are in serious bandini. They’re vacating their properties left and right, leaving valuable anchor space empty and, in the process, starting a death spiral.

If the damage stopped there, it’d be one thing. But it doesn’t.

Here’s What Most Investors Are Missing

As we have talked about many times, sales drive earnings, and earnings, in turn, ultimately drive stock prices. Sometimes that’s an immediate relationship, but typically they’re a quarter or two ahead.

When things are great, you can have positive inputs at any step in the process. Debt and fancy accrual accounting will see to it that everything balances out and that stock prices continue higher over time.

But when things slow down or go flat, no amount of fancy accounting can help.

If there are no sales, there are no profits. Period.

Ultimately that translates into stock prices.

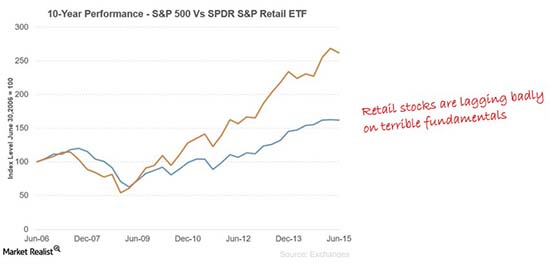

Nordstrom is down 13% in the last month. Sears is down 34% in the 10 months since I recommended Total Wealth readers short it. Even the mighty Wal-Mart fell 10% in the first three weeks of November – a slump that bled more than $19 billion in market capitalization from the retail giant.

This isn’t new. In fact, retail stocks have never recovered from the shellacking they received during the financial crisis. Anybody who’s invested in them has left a lot of money on the table.

Washington may tell you that they are all about Middle America, but this is all the proof you need that the wealth just isn’t there… at least not in conventional terms.

And that’s where our Unstoppable Trend of Technology comes in.

The Internet has obviated conventional bricks and mortar. These days most big retailers are little more than fancy showrooms with limited inventory being driven by consumers with Internet access on the spot.

There’s even a term for how consumer behavior has changed to reflect this – “showrooming,” which refers to shoppers who visit a store to examine a product before buying it online at a much lower price.

At the same time, inventory is changing, which removes a good part of the incentive to visit a big retailer.

For instance, video games are no longer console-driven, but exist in the cloud with hundreds of thousands of players accessing them worldwide. Movies and television have moved from clunky console-sized furniture to crystal clear displays we hold in our hand. Cars are likely to be 3,000 pound metal paperweights… driven by smartphone. Home theater… done.

Retailers are trying to fight back but it’s an expensive uphill battle. Digital shelf displays are growing in popularity because they can be linked to smartphone applications many consumers already use. But the cost of equipping a single location can run well into the six-figures. It’s a multimillion dollar, profit-squashing undertaking.

The goal, of course, is to blur the online/offline experience and capture more sales, but I think the consumer-driven initiative is going to backfire. Big retailers average 5,000 price changes a month, according to Kevin Robison, a U.S. Department of Defense spokesman for the Defense Commissary Agency which runs 180 military commissaries. An electronic shelf price tag can handle 3,000 price changes an hour.

If you’ve ever walked through a store and thought prices were changing as you go from one aisle to the next, you’re not imagining things. It’s exceptionally frustrating, at least to me, but that’s a story for another time.

The best way to play this increasingly blurry line is to align your money with the technology that makes it possible. The retail operation has become almost a secondary consideration, if that makes sense.

Right now that’s companies like Netflix Inc. (Nasdaq: NFLX), Amazon.com Inc. (Nasdaq: AMZN), Facebook Inc. (Nasdaq: FB), Apple Inc. (Nasdaq: AAPL), Alibaba Group Holding Ltd. (NYSE: BABA), and Alphabet Inc. (Nasdaq: GOOG, GOOGL) for three reasons:

- These are companies that have already absorbed and will continue to absorb consumer traffic that used to go America’s malls. Jim Cramer put it bluntly on CNBC recently and I agree: “Let’s be honest here, horrific acts of terrorism really don’t embolden people to go shopping.”

- These are companies with tremendous pricing power. Not only can they overcome a change in consumer behavior, but they actually benefit from it directly by serving up advertising content that’s exactly what their users input. They’re also far more efficient.

- These are companies serving truly global markets, many of which are still in their infancy. That means they can overcome the otherwise negative inertia the U.S. Federal Reserve will inject when it hikes rates.

The problem is that these companies are not exactly cheap. The cheapest, in fact, is Netflix, and that trades at $120 per share, while the most expensive, Alphabet, trades at $738. As my dad noted a while back, you can buy shares… or a house.

Fortunately, there’s a workaround.

My favorite is to buy a core holding like the Vanguard Wellington Fund (MUTF: VWELX), which includes shares of all of ’em.

It’s a balanced fund, so you’re going to pick up a lot of other stuff in the process as well, but that’s not necessarily a bad thing at the moment. Between the dividends and the appreciation potential, you’ve got a lot of stability there, too.

Plus, VWELX does contain a number of retail holdings that are poised to do well when the economy finally mends. Those include, for example, a $470 million position in Wal-Mart and a $621 million position in Lowe’s Companies Inc. (NYSE: LOW) – both are well balanced within the context of Vanguard’s $28 billion portfolio.

That means you’re capturing the technology-driven retail revolution as it happens instead of shuffling from one traditional retailer that’s in decline to another.

The fund charges a pittance considering its outstanding performance, with an expense ratio of just 0.26% when the average expense ratio is 0.86%. Returns really add up over time with that sort of advantage.

In closing, there’s a persistent rumor that the Wellington is closed to new investors. I know because I get tons of calls and emails every time I mention the fund.

That’s actually not true. The Wellington is open to new investors who would like to open accounts directly with Vanguard and through brokers that had a pre-existing relationship with Vanguard prior to February 2013, when the fund restricted new capital to protect existing investors.

I think you’ll be hard-pressed to find a better alternative offering the rock-solid experience, stability, and exposure.

— Keith Fitz-Gerald

[ad#mmpress]

Source: Money Morning