Marc is exploring the architecture, music and history of Cuba this week as part of The Oxford Club’s Cultural Expedition to Cuba.

Since he has limited access to Internet and cellular service, he asked me to pen this week’s Safety Net. So let’s get to it.

It’s been a tough year for “Big Blue.” No, not Michigan Wolverines football fans.

[ad#Google Adsense 336×280-IA]I’m referring to shareholders of International Business Machines Corporation (NYSE: IBM), more commonly known as IBM.

The stock is down 22% since July, leading many investors to wonder if the company is falling apart faster than the Wolverines football program before Coach Harbaugh took the helm.

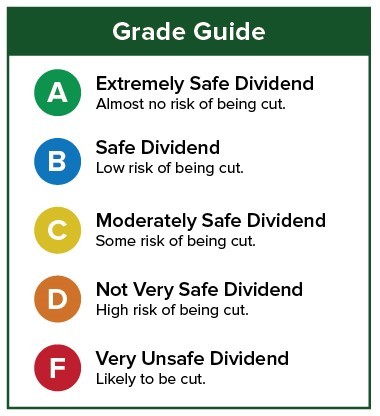

When Marc examined Big Blue’s dividend back in June 2014, he said it was “a dividend even dads can approve.”

With plenty of cash on its balance sheet, a low payout ratio and an expected return to free cash flow (FCF) growth in 2014 and 2015, he gave IBM’s dividend safety an “A.” But that was then, and this is now.

Let’s take a look at IBM’s dividend safety today and find out how the game has played out.

Unfortunately for shareholders, Big Blue’s return to FCF growth hasn’t materialized yet. In 2014, its FCF actually dropped to $13.13 billion. That’s a 5.28% decline from the $13.86 billion it produced in 2013 and 16.59% less than the $15.74 billion of FCF it raked in three years ago.

And IBM’s FCF decline is not expected to reverse in 2015 either. Analysts expect Big Blue to produce $13.1 billion in FCF this year, giving the company yet another dividend safety ding.

But it is not all bad news for investors. Although FCF is declining, IBM’s business still banks a lot more cash than it doles out to shareholders. In 2015, IBM will spend $4.8 billion on dividends. That is just 38.9% of analysts’ FCF estimates. That’s well below Marc’s 75% threshold and gives the dividend plenty of breathing room.

And income investors should not discount IBM’s stellar dividend track record either.

Big Blue has raised its dividend for 20 consecutive years. Those hikes have been more than just token gifts to shareholders – they have been double-digit raises.

Just this year, investors were handsomely rewarded with a nearly 18% increase.

Just this year, investors were handsomely rewarded with a nearly 18% increase.

Even if FCF continues to slide, IBM is bringing in plenty of cash to continue to support and even raise its dividend.

Combined with its low payout ratio, the company should not have to dip into the cash sitting on its balance sheet to fund the dividend anytime soon.

As running back Archie Griffin said, “It’s not the size of the dog in the fight, but the size of the fight in the dog.”

I’d be willing to bet IBM still has a lot of fight left in it.

With a return to FCF growth, I would not be surprised to see a dividend safety upgrade in the near future.

Dividend Safety Rating: C

Good investing,

Kristin

[ad#wyatt-generic]

Source: Wealthy Retirement